|

|

||||||

|

|

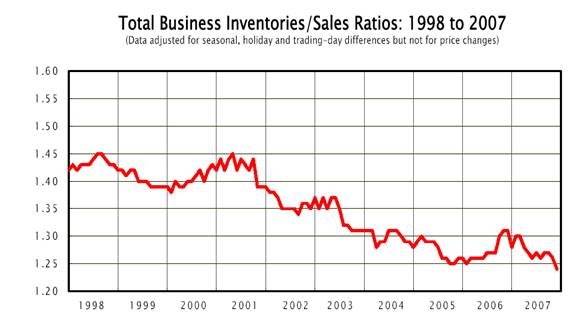

February 3, 2008 A Writeoff Recession and a Dollar Crisis On Friday, the ECRI Weekly Leading Index dropped back to a 6-year low. The ECRI (a widely respected economic forecasting service with a good record) accompanied that decline with its most defensive commentary to date, noting "While the economy and employment did continue to grow through the end of 2007, the window of opportunity to avert a U.S. recession is about to slam shut." From our perspective, the recession warning composite we observed in early November was already sufficient to anticipate a recession, as we've always and only observed that combination of features during and immediately surrounding U.S. recessions. In that context, the weak ECRI figures, as well as the news of a decline in total non-farm employment, are simply additional confirmation of a U.S. economic downturn. Yet while the evidence accumulates that the U.S. economy is in recession, more than a few reporters and analysts have grabbed hold of the Newsweek cover "Road to Recession" as some sort of evidence that a recession cannot happen. This is a pure misapplication of the idea of contrary opinion. Contrary opinion has a history of effectiveness at extremes where a particular event has run its course so fully both in reality and in market prices that it is taken as common knowledge. The magazine cover most frequently held up as a useful instance of "contrary opinion" is the 8/13/79 Business Week issue titled "The Death of Equities." This cover appeared after a decade of zero gains in the S&P 500, at a point where the P/E ratio of the S&P 500 had declined to less than 8. But the truth is that despite the depressed valuations and that dismal cover story, the S&P 500 continued to decline by about 8% following that issue, staged a three-month recovery of about 18%, and then lost it all, hitting fresh lows in March 1980 as the U.S. economy slid into recession. Indeed, the stock market was still lower three years later in August 1982, when stocks finally entered a sustained bull market advance. In contrast, a valid "magazine story" example is the headline that appeared in Commodities Corner of Barron's Magazine on February 12, 2001, after a protracted slump in gold prices: "Tarnished! Nobody expects gold prices to turn up soon." The article began "It's difficult to find any positive news in the depressed gold market. At around $260 an ounce, the metal continues to trade near its cost of production, and almost no one believes it will rally soon. 'Financing is tough to come by these days' in the unpopular gold-mining sector, says Ferdi Dippenaar, Harmony's director of marketing. 'Unfortunately, there is nothing positive on the horizon.'" By the time that this article was published, gold stock prices had already bottomed a few months earlier, with the XAU in the low 40's (the 4 criteria I had previously outlined in Going for the Gold finally turned favorable in September 2000). Since that article was published, gold has advanced to a recent high above $900 an ounce. At some point ahead, we may read cover stories about why commodities are the "new money" and the U.S. dollar is dead. At that point, the commodities run will likely be over (but there is no assurance it won't end sooner if U.S. real interest rates begin to push higher). Again, the effectiveness of the "magazine cover" as a contrary indicator is at extremes, when an event has so clearly run its course in reality and market prices that it is taken as common knowledge. At positive extremes, the common knowledge is that the prosperity will continue forever. At negative extremes, the common knowledge is that things are terrible and there is no end in sight. Lest I make this appear too easy, the fact is that many markets never reach such extremes, so investors certainly can't bank on a trend continuing until the magazine covers give the "signal." But if there is to be a useful signal at all, it is generally only when a boom or a bust has already run an extreme course, and its permanence is taken as common knowledge. Presently, we have none of this. Even the notion that the U.S. economy is in a recession is still widely disputed. With the S&P 500 off only about 10% from its record highs, deep concerns about recession (and the likelihood of weak profit margins) have hardly begun to be reflected in market prices. It will be interesting to monitor magazine covers if we observe a point where stock prices register deep bear market lows, and an economic downturn is broadly viewed as a reality that can only be expected to worsen. But to believe that we can't experience a recession or further market weakness because a single magazine cover expresses concern about that possibility is just naïve. With regard to the stock market, I've often noted that I usually have no opinion about near-term market direction except in unusual instances where stocks are overbought in an unfavorable Market Climate, or oversold in a positive one. As it happens, that presently means that I have a fairly pointed expectation that the market is at risk for a fresh plunge, since the major indices are back to overbought conditions in a still-unfavorable Market Climate. That said, the dollar value of our shorts never materially exceeds our long holdings, nor do we rely on a market decline. Though last week's rebound occurred on the lowest trading volume in weeks, we remain open to the possibility that investors will adopt a more robust willingness to speculate, which we would read out of the quality of market internals (breadth, industry uniformity, leadership, price/volume behavior and so forth). Currently, we don't have enough evidence to infer that investors are doing anything more here than attempting to prematurely buy a dip in an economy that is turning down. But as always, we will be moved as the evidence arrives. I do think it's somewhat odd that many investors don't seem to recognize that even after the recent bounce, the S&P 500 has trailed Treasury bills since September 2006, and has outperformed Treasury bills by only about 2% annually since the end of 2004. Whether stocks are currently in a bear market or not, I would expect 2003 to be the only year of the recent bull market advance for which the gains of the S&P 500 (in excess of Treasury bill yields) will ultimately be retained over the complete market cycle. Economic Outlook If the U.S. economy does indeed turn out to be in recession, what sort of recession is it likely to be? From my perspective, the best way to answer where the economy may be going is to examine where it is. 1) Expecting a U.S. dollar crisis Presently, the U.S. economy is running the deepest current account deficit in history, even as the Federal government has promised to run up another $150 billion in debt to run a "stimulus package." At the same time, the carry between Chinese interest rates and U.S. Treasury yields has now turned negative, meaning that there is no longer a favorable interest rate differential to encourage Chinese investment in U.S. government debt. Moreover, the gradual appreciation of the yuan continues, meaning that the Chinese are also taking losses on their holdings of U.S. Treasuries due to dollar devaluation. The only remaining allure of Treasuries has been for capital gains due to investors' flight to safety, but with yields already compressed, it is increasingly risky to expect continued downward pressure on long-maturity interest rates. This places the U.S. in the difficult position of having to finance an enormous volume of capital needs from foreigners, particularly for Treasury debt, yet without being able to offer competitive yields or strong prospects for additional capital gains. My impression is that the markets will respond to this difficulty with what MIT economist Rudiger Dornbusch referred to in 1976 as "exchange rate overshooting." In the present context, that means a dollar crisis. Specifically, if there is a weak prospect that foreign lenders will achieve a total return on U.S. Treasuries competitive with what they can earn in their own country, and every prospect that short-term interest rates in the U.S. will remain depressed or fall even further, the only way to attract capital is to immediately drive the value of the U.S. dollar to such a sharply depressed level that it will be expected to appreciate over time. 2) Losses in output and employment are not likely to be severe (provided "overshooting" dollar weakness is enough to sustain foreign capital inflows) As we know from the savings-investment identity as well as historical data, a contraction in the U.S. current account implies a nearly dollar-for-dollar contraction in gross domestic investment. During the fourth quarter, we observed much of the pressure on gross domestic investment as a reduction in housing and inventory investment. Though it's likely that we'll observe increasing pressure on other forms of investment such as capital spending, my impression is that housing, commercial real estate, and factory investment will continue to be the areas of greatest downward pressure. So we can expect to observe a flattening out of the U.S. current account and a similar flattening (but probably not a major decline) in overall U.S. gross domestic investment. As I noted last week, the planned $150 billion "fiscal stimulus" will prevent the current account from improving as much as it typically does during economic downturns. Part of that will support consumption (most likely of the durable variety), but the bulk will be saved and channeled through the economy to support existing levels of gross domestic investment. Inventories are already very lean, and the U.S. inventory/sales ratio is already quite low, which suggests that we are unlikely to observe much further retrenchment there.

3) A "Writeoff Recession" So in terms of GDP, I would expect to observe some slowing in all categories of expenditure, with the worst showing in residential investment. Still, I doubt that the losses in GDP (the "real" production of goods and services) will be particularly striking or deep. Rather, the current economic downturn is likely to focus its damage on asset prices - the U.S. dollar, home values, low and mid-quality debt, and equity prices (largely through the combination of narrowing profit margins and lower valuations). In short, I expect that we are in the process of what might be called a "writeoff recession," where significant amounts of asset value and perceived wealth will ultimately be written off. There will undoubtedly be some "wealth effects" on the real economy, but I would expect these to be only moderate. Whether we look at housing, mortgage backed securities, or stocks, the underlying reason for a decline in asset prices is the same - the prices are too elevated, relative to the stream of cash flows they will produce, to achieve an acceptable rate of return. In housing, there remains a wide gap between broad home price indices and measures of personal income, even adjusting for mortgage rates. A realignment of home values with incomes does not require a recession or employment losses, but will be accelerated by those factors. Similarly, lower-tranche mortgage securities and CDOs (and increasingly the higher-rated ones) are facing disappointments in their payment streams due to mortgage foreclosures, while potential buyers of these securities require much higher risk premiums as compensation, which we observe as still lower prices for that mortgage debt. Similarly, in stocks, analyst estimates reflect a quick return to record profit margins about 50% above their historical norms. If those assumptions disappoint and it becomes clear that profit margins will not be forever sustained at record highs, it doesn't only imply near-term earnings disappointments - it implies that the whole stream of future earnings impounded into stock prices is wrong. After all, a moderate price/earnings multiple on elevated earnings does not imply moderate valuation. This is why we use a variety of measures to gauge valuations - you can't capture the whole valuation picture with only one. It's not useful to estimate market valuations just by plopping operating earnings into the right side of an equation and getting a price forecast on the left. The accounting matters. The profit margins matter. The balance sheet matters. The tendency to repeatedly write down losses as "extraordinary" matters. The extent to which earnings are implicitly given away to executives and employees through stock option grants matters. What matters most is the long-term stream of cash that companies can actually deliver into the hands of shareholders, and whether that stream of cash would provide an acceptable long-term return if you paid the existing share prices. We're certainly willing to assume higher growth rates for well-managed companies with defensible product lines, which is why we don't simply define value as "low P/E" or "low price-to-book." But at a market-wide level, valuations remain far too high to provide investors with tenable long-term returns. The elevated values of home prices in recent years resulted from a combination of speculation on perpetually rising real estate values, coupled with reckless lending. The elevation of stock prices has had much to do with unusually wide profit margins resulting from a depressed share of GDP going to wages and salaries. The expansion in the U.S. current account deficit has resulted largely from profligate U.S. fiscal policy, which absorbed an excessive amount of domestic savings and left us dependent on foreign capital inflows to finance our domestic investment. An economic downturn, even modest in terms of GDP contraction, will simply accelerate the inevitable reversal of these unsustainable trends. As I noted last year, the bulk of mortgage resets did not even begin until October, and are likely to continue well into 2009. At worst, the newly reset mortgages have only now gone delinquent, and it will still be several more months until we see a corresponding rise in foreclosures. At that point, we can expect a major acceleration in writeoffs of lower tranche mortgage debt. Financial companies can't write this off yet, because the losses have not yet emerged, and it is impossible yet to know which particular debts will fail. It is incorrect and unrealistic to believe that financial companies can simply "come clean" and put all of this behind them. Again, I don't believe we are likely to observe major declines in consumption, or capital spending such as information technology - even assuming the U.S. has entered a recession. Indeed, nominal consumption has never declined year-over-year. Though consumption represents the largest share of the economy, it is also the most stable (Friedman and Modigliani were right). Yes, growth rates will probably slow for these classes of spending in a recession, but the bulk of the downward pressure is likely to fall on housing and fixed investment. Meanwhile, an already lean level of inventories should help to prevent much further decline in inventories, which should offer some support to industrial production. Since negative inventory investment or "inventory runoffs" represent a good portion of the output losses in a recession, it follows that losses in real economic output (and by extension, employment), though not insignificant, are unlikely to be dire. Brace for trouble, but don't speculate on it This is likely to be a painful economic downturn - not because of massive job and output losses, but because of losses in the value of things that people count as their assets (primarily housing, non-agency mortgage debt, and equities). Foreigners provided a large portion of the capital that fueled the runup in asset prices, so they will undoubtedly bear a good portion of the subsequent losses through dollar depreciation and writeoffs in the value of their U.S. financial assets. A number of foreign banks have already experienced large losses and writeoffs. The simple fact is that international diversification typically helps least when the U.S. markets are in disarray. The recent oversold bounce in the U.S. stock market does not change these fundamentals. We remain open to the possibility that investors will adopt a fresh willingness to speculate, but we need to observe further improvement in market internals in order to draw that conclusion. In the meantime, January's oversold condition is "cleared," and the market is again overbought in a still unfavorable Market Climate. I noted similar conditions in the December 10 comment (S&P 1515.96), just before the market slide turned brutal. I currently view a fresh plunge as a significant risk. The other growing risk is to the U.S. dollar, largely because of the move to a negative carry between U.S. and Chinese interest rates in recent weeks. None of these threats are so certain that we would establish investment positions that rely on them, and the dollar value of our shorts never materially exceeds our long holdings. Still, we remain braced for serious risks, which I would expect to favor the positions we do hold. Regardless of market direction (and provided that our long-put/short-call index option combinations have identical strike prices and expirations), the return on our hedged investment stance is likely to be driven by the difference in performance between our diversified stock holdings outperform the indices we use to hedge. To the extent that investors gradually rediscover the value of earnings stability, balance sheet quality and moderate valuation, and shift away from their affection for the unreliable cyclicals and speculative issues that have led the market in recent years, I believe we are in the right place regardless of near-term market direction. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action, holding the Strategic Growth Fund to a fully hedged investment position. Given that the market's oversold condition has cleared, the Fund again has a "staggered strike" position that I would expect to provide a strong defense against fresh downside pressure (though losses might still occur if our stocks were to perform poorly or if we experience a net decay in option time-value). In bonds, yield levels have become somewhat compressed, finally prompting a reduction in our TIPS position to bring the overall duration of the Strategic Total Return Fund to about 1 year. The issue here is that inflation-protected securities are now so sought after that the economy would have to deliver long-term inflation of about 2.6% just to match the already depressed yields on long-term Treasuries. That's not necessarily a poor expectation over the short-term, but long-term yields appear increasingly compressed because of default concerns and a flight-to-safety, so that even TIPS prices now include a somewhat speculative component. While it's rare that we invest in Treasury bills as a major asset class in the Strategic Total Return Fund, my impression is that a low, safe return is preferable to a low or negative speculative one. Meanwhile, in precious metals, the Market Climate continues to be favorable, particularly with the specter of accelerated dollar weakness, but given that many of these stocks have become fairly overbought already, I clipped our precious metals position lightly toward 20% of assets in Strategic Total Return. Again, the Market Climate in precious metals continues to be favorable on our measures, but I do try to manage the risks given the volatility of precious metals shares, so it's appropriate to vary our exposure around our core position when intermediate-term trends become particularly stretched. As we begin to observe more reasonable valuations in the general equity market, you'll see us respond the same way in the Strategic Growth Fund. For now, the risks in the overall stock market remain elevated. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |