|

|

||||||

|

|

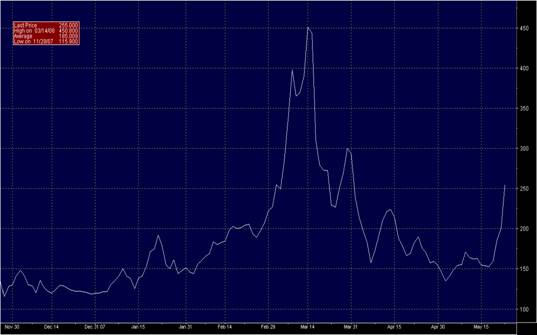

May 27, 2008 A Clue from Contango On the subject of equities, I noted last week that "if the consolidation to clear the current overbought condition is fairly shallow, it will suggest that speculation might begin to feed on itself for a while. A sharp selloff from current levels, particularly on lopsided negative breadth, would suggest that the second round of negative financial and economic news is somewhat nearer." With the Dow down over 500 points last week, and declining issues among NYSE common stocks (not composite breadth, which includes preferreds) outpacing advancing issues by 2, 3, and 5-to-1 on Tuesday, Wednesday, and Friday, respectively, we should probably brace for a second round of negative developments. In an interview published on Saturday, Warren Buffett said the U.S. economy is "already in recession." He suggested that however a recession might be defined by various economists, "people are already feeling the effects. It will be deeper and last longer than many think." Meanwhile, credit default swaps blew out last week in a manner that we haven't seen since the week before the Bear Stearns debacle. I included some of these charts a few weeks ago. The steep rise in swap spreads this week was ominous. The apparent internal deterioration of credit conditions is a stark contrast to what investors have come to believe (hope) during the relief rally since March. The stocks of many investment banks have now plunged to the same or lower levels than they were at prior to the Fed's intervention with Bear Stearns. Lehman Brothers Credit Default Swap Spread

Adding some color to the picture about Lehman Brothers, David Einhorn of Greenlight Capital noted last week that during the first quarter, Lehman took writedowns of just $200 million on a $6.5 billion portfolio of collateralized debt obligations. Yet Lehman's quarterly filing acknowledged, in a footnote, that about 25% of those CDOs were junk rated. While some investment banks have taken much larger writedowns to-date, my impression continues to be that round-two is approaching fast. Lest it appear that I'm singling out Lehman Brothers, I should emphasize that credit default swaps blew out very broadly last week, but the largest spikes were at the institutions with the highest gross leverage ratios (total assets to capital). Merrill Lynch Credit Default Swap Spread

I continue to believe that liquidity problems, delinquencies, foreclosures, writedowns, and credit defaults are still in the early innings. Martin Feldstein's recent comments should not be missed - the Fed has already committed half of its balance sheet to questionable credits, and there is little more the Fed can do to help this situation. Oil prices - a clue from contango Meanwhile, despite the prospects for fresh economic weakness, oil prices surged to fresh record highs last week on speculative momentum and increasing fears of permanent global scarcity. When investors frantically compress extreme views about the indefinite future into current prices, the bubble ends in tears more often than not. Speculative bubbles occur in financial and commodities markets because rising prices become the justification for rising prices, but there is almost always an accompanying "story" that encourages traders to transform long expectations about the future into an immediate and present urgency to buy. During the dot-com and technology bubbles of the late 1990's, for example, beliefs about rapid and long-term future growth rates for the internet were compressed into current prices, yet even though the late-stage price advances were nearly vertical (the Nasdaq gained about 50% in the last 16 weeks of the bubble), somehow investors expected continued rapid price gains from there over the long term. One would have thought that the steep losses paid by speculators would have bought at least a small lesson. But given successive bubbles in housing, private equity, Chinese stocks, and now commodities since then (all but the last which have also exacted heavy losses), it's clear that speculators have learned squat. It's understandable that speculators are easily caught up in a tendency to compress all future demand from China, India and elsewhere into current prices, but it may be helpful to remember that these countries did not simply rise out of the sea in the past year. We need only look back a year to remember that oil prices plunged from about $80 in mid-2006 to about $50 early last year. Of course, wide swings in commodities are nothing new. If you stare at a few historical commodities charts, you'll notice that commodities are particularly subject to vertical spikes and spectacular failures. Price trends in commodities often have a greater tendency to persist once they reverse, compared with equities. You might recall a striking case of that a decade ago, when crude experienced a steep plunge to just $12 a barrel. What offered a warning of the periodic plunges in oil prices during the 1990's, and even just last year? Contango. Normally, the oil futures curve is in "backwardation," which means that futures prices for distant delivery dates trade below the current spot price for oil. Occasionally though, longer-term futures trade well above spot prices, even adjusted for interest rates and cost of carry. Often a contango emerges during a period when the spot price of crude is declining - usually with a resulting acceleration in the decline (as we observed several times during the 1990's). In recent days, we've observed a contango develop between spot crude and futures expiring in 2010 and beyond, while the spreads between near-term futures have narrowed sharply and may also move into contango soon. This is worth monitoring. It is a sign that traders have accepted the bullish case so thoroughly that they have become frantic to bid up oil for delivery well into the future. Contango creates immediate incentives to buy oil for near delivery and store it in inventory. Producers don't particularly like markets in contango, because that tendency to build inventories reduces their ability to control prices through their own actions. Just as stocks tend to be poor buys in overbought markets with extreme advisory bullishness, commodities tend to be poor buys when prices have already enjoyed a parabolic speculative rise and futures move into contango (with the caveat that the last few weeks of a speculative rise can be nearly vertical, so the ultimate highs are unpredictable). A few years ago, the tendency of oil prices to increase despite a mild contango made it appear that the relationship between contango and subsequent price weakness had vanished. But as the contango steepened in 2006 and early 2007, crude plunged from about $80 to nearly $50 a barrel. I emphasize - this was just a year ago. We probably shouldn't assume that the world has suddenly changed so dramatically that the demise of fossil fuels and the extinction of mankind as a species has to be priced in by Labor Day, and then continually revised so that prices form an ever steeper parabola. While the notion of an exhaustible resource encourages traders to think in terms of exponentially rising prices, the economics of exhaustible resources are well-studied. The standard result is that if the level or growth rate of demand is generally known, the price of the commodity should tend to rise at approximately the rate of discount (i.e. about the risk-free interest rate plus a small "convenience yield") over time. When there is uncertainty, compounded by adjustment costs, there will be a range of demand shocks that will not provoke a supply response, so prices may spike temporarily in response to those shocks, but those spikes will tend to revert back to the mean. Permanent shifts in demand will of course cause permanent shifts in price levels, but temporary shocks continue to induce mean-reverting spikes and declines. Presently, we have low single-digit growth in world demand for oil which is expected to be sustained over the long-term. The main factors inducing short-term price fluctuations for oil are short-term fluctuations in demand and supply, amplified by speculation. It's clear that the oil markets are characterized by very low short-run demand elasticity (that is, price changes don't have much effect in suppressing demand), as well as low short-run supply elasticity (price changes don't immediately prompt increased supply, especially where there is not much production slack). That combination of inelasticities can certainly produce unusual price spikes over the short-term, particularly when speculators get a theme in their teeth. But it should also be clear that oil demand responds cyclically to even moderate economic weakness, and that even moderate supply responses over the intermediate term can have a significant effect on prices. It is likely that we will observe some retrenchment in demand as the global economy softens. Notably, the Shanghai stock market has plunged by about 50% from last year's highs, the Hang Seng dropped about 30% before a recent bounce, and stock markets around the world are also clearly off their highs with the exception of Brazil and Russia (due to the high weightings of resource stocks in those markets). So the signal from the equity markets is that economic weakness is not likely to be isolated to the United States. Meanwhile, the EIA estimates that non-OPEC supply will increase by roughly 600 million barrels in the coming months. I've noted before that once a speculative price run-up becomes nearly vertical, it becomes very difficult to form expectations about the final price peak, since very small changes in the date of that peak imply significant differences in the final price. Still, the combination of a developing contango in the oil futures curve, a weakening global economy, and the likelihood of a moderate but positive supply response in the months ahead makes it unlikely that oil prices will escape their cyclical tendencies beyond the summer months. In the Strategic Growth Fund, we finally closed out our oil stock positions on the price strength of recent weeks. In the Strategic Total Return Fund, we reduced our exposure to precious metals shares to just about 2% of Fund assets a few weeks ago as well. Investors wishing to maintain commodity exposure can easily establish it elsewhere. My intent here is not to open an argument with speculators about the prospects for oil and other commodities, but to communicate that we no longer hold them, and that I believe the downside risks have increased significantly in those markets. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action. The weakness we observed last week took the stock market away from the threshold where more robust speculation might have been set off, but we can't rule out a return to that area. If breadth, leadership, price/volume behavior and other market internals improve enough to indicate the possibility of speculation feeding on itself, we remain inclined to cover a portion of our short call options (while leaving the defensive put protection in place). That said, the damage last week was more consistent with the likelihood of fresh credit problems and economic concerns. While these could come from a variety of corners, I suspect that the investment banks will be among them, as may a fresh spike in new claims for unemployment. A surge in new claims typically follows an equally characteristic early-recession lull. In bonds, the Market Climate continues to be characterized by unfavorable yield levels and relatively unfavorable yield pressures. Though it appears very true that current CPI inflation would be considerably higher under prior methodologies of past decades, the trend has abated - partly because of emerging economic weakness, and partly because of a drop in monetary velocity (essentially, as people figuratively stuff money under their mattresses in a credit crisis, broad inflation tends to moderate even if the rate of money creation or commodity price pressures are fairly high). Further economic weakness coupled with widening credit spreads may again drive Treasury yields lower, but the relatively depressed starting levels leave little room for error. For that reason, the Strategic Total Return Fund continues to carry a very short duration of less than 1 year. The Fund has about 15% of assets allocated to foreign currencies, where we observed fresh appreciation against the dollar last week. In precious metals, the Strategic Total Return Fund has less than 2% of assets invested in this sector, which is about the lowest allocation since the Fund's inception. While we may see a bit of further strength in precious metals, downside risks have increased, and given the high volatility of this sector, the return/risk tradeoff has finally become insufficient, at least for now, to carry the 15-25% exposure that has been typical for us in recent years. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |