|

|

||||||

|

|

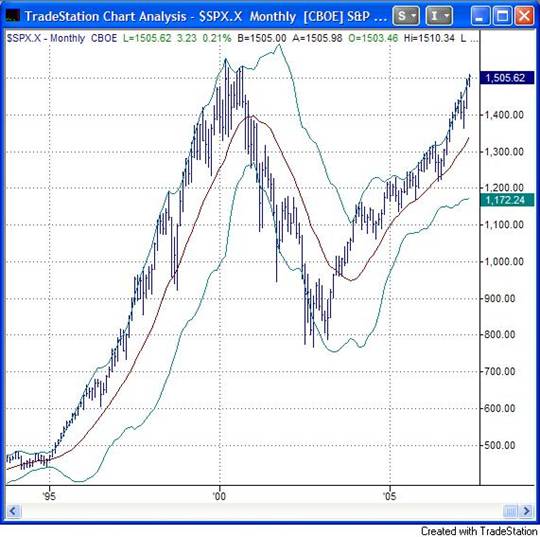

May 7, 2007 Spot the Pigeon It's hard to characterize the recent advance as something other than a speculative blowoff. The Dow has now advanced 23 of the past 26 sessions - something it has not done at any other time in the past century, and at the richest valuations of any comparable stretch (most similar to the blowoff near the peak of the 60's "Go-Go" market). The S&P 500 is currently at about 18.5 times record top-of-channel earnings on record margins. At normalized profit margins, the P/E would be over 25. At every horizon, including monthly, weekly and daily frequencies, the market is either at or through its upper Bollinger bands. As noted in the April 23 market comment, we reestablished a rare set of extreme conditions two weeks ago, which have historically been followed by a few more weeks of upside (typically about 2-3%), then almost invariably by steep and abrupt losses. I am emphatically not forecasting nor relying on a market decline, but it is reasonable to allow for above-average market risk. Monthly and weekly charts offer some perspective on the market's current position:

Despite the fact that this bull market is already far beyond the normal duration of a bull market, we are not relying on the market to enter a bear market immediately. We can allow for the possibility that the bull has months or even years to go. But even if that were the case, we would be hedged here, because the prevailing combination of overvalued , overbought and overbullish conditions has historically been associated with market returns less than Treasury bills, on average, until that combination of conditions has cleared. Even if we can expect a long continued bull market, it is dangerous for investors to assume that we can enjoy durable, continued gains with not so much as a 10% correction, having now gone the second-longest period in history without one, and having fairly extreme conditions in place that have often preceded one. A 10% correction would not even break the bull market trend. The market generally has not achieved durable or satisfactory returns from mature, overextended trends until they have been materially corrected - regardless of whether they were contained within a continued bull market from a longer-term perspective. Suffice it to say that we remain defensive based on prevailing conditions, but are making no inherent assumption that a bear market must be at hand anytime soon. I continue to view the avoidance of deep losses as dramatically more important than overstaying the mature portion of a bull market. The Strategic Growth Fund remains far ahead of the S&P 500 over the complete market cycle (bull peak to bull peak with an intervening bear), which remains the performance horizon central to our investment objectives. Of course, one can also measure a full cycle from bear trough to bear trough with an intervening bull. Assuming the Fund remains hedged and the Fund's holdings do little but track the market (in which case the hedged returns would be close to Treasury bill yields), I would expect even a modest bear market to suffice in placing the Fund ahead of the S&P 500 on every standard performance horizon, again with much less risk over the full cycle. On the subject of the long-term benefits of loss avoidance, Bill Hester sent along the following remark from this weekend's Berkshire Hathaway meeting in Omaha : "Buffett said it wasn't his best ideas that gave him his tremendous track record. It was having a smaller number of bad ideas that resulted in a permanent loss of capital. 'We haven't taken two steps forward and one step back. We've taken two steps forward and a fraction of a step back. Avoiding the catastrophes is really important.'" Bill added, "Buffett counseled investors repeatedly throughout the day to have modest expectations for future stock returns." He did, however, prefer stocks to bonds looking out over the next 20 years - mainly because over the next 20 years, he expected stocks to earn "more than four and three quarter percent. How much more? I'm not sure." Interpreting day-to-day Fund movements The Strategic Growth Fund is currently fully invested in a diversified portfolio of stocks that I view as both favorably valued and having above-average stability in earnings, revenues and financial condition. With the notable exceptions of Archer Daniels Midland and Estee Lauder, which experienced earnings disappointments last week, our stocks have generally enjoyed good earnings reports. In recent sessions, we're alternately seeing days where investors chase garbage (cyclicals, companies with poor financial performance that speculators hope will be "taken out" in an LBO, etc), and other days where investors chase quality. Over the short-term, that causes our stocks to behave as if they have smaller "betas" than they actually have (slightly lagging advances in the market and outperforming during declines), which induces a bit more day-to-day fluctuation in the Fund (given that we've hedged what we believe their betas to be more generally). I've responded by slightly increasing the emphasis on market action in our newer purchases, but I continue to insist on reasonable value and quality, so we may get a little more of that sort of pattern in the coming weeks. The other factor that has introduced some day-to-day fluctuation in recent days is our "staggered strike" position (our long put option strikes are out-of-the-money, but closer to market levels than our short call strikes, which affords added protection against market losses at the cost of less "implied interest" on our hedge). It's important to recognize here that the overall risk of this position amounts to less than 1% of assets, compared with a flat hedge. In other words, if the market was to advance unrelentingly, the difference in performance between our current position and a flat hedge would be less than 1%. On the other hand, if the market declines, the staggered-strike position would be expected to provide a stronger defense. Keep this in mind when interpreting day-to-day Fund movements. If the market declines quickly, then quickly advances again before we have a good opportunity to re-set our strikes, we would expect to gain some amount and then give it back. That's essentially what happened in a few recent sessions - the Strategic Growth Fund gained 14 cents in a couple of trading days, and then gave it back as the market reversed. Extended declines give us the opportunity to lock in hedge returns again and again by lowering our strikes as the market declines. But again, if we enjoy a short-term gain without a good opportunity to reset our strikes, we can lose that gain. In any event, it's important to remember that the potential risk resulting from our staggered-strike position, even in the event of a relentless advance, is less than 1% of assets at present, essentially offsetting interest that we would otherwise earn on our hedge. Overall, I believe the Fund is well positioned to perform well in the months ahead, regardless of market environment, though short-term performance relative to the market will clearly be better on market declines than advances here. Greater fool theory It's fascinating to watch the increasingly carnival-like atmosphere on CNBC on any given day (I generally catch about half an hour with breakfast before the market opens, to hear the prevailing arguments and get the tone of investor sentiment). One quickly finds that the cheerleading tone of the late 90's is back, and the greater fool theory is in full bloom, with investors regularly encouraged to "buy high and sell higher." Lately, the bullish arguments are running so fast and loose that it is apparently no longer a requirement that they have any relationship to fact. Take for example a remark last week that "mutual funds are sitting on piles of cash that these managers are going to have to get invested." Wow. That's just a bald-faced fib. It could not be further from the truth. Cash as a proportion of mutual fund assets has never been lower. Never.

To offer an idea of exactly how stark the situation is, keep in mind that when money market yields (e.g. Treasury bill yields) are high, mutual fund managers have a greater incentive to hold cash balances than when yields are low. Norm Fosback of the Institute for Econometric Research used to account for this by adjusting the level of cash by the level of interest rates, so that the resulting figure is the "excess cash" above (or below) what would be expected, given prevailing interest rate levels.

The adjusted ratio has never been lower either, but using this version of the indicator, you can also see that the current situation is now slightly worse than the prior extreme - which occurred right at the 2000 market top. A similar claim is that "there are a lot of shorts out there, and they're going to be forced to cover." Again, this is not supported by the data. Recent years have seen a proliferation of hedge funds, market neutral strategies, and merger arbitrage vehicles. All of these are based on matched long and short positions. These are not "speculative" or "naked" shorts, and in many cases are not even bets that the stocks sold short will decline (instead, the objective is to earn a difference in performance between the longs and the shorts, regardless of whether they both rise or fall in absolute terms). It is wrong to quote the current short interest as a bullish argument, as if the shorts are somehow compelled to cover here. To the contrary, it is the level of speculative margin debt, not short sales, that has been expanding most rapidly in recent months. The chart below tells the story, where short interest is converted to dollar values using the relatively constant historical average share price of $30 a share (which companies have tended to maintain through stock splits and the like).

Near the market lows in 2002 and early 2003, the ratio of short interest to margin debt spiked higher as investors sold short near the lows while battered bulls got margin calls. Currently, the value of short interest relative to margin debt is the lowest since this bull run began, as margin debt has ballooned. The ratio isn't as low as it was at the 2000 bubble peak, when margin debt exceeded 25% of the total value of commercial and industrial loans in the U.S. banking system, but it's the lowest level of this bull market in any event. The greater fool theory relies on one thing - the assumption that there is somebody else out there who is willing to pay an even more reckless premium for stocks. That's what the market is thriving on at this point; the hope that there is an ocean of unsatisfied demand out there by short sellers or mutual fund managers who will be "forced" to buy. Unfortunately, the facts do not support that assertion. As noted last week, we may see additional buyout activity, but that is driven primarily by credit spreads and does not have a strong relationship to subsequent market returns. In any event, mutual fund cash is at a historic low, and higher short interest is more than offset by rising margin debt. There may not be many greater fools out there after all. As they say, if you're sitting at the poker table and you can't spot the pigeon... you're probably the pigeon. Market Climate As of last week, the Market Climate for stocks was characterized by unfavorable valuations, positive but overextended price trends, and a combination of overvalued, overbought, overbullish conditions that has historically been associated with market returns below Treasury bill yields on average. The Strategic Growth Fund remains fully hedged here, with a staggered-strike position that affords greater downside defense at the cost of lower "implied interest" on our hedges (compared to a "flat hedge"). The difference between this position and a flat hedge amounts to less than 1% of assets. It is not a position that would be expected to produce extended losses - even if the market was to advance relentlessly. Essentially, the risk is limited to foregone interest on the hedge. However, it does contribute to additional "local" fluctuations of a few cents in either direction on a day-to-day basis, and should improve our defenses in the event of a market decline. In bonds, the Market Climate remains characterized by unfavorable valuations and unfavorable market action, holding the Strategic Total Return Fund to a short 2-year duration, mostly in Treasury Inflation Protected Securities. The Fund continues to carry just over 20% of assets in precious metals shares, where the Market Climate continues to be quite favorable on our measures. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |