|

|

||||||

|

|

November 5, 2012 Stream of Anecdotes Is the economy at an inflection point, or are we simply in the calm before the storm? Though economic reports have been relatively muted on balance, they have also come in somewhat above expectations in recent weeks – particularly the advance estimate of third quarter GDP at 2%, and October non-farm payrolls at 171,000. The lack of clear deterioration in recent reports begs the question of whether this is enough to dispose of any concern about recession, and instead look forward to continued positive – if slow – economic progress. The answer to that question largely depends on how one draws inferences from economic data. The consensus of Wall Street economists, as well as the broader economic consensus, has never successfully identified a U.S. recession until well after it has begun. I believe that much of the reason is that economists tend to interpret reports one-by-one as what I’ve called a “stream of anecdotes.” From that perspective, a series of positive anecdotes, such as the reports we’ve recently seen on GDP and non-farm payrolls, encourages views that the economic landscape is all clear. The problem is that the stream of anecdotes approach places no structure on the data – there is no analysis of leading/lagging or upstream/downstream relationships, no examination of the frequency and size of revisions to the data – particularly around economic turning points – and no attempt to place the data points into a larger “gestalt” that captures relationships between dozens of other economic reports. Moreover, it's natural for analysts to gauge “trends” by comparing recent reports to past data, with a look-back horizon somewhere in the range of 13-26 weeks. If analysts then form expectations by extrapolating recent surprises, it then becomes very easy to produce regular “cycles” of economic surprises. We’ve been able to generate that phenomenon even using randomly generated data. In practice, the cycle of economic “surprises” tends to run about 44-weeks in U.S. data (see The Data Generating Process). As it happens, much to the chagrin of conspiracy theorists, we would expect the present cycle to peak out roughly the week of the election. In any event, a series of positive economic surprises can easily be interpreted as an important inflection point. Looking deeper into the data, however, we really don’t see the sort of broad, persistent strength in economic reports or leading indicators that would indicate a significant shift in economic fundamentals. To the contrary, we continue to believe that the U.S. entered a recession last quarter and that some of the more prominent data points (GDP, non-farm payrolls) will be revised downward within several quarters, as we’ve regularly seen around economic turning points throughout history. The regular pattern of revisions around economic turning points has also been emphasized by ECRI, which uses much different methods than we do, but shares our concerns about recession risk. We could hardly choose better company on this particular deserted island. To recap this pattern of data revisions around recession turning points, note that in the originally reported data for May through August 1990, as a new recession was emerging, the Bureau of Labor Statistics reported that 480,000 total jobs were created (see the October 1990 vintage in Archival Federal Reserve Economic Data). But in the revised data as it stands today, those figures have been revised to a loss of 81,000 jobs for the same period. Consider early 2001. A U.S. recession had already started months earlier, but first-quarter GDP growth was initially reported at 1.2%. Based on final revision, that same quarter’s GDP growth is now reported at -1.3%. The vintage data shows that non-farm payrolls were initially reported with a gain of 105,000 jobs during January-April 2001, while the revised data now shows a loss of 262,000 jobs. Likewise, by early 2008, the U.S. was also already in recession, but first-quarter GDP growth was initially reported at 1% growth. That figure was only later revised to -1.8%. The non-farm payroll reports were already deteriorating, with a cumulative job loss from February-May of 2008 of 248,000 jobs. Still, those initial reports pale in comparison to the revised figures, which presently show a loss of 577,000 jobs for the same period. As for the latest employment figure, my impression is that we will ultimately see revisions that put non-farm payroll growth at negative figures from about September 2012 onward. That said, I should emphasize that this tendency for data revisions around economic turning points should not be viewed as evidence of any kind of manipulation. In my view, the October payroll report doesn’t support the notion that the numbers are rigged in any way. It’s just that all of this data is based on limited surveys, and is heavily smoothed with algorithms that adjust the data by enormous amounts compared with the actual monthly changes that are reported. For example, over the past year, the average monthly change in total non-farm payrolls has been 162,000. That’s all well and good, but it should at least be understood that the average monthly seasonal adjustment, in absolute terms, has been 840,000 jobs (the smallest being a negative adjustment of 14,000 jobs in April, and the largest being a typical upward January adjustment that came to 2,164,000 jobs. Such enormous adjustments are not unusual at all. It should be clear that last month’s “beat” of 45,000 jobs versus Wall Street’s expectations is not cause for particularly strong conclusions, in a month where the seasonal adjustment itself exceeded 1,000,000 jobs. Examining the full set of available data, I continue to maintain the view that a U.S. recession is already in progress. Below, I’ve updated our summary of regional and national surveys from the Federal Reserve and the Institute of Supply Management (ISM), including the employment component of those reports. The chart below presents this data in standardized form (mean zero, unit variance) to make the various surveys comparable. Notice that the employment components of these surveys have generally been very strong since the recession. That may seem counter-intuitive given that the labor market has not been particularly robust in recent years, but remember that this is survey data, so the benchmark is whether conditions are getting “better” or “worse.” The strength of the employment component in recent years is therefore partly a reflection of how bad conditions became during 2009, after which nearly anything could easily be graded as an improvement. Nonetheless, note that the employment component has been plunging in recent months, bringing it closer to the already weak headline, new-orders, and order backlogs components.

The next chart averages all of the above components, and compares the resulting average with the growth in non-farm payrolls over the subsequent quarter. Notice that after a brief improvement in the September data, the average of these indices deteriorated sharply in October, to a fresh low in the combined data. The average standardized value is now at the worst level since the last recession, and is at a level that has generally been observed near the beginning of prior recessions. Still, although this particular indicator has ideal “sensitivity” in that it captures every recession, it doesn’t have flawless “specificity” in that there are a few cases where similar readings have occurred without a recession in progress. On a broader reading of economic evidence, including a European recession clearly in progress and recessionary signals from our unobserved components models (which use leading/lagging relationships inferred from dozens of economic indicators such as real income growth, consumption, GDP, employment, survey data, industrial production, and so forth), my impression remains that the present deterioration should be taken seriously.

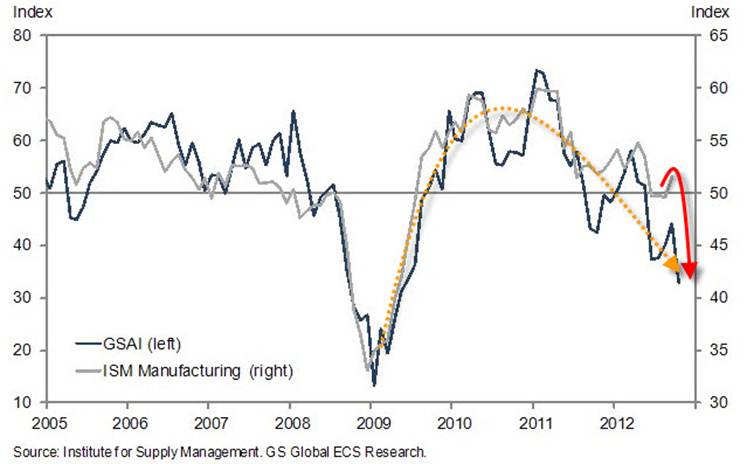

The deterioration in economic internals is consistent with the weakness that is evident based on company-by-company measures of business activity. While U.S. companies reported broad earnings misses in the latest round of quarterly reports, it’s worth observing that a reported earnings “miss” is actually measured relative to the analyst estimates that existed immediately prior to the report, and those estimates were brought down sharply just before earnings season started. The misses were even worse in comparison to estimates that were available even a few weeks earlier. The same was true for revenues, where the misses on the revenue side were worse than for earnings. Goldman Sachs (h/t Zerohedge) constructs a bottom-up, firm-by-firm measure of economic activity called the Goldman Sachs Analyst Index (GSAI), that summarizes data based on new orders, sales/shipments, employment, and other components, including both service and manufacturing industries. The latest report notes “Compared to other business surveys such as the Philadelphia Fed or Chicago PMI [Purchasing Manager’s Index], the GSAI sends a more pessimistic bottom-up message and suggests downside risks to the ISM. In addition to the headline index, most of the underlying components of the GSAI also fell sharply... The sharp reversal in the sales, new orders, and orders-inventories gap measures suggest that the broad improvement in September was likely transient, and that activity and demand will likely remain depressed.”

In summary, analysts who interpret economic data as a stream of unconnected anecdotes are likely to find recent data encouraging, and will easily dismiss any concern about a U.S. recession on that basis. For our part, the internals of the economic picture – new orders, backlogs, real income growth, and even the employment components of prominent economic surveys – continue to deteriorate. Based on dozens of economic variables and methods that account for leading/lagging relationships (e.g. unobserved components estimates) our view remains that the U.S. economy has already entered a recession. We are certainly open to changing that view in the event that we observe a broad and sustained firming in leading economic measures, particularly those that are broadly based on orders, production, sales and income. But at present, those measures remain generally weak, and their direction remains flat to down (though the bright spot is that they are not collapsing as they did in 2008), while the employment-related measures have deteriorated significantly. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes As of last week, our estimates of prospective return/risk in stocks remained significantly negative. Bond yields remain depressed, and while I expect that economic weakness will benefit long-maturity Treasury securities, yields are already so low that investment positions taken on that view would be largely speculative and would rely on a precise exit. The yield-to-maturity on long-dated Treasury securities remains terribly inadequate, in my view. Meanwhile, the yield on the Dow Jones Corporate Bond Index, at 2.61%, has never been lower. I believe that the tendency of investors to reach for yield in credit-sensitive securities – however strongly encouraged by Federal Reserve policy – is likely to be punished in an economic downturn even if Treasury yields decline. Corporations may be cash-rich, but many are also debt-heavy, and one cannot cheer the asset without considering the liability. On the commodity front, though I continue to expect significant inflation pressures in the back-half of this decade, my expectations of weakness in both the global economy and the financial markets (ex-Treasuries) sustains the concern that we could see general weakness in gold and gold equities on broader economic pressures. While our estimates of prospective return/risk in precious metals shares are positive, they are also fairly muted relative to the risk here. Strategic Growth Fund remains fully hedged, with a staggered-strike position where the index put side of our hedge is about at-the-money based on current levels in the S&P 500. With the CBOE volatility index at about 17% and our prospective return/risk measures deeply negative, I continue to expect greater volatility in the market (particularly to the downside) than is reflected in option premiums here. We would expect this position to bolster our hedge against market weakness, but to experience some loss of time-premium in the event of a flat or advancing market. As a result of recent market weakness, this position is now fluctuating between 2-3% of assets, extending out to 2013. Of course, we continue to look for good opportunities to shift strike prices when our put hedges go significantly “in the money”, and to reduce or eliminate those positions on improvements in the expected return/risk profile. Meanwhile, Strategic International remains fully hedged, Strategic Dividend Value is hedged at about 50% of the value of its stock holdings, and Strategic Total Return continues to carry a duration of less than 2 years (meaning that a 100 basis point move in interest rates would be expected to impact the Fund by less than 2% on the basis of bond price fluctuations, with less than 5% of assets in precious metals shares at present.--- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |