|

|

||||||

|

|

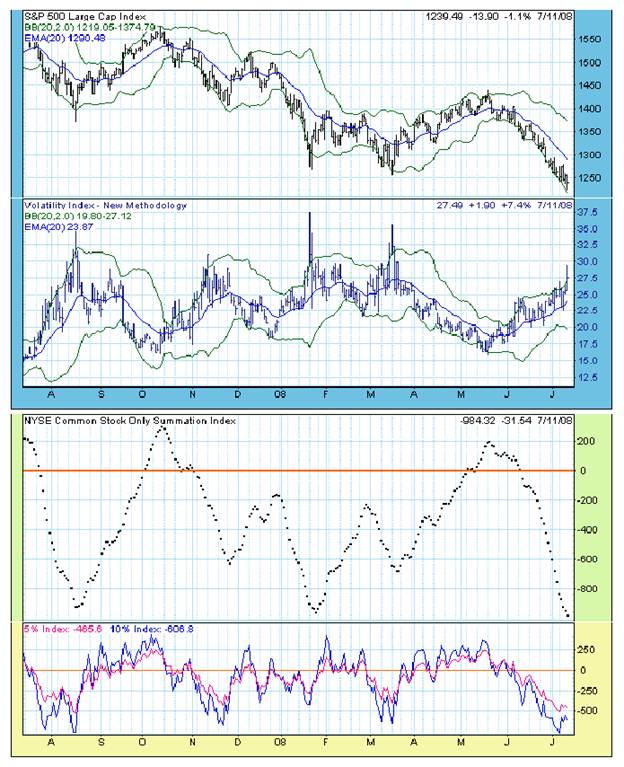

July 14, 2008 The 2% Solution To begin, I should note immediately that I have every confidence that the government sponsored mortgage securities issued by Fannie Mae and Freddie Mac are secure, as are the deposits that individuals hold at FDIC insured banks. The Treasury's reassertion on Sunday that the government stands behind those institutions should make that commitment clear. Moreover, it is important to understand that the risk to Freddie and Fannie isn't that their entire mortgage portfolio, or even a significant percentage of it, will go bust. The problem is that these companies operate on about 40 times leverage, so their shareholder capital can't provide adequate buffer for the losses. We should be careful to distinguish the stocks of financial companies from those securities that are issued with the explicit or implicit backing of the U.S. government. I do believe that many financials face heavy dilution as they attempt to rebuild capital, but I continue to believe that the primary risk is to the stocks of financial institutions, particularly investment banks, and not to the integrity of the U.S. financial system itself. With regard to Fannie Mae and Freddie Mac, it should be clear that last week's panic came as no suprise, because these institutions have always walked the tightrope on a shoestring even before mortgage defaults became an issue. A few excerpts from prior commentaries: "I don't even understand why Fannie Mae trades at all." "Now make no mistake, there is little question that bank deposits and agency debt are safely backed by the U.S. government and that this is a good commitment. However, the holders of stock in banks or mortgage companies like Fannie Mae and Freddie Mac may not be so secure. It's just excruciatingly difficult to perfectly match risky assets and liabilities at extremely high levels of leverage. Ask Long Term Capital. Indeed, were it not for accounting rules that allow Fannie Mae to keep balance sheet losses out of earnings, it would be clearer to investors that last summer's 5-month "duration mismatch" cost Fannie nearly a year of earnings. Similar derivatives-related issues are at the core of Freddie Mac's recent difficulties." "The duration gap of a financial company is equal to the duration of assets minus the duration of liabilities. For Fannie Mae to have a duration gap of -14 months means that the duration of liabilities exceeds the duration of their assets by 14 months. Since -14 months is -1.17 years, this means that a 1% drop in interest rates would cause Fannie Mae's loan portfolio to lose about 1.17% in value. Now, that doesn't sound like a lot. Until you realize that Fannie Mae has leveraged its equity 40-to-1 (the highest leverage ratio in its history), and that its annual return on this portfolio is just 0.65%. In short, a further drop in interest rates of even 0.50% here would cause an overall portfolio loss equal to about (1.17 x .50 x a leverage factor of 40 =) 23% of Fannie Mae's book value, or equivalently, about (1.17 x .50 / .65 = ) 90% of Fannie Mae's annual earnings." "As I've written many times, there are three features common to nearly every financial debacle: 1) extreme leverage, 2) a mismatch between assets and liabilities, and 3) lack of disclosure. In this regard, it's difficult to exclude Fannie Mae from concern. We don't own any stock in the company." Hussman Funds Weekly Market Comment, 2002-2003 The 2% Solution With last week's decline, the total return of the S&P 500 for the most recent 10-year period has dropped below 2.5% annually. It is now also below 2.5% annually for the past 1, 2, 3, 4, 7, 8, and 9-year periods. The only lookbacks for which the S&P 500 has exceeded 2.5% annually are the 5-year and 6-year horizons (that is, measuring from July 2003 and July 2002, which are on either side of the last bear market low). Even the total return from those points is still only about 5-6% annually. Suffice it to say that the most recent bull market has been one of least satisfactory on record from the standpoint of achieving and retaining long-term returns for buy and hold investors. That market performance was born of high initial valuations at the 2002-2003 trough, which were the richest on record for a bear market low. That rich valuation, coupled with the fact that the market's leadership in recent years has focused on cyclicals, materials, and stocks with low-quality balance sheets - has certainly made our job more challenging during this cycle. As a growth fund (not a bear fund or a market neutral fund), Hussman Strategic Growth is intended to accept a significant amount of market risk over the typical market cycle, in the expectation of achieving the full-cycle total return of the S&P 500 (due to a positive market exposure during much of the cycle), plus an "alpha" to the extent that our stock holdings perform differently than the major indices (which has been both our primary source of short-term risk and also our primary source of long-term return since the inception of the Fund). Predictably, the elevated level of valuations during this cycle hasn't produced durable rewards for investors in the S&P 500. Meanwhile, those high average valuations haven't given us nearly as much opportunity to accept market risk as we would expect over typical market cycles. Even now, the broad market continues to carry above-average valuations on the basis of normalized earnings and expected discounted cash flows. On the bright side, unless the market is currently registering its final bear market low (which I strongly doubt), my impression is that valuations will retreat enough by the eventual trough of this bear market that we will be able to expect more normal (if not extraordinary) full-cycle returns on the S&P 500 during the next market cycle, and more typical opportunities to accept market risk. While the Strategic Growth Fund continues to hold a significant hedge against further downside risk, through option combinations and moderately in-the-money index put options, market conditions are now very similar to those that have historically produced powerful bear market advances over a period of weeks or months (even if those advances failed later). In particular, valuations - though still relatively high - are no longer extreme, interest rates have shifted to somewhat more constructive trends, advisory bullishness has collapsed (a contrary indicator), and technical conditions are deeply compressed. Of course, this evidence has to be weighed against a probable continued deterioration in the balance sheets of financial companies as well as the likelihood of disappointments in earnings and earnings guidance in the coming weeks, so the overall picture is not one-dimensional. Fortunately, the relatively restrained level of option premiums (as measured by the VIX) provides us with a balanced solution to the mixed prospects of strong upside coupled with the potential for further panic. Late last week, we removed a significant portion of the short call option side of our hedges, leaving our defensive put options in place. With that shift, the Strategic Growth Fund can be thought of as still being fully hedged, but with an additional 2% of assets in call options, primarily on the S&P 500 Index. As I've noted in recent weeks, a spike in the VIX (the CBOE option volatility index) would ideally provide more confirmation of a "capitulation" in stocks from which a rebound might occur. However, we already have enough other evidence of compression to establish this small 2% "anti-hedge." Note that Friday's spike in the VIX (charts courtesy of DecisionPoint.com) was a few points short of spikes at prior selloffs during the past year, but was not entirely dissimilar. Meanwhile, our own measures of market internals, as well as a variety of popular technical measures, are also compressed. The McClellan Summation Index (a breadth based indicator) is presently at levels that match the August and January troughs. None of these are overwhelmingly reliable in and of themselves, but presently, the overall context is one of only moderate overvaluation (finally), relatively constructive interest rate trends, and moderate (if not spectacular) capitulation in market internals and sentiment.

My impression is that the somewhat restrained VIX reflects a general belief among investors that the market can't decline significantly lower, combined with a relative reluctance to actually buy stock. As a result, a) investors and hedge funds that are skittish, but not outright bearish, are willing to write call options rather than selling outright, in hopes of at least picking up some premium income, and b) investors who are interested in buying, but only at a discount, and are willing to write put options to implicitly lower their purchase costs. While we do allow for the possibility that the market could decline more deeply, the likelihood is that the current compression of prices will be cleared first. Meanwhile, the low level of option premiums allows us to have our cake and eat it too, albeit at a slight increase in our overall risk profile. You can think of our current stance as "locally long, and globally hedged." Locally long in the sense that if the market declines a few percent further, the Fund will tend to lose a bit because our call options will tend to decline more than we would expect to make up from any tendency of our stocks to outperform the market, and also in the sense that we would expect to participate at least moderately in a market rebound of more than a few percent (less than that and potential gains would be offset by time decay in the options). Meanwhile, we are globally hedged in the sense that if the market was to crash, the only difference between our current position and a fully hedged stance is that 2% of assets in call options. As soon as any crash was to bite through that 2% in calls, our position would effectively look no different from a full hedge. Compared with a fully hedged position as we've generally held in recent years, the potential downside of this position is the loss of 2% in option premium, which we would experience in the event that the market continues to decline without any recovery. The potential gain from this position is several times that amount, given the implicit "curvature" (the tendency of options to gain at a faster rate as the market advances). The Fund could lose some portion of that 2% in the event that the market remains unchanged without enough volatility to allow us to "scalp the gamma" (raise the strike price of the options after market advances and drop the strike price after market declines in a way that preserves the value of the position over time in a sideways market). As usual, the Fund may also achieve gains or losses to the extent that the stocks owned by the Fund perform differently than the indices we use to hedge. No "Buy Signals" Understand that we may be "early" from a market-timing point of view, but we are not market timers. We establish our investment positions on the basis of prevailing, observable market conditions and the average historical return/risk profile associated with those conditions. Unlike market timers, our investment position is not based on short-term forecasts about where the market is headed. We deal with observables, and averages, and probabilities, and risk management, and repeated trials, not with specific scenarios or forecasts about what will happen next week or next month. Stated differently, the shift in our hedge toward a "directional" position (preserving our downside protection and allowing upside participation, at the potential cost of 2% in time decay) is not a "buy signal" or a statement that some major turning point is at hand. Rather, it is based on the correspondence of current market conditions to those that have often produced strong risk-adjusted returns - on average - even in periods that, in hindsight, were still part of a bear market in stocks. As I've repeatedly noted, the 2000-2002 bear market contained three separate advances of 20% in the S&P 500 from intra-day low to intra-day high, and numerous smaller advances, despite the fact that the overall bear market took stocks down by half. The Strategic Growth Fund periodically established a constructive (modestly unhedged) or directional exposure during that bear market. If there was a strong likelihood that the market might be setting the final low of a bear market, if valuations were average or favorable, if a recession was fully recognized by investors, and if market action was showing significant positive divergences and constructive strength, our assessment of downside risk would be smaller and we would be closing out our defensive put options. Unfortunately, we observe none of this, and it appears unlikely that we are observing the final lows of the current bear market. For that reason, we continue to hold a significant downside defense, and we cannot and should not rule out the possibility that the market will experience significant further losses. I can't stress enough that our shift here is not a "buy signal." We are not ramping up our exposure to overall market risk, and certainly not establishing open-ended downside risk. Rather, the major shift is that we have bought in a portion of call options that we were previously short, leaving our defensive put options in place. That said, the prevailing evidence and return/risk probabilities are such that a modest 2% exposure to index call options is an appropriately constructive stance with a manageable level of risk. Market Climate The Strategic Growth Fund achieved a fresh all-time high (adjusted for distributions) on Wednesday. The Fund backed off about 1.5% from that high by the end of the week - on Thursday because of particularly concentrated weakness in consumer-related stocks, and on Friday as a result of scaling into a somewhat more constructive position late in the week. Again, the difference between our current investment position and a full hedge is that 2% of assets that we have in call options. As of last week, the Market Climate for stocks was characterized by unfavorable valuation and unfavorable but unusually compressed market action, with features that have often been associated with significant (though often short-term) advances - typically within the context of ongoing bear markets. Importantly, this evidence isn't sufficient to warrant removing our defense against further losses. In 1987, for example, the market appeared deeply oversold the week prior to the crash, only to continue lower. So oversold conditions are not in themselves sufficient evidence to establish unhedged long positions. Rather, such conditions can create the potential of having to cover hedges quickly at higher prices should market internals improve sharply, and in those cases it is appropriate to establish a "contingent asset" (in this case, call options) to hedge that "contingent liability" (the need to cover short positions but only in the event of a strong advance). The bottom line is that we remain well defended against serious downside risk, but on smaller declines or on advances, I would expect the Fund to behave locally as if it was between 10-50% unhedged. The fraction is variable because of option curvature (gamma): the Fund will tend to appear more constructive as the market rises, and more fully hedged as the market declines. In bonds, the Market Climate last week was characterized by modestly unfavorable yield levels and relatively neutral yield pressures. The Strategic Total Return Fund continues to carry a duration of about 2.5 years, primarily in Treasury securities, with just over 15% of assets in foreign currencies. We've observed a substantial widening in credit spreads in recent weeks, which I would expect to substantially reduce inflation pressures in the next few months. My impression is that given credit concerns and broadening evidence of global economic weakness, commodity strength is near the end of its run, now probably within weeks rather than months. As I noted last week, a break in commodity prices would help to reinforce any intermediate-term bear market rebound in stocks. Meanwhile, the combination of continued credit concerns along with easing commodity price pressures could support the Treasury market, despite yields that are not particularly compelling from an investment standpoint. While none of our investment positions rely on commodity price weakness, an easing of oil and food price concerns would certainly be of temporary support to stocks and bonds, even within the broader context of a bear market with potentially more damage to exact over time. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |