|

|

||||||

|

|

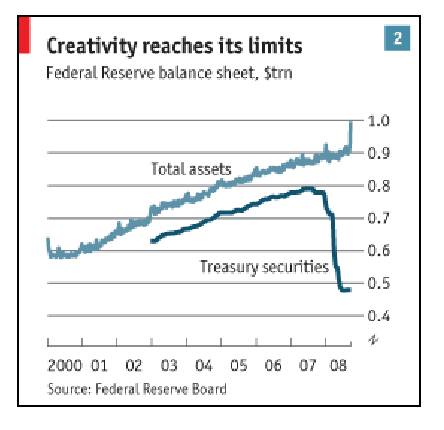

September 29, 2008 You Can't Rescue the Financial System If You Can't Read a Balance Sheet This is a bad idea. However the final legislation is written, the Troubled Assets Relief Program (TARP) being rushed through Congress will evidently be built around its single worst provision, which is that the Treasury will have authority to purchase distressed mortgage securities from U.S. financials. As I noted last week in An Open Letter To Congress Regarding the Current Financial Crisis, the sequence of bankruptcies that we've observed among U.S. financials has been almost exactly in order of their gross leverage (the ratio of total assets to shareholder equity). The reason for that is: 1) as the assets of a financial company lose value, the losses reduce the asset side of the balance sheet, but also reduce shareholder equity on the liability side; 2) as the cushion of shareholder equity becomes thinner, customers begin to make withdrawals; 3) in order to satisfy customer withdrawals, the financial company is forced to liquidate assets at distressed prices, prompting a further reduction in shareholder equity; 4) go back to 1) and continue the vicious cycle until shareholder equity goes negative and the company becomes insolvent. Let's return to the basic balance sheet of a typical financial company before the writedowns: Good Assets: $95 Liabilities to Customers: $80 Now let's write down the questionable assets - not all the way to zero, but to $2: Good Assets: $95 Liabilities to Customers: $80 This shortfall of protection on the liability side of the balance sheet is what causes a run on the institution, because once shareholder equity is gone, the only way to get at the debt to bondholders is for the company to declare bankruptcy. The concern has been that continuing bankruptcies would throw the whole financial system into disarray, especially for investment banks having lots of counterparty relationships with other institutions. But the reality is that for nearly all of these institutions, the cushion of debt to bondholders has always been more than sufficient to protect customers from losses even in the event of bankruptcy. What the financial system has needed most has been for Congress to streamline the bankruptcy process for investment banks, so that in the event of failure, the "good bank" (assets and liabilities, ex the debt to bondholders) could be cut away quickly and liquidated to an acquirer, leaving the proceeds as a residual for the bondholders. Indeed, that's exactly how it works for regulated banks. What investors overlooked in last week's panic was that we actually saw the largest bank failure in history - Washington Mutual - with absolutely no losses to customers or the U.S. government, precisely because the good bank was seamlessly cut away and sold to J.P. Morgan, wiping out shareholder equity, preferred equity, and subordinated debt, with partial repayment to the bondholders. Snap - just like that. Now, let's go back to the previous balance sheet. The Treasury plan seeks to buy up those questionable assets and thereby protect the institution against failure. Problem is, suppose the Treasury buys those questionable assets at their going value of $2. Here's the result: Good Assets: $95 Liabilities to Customers: $80 Does this transaction protect the institution against failure? No! If you buy the bad assets off the balance sheet at their market value, nothing changes on the liability side! You may have improved the "quality" of the balance sheet, but you've provided no additional capital. At best, you've allowed the bank to liquidate its assets more easily to meet continuing customer withdrawals in the vicious cycle described above. The only way that buying the questionable assets will increase capital on the liability side of the balance sheet is if the Treasury overpays for them. A better approach would be for the government to provide capital directly, in the form of a "super-bond," in an amount no greater than the debt to bondholders. The "super-bond" would be subordinate to customer liabilities, so it could be counted as capital for the purpose of capital requirements, and would be seen by customers as a legitimate cushion of protection. However, in the event of bankruptcy, it would have a senior claim in front of both stockholders and even senior bondholders. Do that, and you've actually got a mechanism to protect the financial system while at the same time protecting customers and taxpayers. Ideally, the super-bond accrues a relatively high rate of interest so that financials have an incentive to shift to private financing as soon as possible, but you would also defer the interest until the bank meets a minimal level of profitability to make sure that the financing doesn't strain the institution's liquidity. But then, Congress didn't do this because nobody thinks in terms of balance sheets. So after a nice pop to maybe 1300 or even 1400 on the S&P 500, we can expect all hell to break loose again. As a side note, a lot has been made of Warren Buffett's investment in the senior preferred stock of Goldman Sachs. But it's notable that Buffett invested in Goldman only upon the conversion of Goldman to a bank holding company, which puts it under a different regulatory structure that gives it access to the Fed window. Goldman's balance sheet has $40 billion of shareholder equity that would have to be drilled through before getting at the preferred. Evidently, Buffett believes that Goldman's asset mix is diversified enough, and light enough in mortgage assets, that Goldman won't take a major haircut on its entire (largely hedged) portfolio of assets. Buffett's investment may reflect confidence in Goldman, particularly with a government backstop on whatever questionable assets it does own, but if anything, it suggests that the government should have gone the same route - namely, provide capital in return for a financially viable security that is senior to common shareholder equity, have it accrue a relatively high rate of interest, and allow it to be repaid early (Buffett's preferred is callable by Goldman) as soon as the financial institution can secure cheaper financing. Instead, the government is taking on financially non-viable securities and warrants on common equity, while failing to improve the capital position of these financial companies at all (unless it overpays). Taxpayers will not make money here. As Congressman Scott Garrett noted to taxpayers on Sunday, "This morning we should be very much alarmed. Obviously, Washington is not listening to your wishes. Those who used to work for Goldman Sachs will support this deal. Those who have blocked reform in the past will support this deal. I will not support this deal." I couldn't agree more. This is not a good deal, because it will waste taxpayer money without addressing the fundamental solvency problems. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action. At present, however, there's not a lot to stand in the way of a violent short squeeze, particularly in financials, on the prospect of hundreds of billions in helicopter money for Wall Street. The Fund remains well hedged against substantial downside risk, but we did establish a modest "anti-hedge" on market weakness last week: an out-of-the-money index call option position amounting to about 1% of assets, not to create a significant positive exposure, but to soften our hedge in the event of a hyperactive relief rally. This is not a long position for us, and certainly not a "buy signal." It's just risk-management to provide for the contingency that investors could shift to a risk-taking preference for a while. If broad improvement in market action confirms that sort of shift, we'll allow that call exposure to go "in-the-money," which would provide the Strategic Growth Fund with a modest positive exposure to market fluctuations. Poor internal market action on any relief rally would encourage us to clip off that call option exposure or raise our strike prices to capture any intrinsic value that accrues. In bonds, the Market Climate last week was characterized by relatively neutral yield levels and modestly unfavorable yield pressures. If the legislation is passed, as appears likely, Treasury prices may be pressured lower on expectations of expanded supply, combined with potential aversion of foreign investors to hold a currency that is increasingly backed by junk. If you take a U.S. dollar out of your wallet, you'll see "Federal Reserve Note" written prominently along the top. Witness how the U.S. currency is now backed. The Treasury plan will make the situation no better. For our part, the Strategic Total Return Fund is primarily invested in short-dated Treasury securities with little sensitivity to interest rate fluctuations. The Fund also holds about 30% of assets in a mix of foreign currencies, precious metals shares, and utility stocks. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |