|

|

||||||

|

|

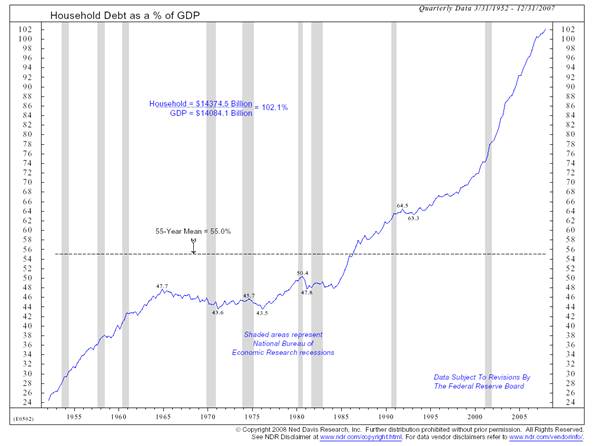

May 5, 2008 Deja Vu Well, having declined nearly 20% from its peak, the S&P 500 has recovered about half of its loss in a period of several weeks, taking the index within about 10% of the all-time high it registered in the mid-1500 range a few quarters ago, with the Dow Industrials down even less. Transportation stocks, in particular, have enjoyed a scorching rally in recent weeks, bettering their prior bull market highs. Despite the fact that our most reliable recession indicators registered a clear warning late last year pointing to an oncoming economic downturn, the unemployment rate stands only about a half-percent above its lows and remains modest on a historical basis. The option volatility index has declined significantly, while credit spreads and advisory bullishness are on the mend. All of this suggests that market participants believe the worst is over, thanks largely to the actions of the Federal Reserve. For our part, the Strategic Growth Fund has achieved positive returns since the market's peak. Still, the Fund has not participated in the recent advance, and remains a few percent below its all-time high, but we are willing to take a more constructive position if market internals improve. But enough about January 2001. Talk about deja vu. At that time, market conditions could be precisely described by the preceding paragraph, including the optimism of investors. As I wrote in my weekly market comment then, "Everybody seems to believe that the Fed has bought a market bottom, and that the current economic slowdown is "old news". We're skeptical. Mainly because the current economic downturn is coming off of a capital investment boom financed with a great deal of leverage. We believe that the economy is in the early phase of a "deleveraging cycle". Investors who believe in the omnipotence of the Fed have evidently forgotten phrases like "liquidity trap" and "pushing on a string", which are ways that economists describe the failure of easy money to stimulate the economy when spending is sluggish. Well, that's what we're likely to get." As it turned out, the rally into 1/30/01 was quickly erased by a plunge in the S&P 500 Index of -19.7% into 4/4/01, followed by a powerful bear market rally of 19.0% through 5/21/01. The S&P 500 then proceeded to surrender that gain, and the events of 9/11 worsened an already weak market, driving the market down -26.4% from May's rally high. The S&P 500 then surged 21.4% into 1/4/02, dropped -7.9% into 2/7/02, advanced 8.3% into 3/19/02, collapsed -31.8% into 7/23/02, advanced 20.7% into 8/22/02 and finally plunged -19.3% to its bear market low on 10/9/02, for a cumulative loss in the S&P 500 Index of -49.1%. Investors really have no sense of market dynamics if they believe that a recession-linked bear market comprises a single decline of less than 20% followed by a "V" shaped rebound into a new bull market. While I don't expect the market's losses to be nearly as severe as they were in the 2000-2002 bear market, the simple fact is that if the recent market low was indeed a final bear market trough, it occurred at the highest valuation level of any prior bear market trough in history. I don't want to convey the impression that the market cannot advance further as a result of speculative pressures, but at present, the S&P 500 remains priced to deliver probable total returns of about 2-4% annually over the coming decade (a decade ago, using the same methodology, the projected return was in the range of 0-2%, which is about what we've observed). I do not hope for a steep market decline, but it is effectively the only way for stocks to be priced to deliver meaningful long-term returns. Apart from the belief that potential losses are presently not likely to be as deep as in 2000-2002, my views about the current cycle are very much in line with the views I had following the bear market rally in January 2001, which, in hindsight, occurred very early into the downturn. Household debt now exceeds GDP for the first time in history, while total credit market debt is about 350% of GDP. Considering the rising default rates on the mortgage portion of that, and the risk that profit margin compression will endanger the debt-service coverage of marginal corporations, it's difficult to have a great deal of optimism that current difficulties will leave investors as unscathed as analysts widely suggest. The chart below (Household Debt as a percent of GDP) is courtesy of Ned Davis Research. It's not that the quantity of debt itself is particularly responsive to recessions. Rather, as the economy softens, the debt burdens tend to amplify the effect by forcing cutbacks in spending, employment and fixed investment.

Though price/volume behavior, leadership, market breadth and industry group uniformity still appear somewhat tepid, we may "soften" our hedge by covering a portion of our short call options (leaving tight put protection in place) the event that this rebound continues much further. The current price range is about where one would draw the line between a bear market rally and renewed, robust speculation. So while we'll continue to defend ourselves against the potential (even probability) of a steep and abrupt market plunge, a further push on improved internals would make us willing to risk 1-2% of assets in call options (i.e. to reduce our short call option position by that amount). My personal expectation is that we won't observe further improvement, but we don't invest on personal opinions about short-term market direction. In any event, I expect the Strategic Growth Fund to remain well-hedged against significant downside risk, even if we do soften our hedges enough to allow some modest speculative participation. Presently, the Fund remains fully hedged, and I don't expect to remove our downside protection anytime soon. In short, I continue to view stocks as being priced to deliver relatively poor long-term returns - an expectation that has clearly been borne out over the past decade, as the S&P 500 has lagged risk-free Treasury bill returns. Still, I believe that a run-of-the-mill bear market decline in the area of 30% from the highs would be enough to restore meaningful (though not breathtaking) long-term return prospects to investors. Market action continues to suggest that economic weakness may be somewhat deeper in the real sector (goods and services) than I initially expected, but I don't believe that we are likely to have a depression, or a Malthusian breakpoint, or widespread famines and energy shortages. I do recognize that many investors are bullish on the basis of commodities, fertilizer, basic materials and all sorts of scarcity-oriented investment themes. There are plenty of ways for investors to speculate on that sort of theme if they believe that "this time it's different" and we have entered a new world of permanent global shortages (no reason to convince me of it - just speculate elsewhere). As for me, I continue to believe that the best long-term investment opportunities will come from well-run companies with reasonable valuations, financial stability, and creative, useful products, just as durable long-term investment opportunities always have. So while investors clamor to buy stocks that fit into a pessimistic theme of global scarcity, famine and energy shortages, I'm frankly too optimistic to be bullish here. Market Climate As of last week, the Market Climate for stocks was characterized by unfavorable valuations and still unfavorable market action - strenuously overbought in an unfavorable Market Climate, which frequently leads to abrupt weakness. Still, but precisely because of that extended short-term strength, we have to recognize that the market is near the point where further strength could feed on itself to produce further speculation for a while. New bull market advances typically produce far more powerful price/volume and internal strength very early on, so the recent advance more closely resembles a bear market rally, albeit an extended one. In any event, we are not about to remove our downside defenses, but would be willing to place about 1-2% of assets in call options given sufficient further improvement in internals. For now, the Strategic Growth Fund remains fully hedged. In bonds, the Market Climate last week was characterized by somewhat unfavorable yield levels and unfavorable yield pressures. The Strategic Total Return Fund continues to carry a short duration of less than 1 year, mostly in Treasury bills. This is unusual, but Treasury securities of longer maturity have generally experienced negative returns as a result of recent yield increases. While I expect that we may observe another rush back toward Treasuries as safe havens in the coming months, we don't have enough abatement in yield pressures or inflation to significantly extend our maturities given the low yields-to-maturity that are available here. In precious metals, the Market Climate continues to be modestly favorable but we continue to look for opportunities to clip our exposure in this area, now at less than 10% of assets in the Strategic Total Return Fund. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |