|

|

||||||

|

|

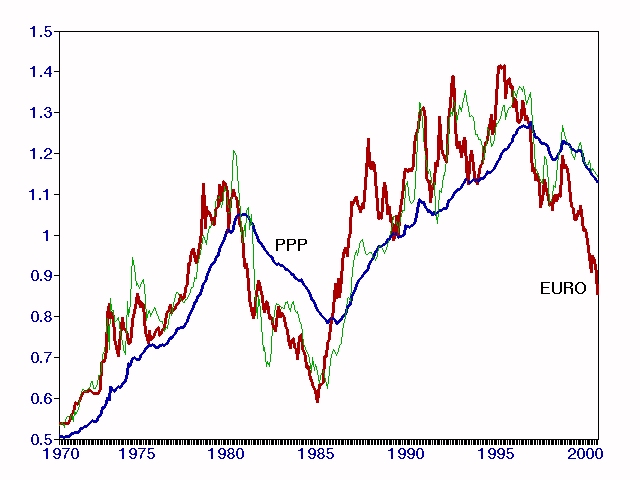

Valuing Foreign Currencies One of the main developments in international markets this year has been the plunge in the euro, which has generated an unusually attractive opportunity in foreign (and particularly European) bonds. We don't frequently get a chance to write about currencies, so the recent development gives us a chance to shift gears. Any currency is both a means of payment and a store of value. So when you try to determine what it's worth, you have to consider both what it can buy in terms of goods, and what it can earn if you hold it as an asset. An exchange rate is just the price of a currency. So a given foreign currency might be quoted as so many dollars per unit ($/FC). If you look at a currency as a means of exchange, you can say, "this basket of goods costs $20 in the U.S., and the same basket costs FC10 in the foreign country, so the exchange rate should be $20/FC10 = 2.0 $/FC." And even if you don't have identical baskets of goods, you can get a reasonable idea of the "long term" tendency of the currency by tracking the movements of price indices in two countries. This is what traders refer to as the "Purchasing Power Parity" (PPP) value of the exchange rate. But PPP is only a tendency that holds loosely over the long term. Over the short term, there's another important factor: interest rates. Suppose that inflation rates are identical in two countries, so the PPP value of the exchange rate is constant over time. But let's say that interest rates in the foreign country are 8%, and they're only 6% in the United States. Well, then, if the currency was just constantly at the PPP value, investors could expect to earn 2% more over the long term by holding the foreign currency instead of the dollar. So as investors buy the currency, it will tend to rise above the PPP value by enough to offset the probable long-term advantage. In general, anytime long term interest rates, after inflation (i.e. real interest rates) are expected to be higher in the foreign country than in the U.S., the foreign currency will be above PPP. Below, we've generated a graph to show you what this looks like. The currency is actually the German mark prior to 1999 (appropriately scaled), and uses data on the euro since then. The analysis holds up strongly using other currencies as well, so our conclusions are not affected by this splice. The thin line is our own proprietary calculation of the exchange rate for the euro implied by interest rates as well as price levels. Note that it does a much better job of tracking actual movements in the exchange rate, though it's imperfect since we have to proxy things like "future expected inflation". Even so, notice that the recent plunge in the euro has produced a wide gap between the actual exchange rate and the exchange rate that is justified by PPP and asset-market considerations. By our calculations, the euro would have to appreciate by over 30% to be appropriately valued, with a justified exchange rate closer to $1.14 than the current $0.85. Now, that doesn't mean that the euro has to close this gap quickly, nor does it mean that the euro can't decline further. Typically, foreign currencies can take as much as 5-10 years to move from extremely undervalued to extremely overvalued conditions. But from a reward-to-risk standpoint, foreign bonds appear attractive. They currently offer interest rates which are competitive with U.S. bonds, plus the prospect of substantial currency appreciation over time, and a low likelihood of sustained currency erosion. Add international diversification to the list of virtues, and international bonds make sense as a portion of a diversified fixed income portfolio. The Hussman Strategic Total Return Fund has the flexibility to invest up to 30% of assets in securities outside of the U.S. fixed income market, including foreign government bonds rated A or higher, utility stocks, and precious metals shares, when market conditions suggest that such diversification is appropriate. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |