|

|

||||||

|

|

June 7, 2010 Extraordinarily Large Band-Aids Market internals deteriorated further last week, while valuations eased off of their recent extremes, but remain clearly elevated on our metrics. The continued combination of unfavorable valuations and unfavorable market action holds us to a fully hedged investment stance. The majority of the day-to-day fluctuation in the Strategic Growth Fund here is driven by the difference in performance between the stocks held by the Fund and the indices (S&P 500, Russell 2000, Nasdaq 100) we use to hedge. We have no inclination to buy dips here, because we have no support from either valuations nor market action. What was most surprising about Friday's "disappointing" jobs report was that it was a surprise. As I observed a few months ago in Notes on a Difficult Employment Outlook "Presently, the 4-week moving average of initial claims for unemployment is running at 468,500. This level is normally consistent with monthly payroll job losses on the order of 80,000. Against that, however, we are likely to get significant short-term job growth from census hiring, which can be expected to exert a positive impact on non-farm payrolls through mid-year. I continue to view the 4-week average of initial claims as one of the more informative series to monitor regarding the employment situation."

A 4-week average of about 400,000 - 425,000 jobless claims is roughly where we would expect to observe flat jobs growth (excluding temporary factors like census hiring). With the recent figures running closer to 450,000, the fact that we got a positive private sector number at all was something of a gift. As the stock market sold lower on the news, it was fascinating to hear several analysts saying palliatives to the effect of, "Well, some amount of month-to-month variation should be expected. Nobody expected the economy to have a 'V' shaped recovery." Excuse me, but that's precisely what the market has priced in. And that's the problem. Several weeks back, in An Update on Valuations and Forward Earnings Assumptions, Bill Hester plotted the operating profit margins that were implicitly being forecast by Wall Street Analysts (presented in red below), noting "Last October, analysts were about half way to pricing in profit margins that matched the record levels of 2007. Now, they are just about there." If this doesn't reflect the expectation of Wall Street analysts for a "V" shaped recovery, I'm not sure what does.

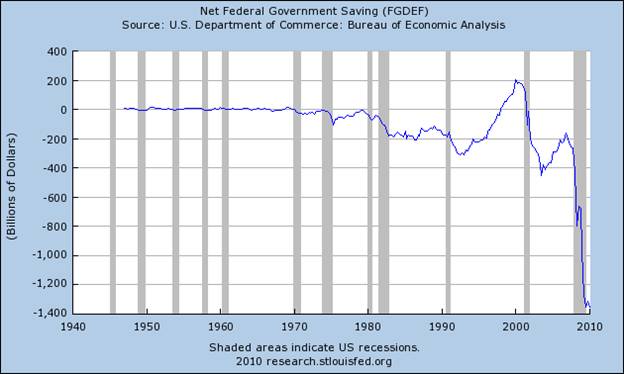

I'll reiterate that from our perspective, the essential difficulty of the market here is not Greece, it is not the Euro, it is not Hungary, and it is really not even the slow pace of job growth in the latest report. The fundamental problem is that we have not, as a global economy, accepted the word "restructuring" into our dialogue. Instead, we have allowed our policy makers to borrow and print extraordinarily large band-aids to temporarily cover an open wound that will not heal until we close the gap. That gap is the difference between the face value of debt securities and the actual cash flows available to service them. The way to close the gap is to restructure the debt. This will require those who made the bad loans to accept the associated losses. By failing to do that, we have failed to address the essential problem faced by the world, which is that we have created more debt than we are able to service. A few observations. First, I remain convinced that the other shoe to drop is not Greece or Spain or Hungary, but rather a second wave of major credit strains here in the U.S. related to fresh delinquencies from exotic adjustable rate mortgages. Second, it is a delusion to interpret economic statistics suggesting an economic turnaround over the past year without factoring out the extent to which that has been driven by unsustainable levels of deficit spending.

If you do that, you'll find that the economy has recovered to the point where the the year-over-year growth rate since early 2009 now matches the worst performance of any of 50 years preceding the recent downturn.

Third, when our policy makers insist on defending reckless lenders with public resources, we have to recognize that this is not free money. When the government issues a paper liability for real value, that real value gets directed to the recipient at the expense of countless other activities. Even seemingly costless interventions can be redistributions of wealth. For example, the strategy of dropping short-term interest rates to nearly zero as a way of increasing the interest spread earned by banks has the direct effect of impoverishing savers, very often elderly people who rely on lower risk investments for capital preservation. With regard to Fannie Mae and Freddie Mac, either the Treasury securities issued in order to cover their losses will crowd out other private investment, or the eventual inflationary effects of printing money to do so will act as an implicit tax on people with fixed incomes. As a side note, we don't hold any Fannie or Freddie liabilities in the Strategic Total Return Fund. I am still unconvinced that the Treasury's unlimited 3-year backstop was authorized or even contemplated by the 2008 HERA legislation, which is what the Treasury used as justification. A dollar spent by the government is always a dollar taken from somebody and diverted from some other activity. The only question is whether the dollar spent is more productive, or satisfies a more desperate human need, than the alternative activity would. If not, the spending is hostile to economic growth and public welfare. There is no free lunch. At best, what people call "stimulus" can only occur if the dollars spent by government are more productive than they would have been if they were allocated privately. I cannot imagine how allocating public funds to the same reckless stewards of capital that made the bad loans in the first place can possibly be a productive use of capital. All of this would be fairly moot if it we were simply talking about 2008 and 2009. However, my impression is that as the effects of last year's surge of deficit spending taper off, we will begin to observe a more accurate and generally flat reflection of underlying economic activity. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action. The Strategic Growth Fund remains fully hedged. A few side notes - when the long put / short call combinations we use to hedge have the same strike price and expiration, as our S&P 500 combinations do, the combination behaves as an interest bearing short sale on the underlying index, regardless of the level of implied volatility. Time decay is what you pay in order to get curvature (as you do with a straight call or a straight put). It's not a factor when the long put and short call options have the same strike and expiration because their time decay offsets (which is enforced by arbitrage). Also, events like the "flash crash" would only affect us liquidity-wise if we were trying to get size off in a panic. Since we're fully hedged already, and do our best to panic sufficiently before everyone else does, that's not a concern here. Given that we have modestly eased from strenuous overvaluation to still clear overvaluation, coupled with the tendency for oversold markets to become wickedly oversold in their early stages, we have no inclination to "buy dips" here either, though we might place a percent or two of assets into out-of-the-money call options (as a contingency against a brief short squeeze) if the market was to drop precipitously. From my perspective, we remain in the eye of the hurricane here, which we have expected for some time. Suffice it to say we remain very cautious. In bonds, the Market Climate last week was characterized by moderately favorable yield levels and favorable yield pressures. Given that commodity weakness often emerges in response to concerns about economic weakness and deflation (both which we may observe in the months ahead), our inclination is to gradually expand our exposure to precious metals shares on weakness where possible. Though longer-term inflationary prospects are quite hostile, they are in no way close at hand in my view, and my impression is that it has generally been difficult for investors to maintain a long-term thesis in the face of contradictory shorter-term pressures. So our intermediate-term position leans toward a modest (3-4 year) duration in Treasuries, and a moderate (5-10%) exposure to precious metals shares, while our longer-term expectation will most likely favor a greater allocation to TIPS and other inflation-hedges, with a tendency to accumulate on (possibly significant) weakness. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |