|

|

||||||

|

|

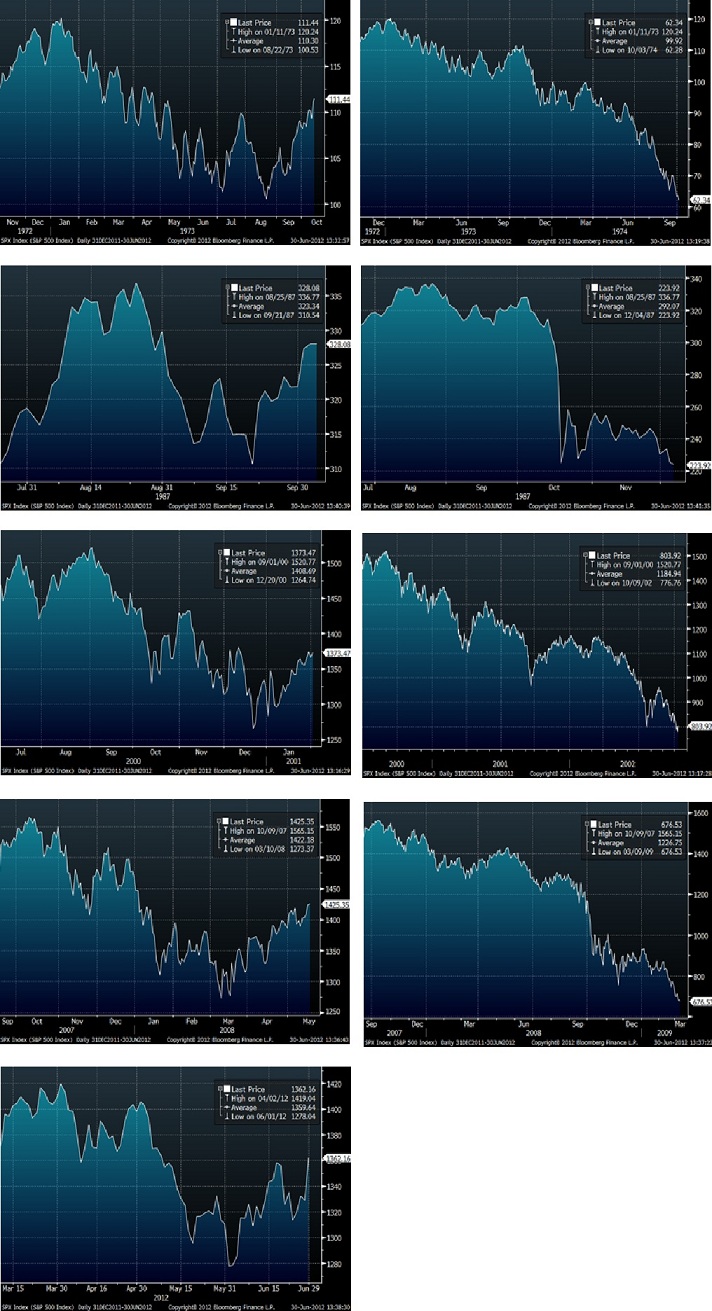

July 2, 2012 Anatomy of a Bear In the first week of March, the U.S. stock market established a set of conditions placing it among the most negative 2.5% of historical observations (see Warning: A New Who’s Who of Awful Times to Invest) – a short list that includes the major peaks of 1972-73, 1987, 2000, and 2007. Since then, we’ve seen an increasing set of indicator syndromes that are associated with historically hostile market outcomes, maintaining us in a hard-defensive stance that is as rare as it is imperative. Last week, the market reconfirmed the “exhaustion syndrome” that I discussed several months ago (see Goat Rodeo). Prior to 2012, there were 112 weeks in post-war U.S. data where our investment strategy would have encouraged a similarly defensive position with that syndrome in place. Following those instances, the S&P 500 plunged at an average annual rate of -47.5%. The trend-following components of our market action measures remain negative here, but it is important to note that those components are moderately – probably a small number of positive weeks – away from an improvement that could shift us from such a tightly defensive stance. While our outlook would not become bullish by any means, this shift would rein in the “staggered strike” put option hedges we presently hold in Strategic Growth. These positions (which raise the strike prices on the long-put portion of our hedges) seek to improve performance during market plunges, but make us vulnerable to the loss of put option premium during “risk on” advances such as we saw last week. That is uncomfortable even if the puts only represent a very small percentage of assets (as they do here). Suffice it to say that we are most likely a single number of weeks away from either substantial market losses, or enough stabilization in market action to ease our defensiveness. In any event, we will not maintain our present stance indefinitely. So far, hopes for massive bailouts and monetary interventions have allowed the market to forestall the more violent follow-through that it experienced in 1973-74, 1987, 2000-2002 and 2007-2009 from similar conditions. Yet the market impact from various monetary actions has become progressively weaker, and the exuberance from various “agreements” out of Europe has become progressively shorter. More importantly, in data spanning more than a century, including Depression, two world wars, rapid inflation, credit crisis, and numerous bubbles and crashes, we’ve seen that relevant global events show up in observable data such as market action, credit spreads, valuations, economic indicators, sentiment, and specific syndromes of conditions. As a result, we don’t need a “Euro breaks up” indicator, or a “Bernanke bubble factor” in our data set, nor do we need a live feed showing constantly refreshed CT-scans of Angela Merkel’s spine. When the observable data shifts, so will our investment stance. We certainly struggled in 2009 and early 2010 to ensure that our methods were robust to Depression-era data, and the repeated bouts of monetary intervention have narrowed our criteria for establishing staggered-strike hedges, becoming more sensitive to trend-following factors than was necessary prior to 2009. The past few years would have been more comfortable if these adaptations had not been necessary, but they also leave us well-prepared to weather a broad range of potential outcomes, in the expectation of returns that resemble what we’ve achieved in other complete market cycles (e.g. peak-to-peak 2000-2007, trough-to-trough 2002-2009). Both the internet bubble and the housing and credit bubble offered plenty of temptation to believe in a “new era” where historically important market factors were irrelevant. The same temptation exists today despite accelerating global economic challenges. We remain just as unwilling to shift our investment discipline away from testable evidence, or to rely on a blind faith in policymakers to make risk simply go away. Anatomy of a Bear Last week, the market re-established the “exhaustion syndrome” that we observed several months ago. The associated rally was uncomfortable, not only because banks and financials advanced (where we hold very little exposure), but also because the advance took our staggered strike put option hedges from in-the-money to out-of-the-money while the CBOE volatility index dropped to just 17. It is easy to forget that we experienced much the same thing near the 2000 and 2007 market peaks. As I noted in the March Who’s Who piece: “A word of caution... When we look at longer-term charts like the one above, it's easy to see how fleeting the intervening gains turned out to be in hindsight. However, it's easy to underestimate how utterly excruciating it is to remain hedged during these periods when you actually have to live through day-after-day of advances and small incremental new highs that are repeatedly greeted with enthusiastic headlines and arguments that ‘this time it's different.’ For us, it's particularly uncomfortable on days when our stocks don't perform in line with the overall market, or when the ‘implied volatility’ declines on our option hedges.” Though our level of defensiveness will remain sensitive to any improvement in our measures of market action, my opinion remains that the global economy is entering a new recession, and that stocks are already in the beginning of a bear market. Because bull and bear markets can only be confirmed in hindsight, we prefer in practice to focus on the broad set of observable evidence at every point in time. Our investment stance is based on that evidence, not my views about recession or bear market status. As veteran market analyst Richard Russell has noted, investors often equate the concept of a bear market with the expectation that prices will continuously fall. Indeed, if you think back to the 2000-2002 bear, or the 2007-2009 bear, that is probably the memory that those bear markets invoke. In fact, however, those bear markets can be seen on a smaller scale as a constant process of hope and disappointment, with periods of risk-seeking abruptly punished by fresh waves of risk-aversion. This can make it very difficult to live through a bear market day-after-day with a clear sense of the larger picture. In an attempt to reinforce this picture, the following charts present the initial the 1973-74, 1987, 2000-2002, and 2007-2009 bear markets, respectively. For each period, the initial portion of the bear market is on the left side, while the complete decline is on the right side. Those complete declines represented market losses of about 50% from the highs, except for 1987 which was more abrupt but somewhat less extensive. The final chart shows the S&P 500 from early March through last week. Notably, each of those previous bears started from conditions that match the “Who’s Who” syndrome we observed in March of this year. The feature to notice about these early bear markets is that in each case, despite a hard initial decline, the market recovered within a few percent its bull market high at some point between 2-9 months after the bear market had already started. In effect, investors mounted an “exhaustion rally” despite already deteriorating market internals and rich valuations.

Past performance is not indicative of future results. That said, the unusually bad outcomes of similar historical precedents help to convey why we retain such a durable sense of doom, even after last week’s scorching “risk on” advance. Again, a moderate continuation of constructive market action would likely be sufficient to move us to soften our presently hard defense by retreating from a “staggered strike” option hedge. At present, conditions remain aligned with those that have preceded some of the most negative consequences in market history. On Europe’s Plan to Have a Plan to Have a Memo of Understanding The following is Friday’s statement from the EU (emphasis added): “We affirm that it is imperative to break the vicious circle between banks and sovereigns. The Commission will present Proposals on the basis of Article 127(6) for a single supervisory mechanism shortly. We ask the Council to consider these Proposals as a matter of urgency by the end of 2012. When an effective single supervisory mechanism is established, involving the ECB, for banks in the euro area the ESM could, following a regular decision, have the possibility to recapitalize banks directly. This would rely on appropriate conditionality, including compliance with state aid rules, which should be institution-specific, sector-specific or economy-wide and would be formalised in a Memorandum of Understanding. The Eurogroup will examine the situation of the Irish financial sector with the view of further improving the sustainability of the well-performing adjustment programme. Similar cases will be treated equally. “We urge the rapid conclusion of the Memorandum of Understanding attached to the financial support to Spain for recapitalisation of its banking sector. We reaffirm that the financial assistance will be provided by the EFSF until the ESM becomes available, and that it will then be transferred to the ESM, without gaining seniority status. “We affirm our strong commitment to do what is necessary to ensure the financial stability of the euro area, in particular by using the existing EFSF/ESM instruments in a flexible and efficient manner in order to stabilise markets for Member States respecting their Country Specific Recommendations and their other commitments including their respective timelines, under the European Semester, the Stability and Growth Pact and the Macroeconomic Imbalances Procedure. These conditions should be reflected in a Memorandum of Understanding. We welcome that the ECB has agreed to serve as an agent to EFSF/ESM in conducting market operations in an effective and efficient manner. “We task the Eurogroup to implement these decisions by 9 July 2012.” The upshot here is that Spain’s banks are undercapitalized and insolvent, but rather than take them over and appropriately restructure them in a way that requires bondholders to take losses instead of the public, Spain hopes to tap European bailout funds so that it can provide capital directly to its banks through the European Stability Mechanism (ESM), and put all of Europe’s citizens on the hook for the losses. Spain has been trying to get bailout funds without actually having the government borrow the money, because adding new debt to its books would drive the country further toward sovereign default. Moreover, institutions like the ESM, the ECB, and the IMF generally enjoy senior status on their loans, so that citizens and taxpayers are protected. Spain’s existing bondholders have objected to this, since a bailout for the banks would make their Spanish debt subordinate to the ESM. As a side note, the statement suggests that Ireland, which already bailed its banks out the old-fashioned way, will demand whatever deal Spain gets. So the hope is that Europe will agree to establish a single bank supervisor for all of Europe’s banks. After that, the ESM - Europe’s bailout fund - would have the “possibility” to provide capital directly to banks. Of course, since we’re talking about capital – the first buffer against losses – the bailout funds could not simply be lent to the banks, since debt is not capital. Instead, it would have to be provided by directly purchasing stock (though one can imagine the Orwellian possibility of the ESM lending to bank A to buy shares of bank B, and lending to bank B to buy shares of bank A). On the question of whether this is a good idea, as opposed to the alternative of properly restructuring banks, ask Spain how the purchase of Bankia stock has been working out for Spanish citizens (Bankia’s bondholders should at least send a thank-you note). In any event, if this plan for a plan actually goes through, the bailout funds – provided largely by German citizens - would not only lose senior status to Spain’s government debt; the funds would be subordinate even to the unsecured debt held by the bondholders of Spanish banks, since equity is the first thing you wipe out when a bank is insolvent. It will be interesting to see how long it takes for the German people to figure this out. Market Climate It bears repeating that our present defensiveness is not a reflection of European concerns or even our view that the U.S. economy is entering a recession. We try to align our investment position with the prospective return/risk profile that we estimate on the basis of prevailing market conditions, and those conditions are what keep us tightly hedged here. As noted earlier, a moderate further recovery in market internals would move us to reduce the tightness of our hedge, though it’s fair to say that the required improvement is not simply a stone’s throw away and would likely require at least a small number of positive weeks. Here and now, present conditions remain among the most negative in history from a prospective return/risk standpoint. Strategic Growth Fund remains tightly hedged, with a staggered strike position where the additional put option premium at risk represents about 1.8% of total assets. Strategic International also remains fully hedged, and Strategic Dividend has nearly 50% of its stock holdings hedged (its most defensive stance). Strategic Total Return continues to carry a duration of about one year, with about 14% of assets in precious metals shares, and a small percentage of assets in utility shares and foreign currencies. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |