|

|

||||||

|

|

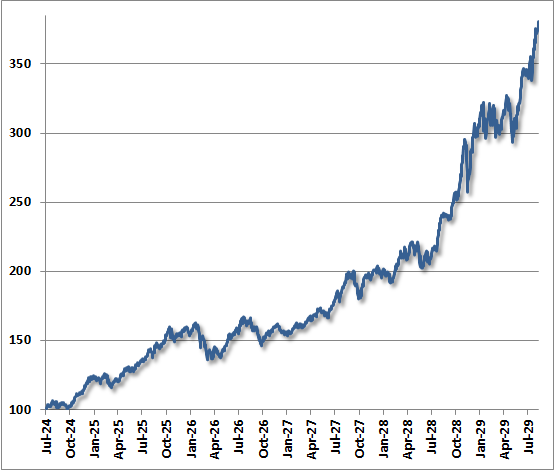

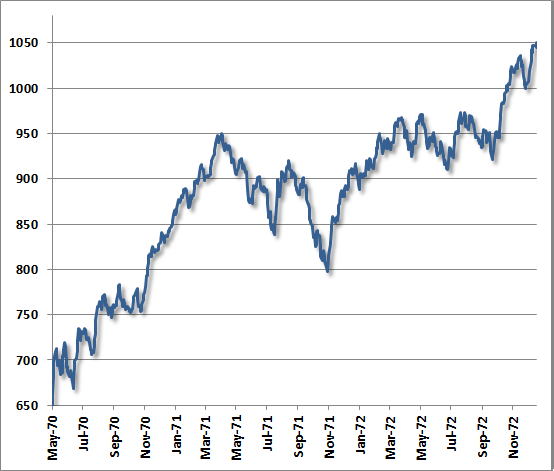

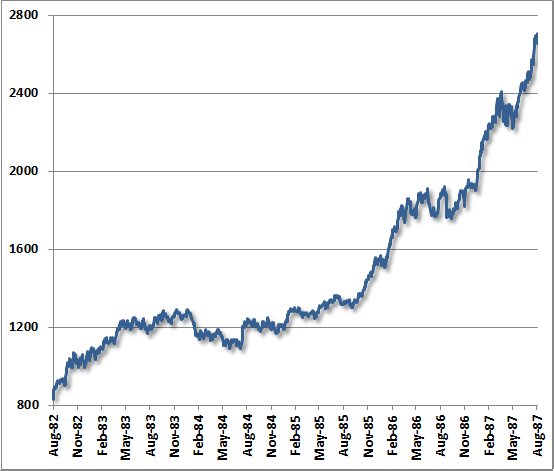

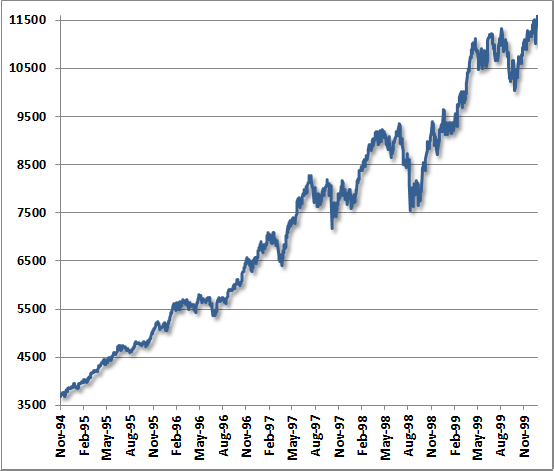

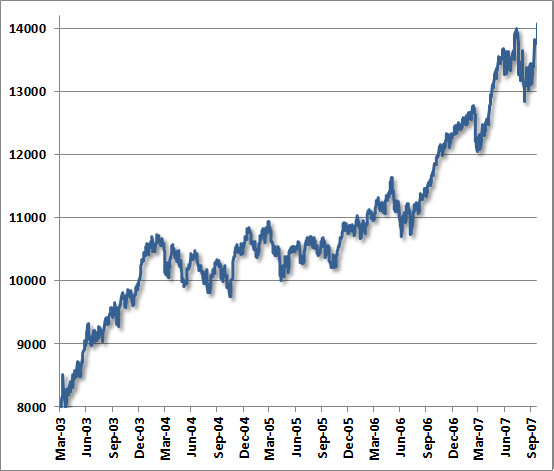

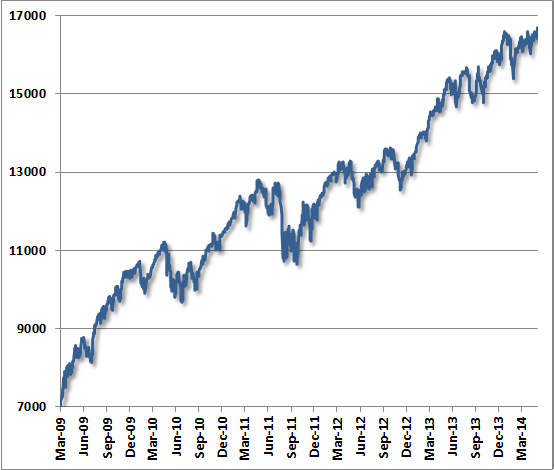

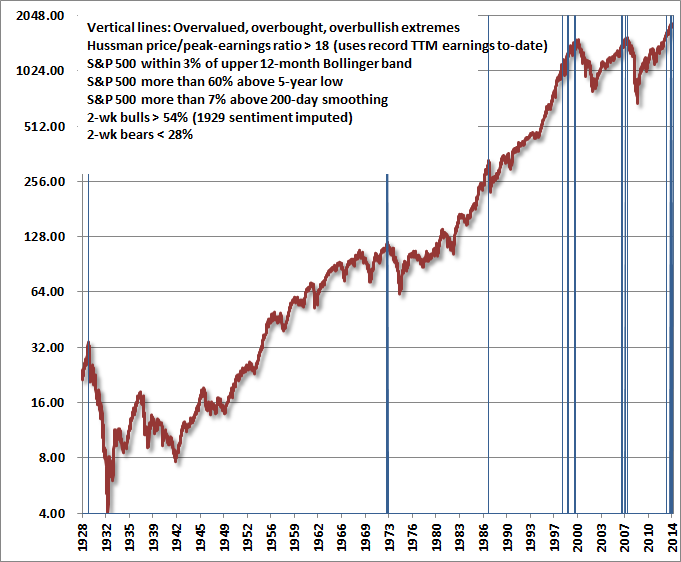

May 19, 2014 The Journeys of Sisyphus “The gods had condemned Sisyphus to ceaselessly roll a stone to the top of a mountain, whence the stone would fall back of its own weight. At the very end of his effort measured by skyless space and time without depth, the purpose is achieved. Then Sisyphus watches the stone rush down in a few moments toward that lower world whence he will have to push it up again toward the summit. If this myth is tragic, that is because its hero is conscious. Where would his torture be, indeed, if at every step the hope of succeeding upheld him? ... Sisyphus, proletarian of the gods, powerless and rebellious, knows the extent of his wretched condition: it is what he thinks of during his descent.” Albert Camus After little more than a year of legitimate revaluation of equities following the 2007-2009 credit crisis, and more than three years of what will likely turn out to be wholly impermanent – if dazzling – Fed-induced speculation, investors have again pushed the stone to the top of the mountain. Despite the devastating losses of half the market’s value in 2000-2002 and 2007-2009, investors experience no fear – no suffering as a result of present market extremes. There is no suffering because at every step, as Camus might have observed, “the hope of succeeding” upholds them. As we discussed several months ago, that hope of succeeding rests on what economist J.K. Galbraith called “the extreme brevity of the financial memory.” Part of that brevity rests on ignoring the forest for the trees, and failing to consider movements further up the mountain in the context of how far the stone typically falls once it gets loose. It bears repeating that the average, run-of-the-mill bear market decline wipes out more than half of the preceding bull market advance, making the April 2010 S&P 500 level in the 1200’s a fairly pedestrian expectation for the index over the completion of the current market cycle. A decline of that extent wouldn’t bring valuations close to historical norms, and certainly not to levels that would historically represent “undervaluation.” But consider that a baseline expectation, and don’t be particularly surprised if the market loses closer to 38% - which is the average cyclical bear market loss during a secular bear market period. A market loss of about 50% would put historically reliable valuation metrics at their historical norms, though short-term rates near zero would seem inconsistent with a move to historically normal valuations with typical (~10% annual) expected total returns, absent other disruptions. The simple fact is that the completion of the present market cycle might be better, or it might be worse than historic norms. We know that we don’t want to speculate here in any event, but neither a severe market loss nor a move to “undervaluation” is a requirement for us to encourage market exposure. For our part, we would expect to shift to a significantly constructive position on a meaningful retreat in valuations – even if to still-overvalued levels – coupled with an early improvement in key measures of market internals. The charts below display various journeys of Sisyphus - a chronicle of multi-year, increasingly speculative market advances that terminated in the same set of conditions that we presently observe. The charts show only the advance to the highs. So for example, the chart below of the advance to the 1929 high does not feature the 85% market plunge that followed, the chart for 1987 does not feature the subsequent crash, and the charts ending in 1972, 2000 and 2007 do not feature the 50% market plunges that followed. Then of course, there is the chart through last week which, we are assured, is entirely different from the others. Examine these charts carefully, and ask yourself if you would have had any less confidence in the “strength” and “resilience” of the market at these pinnacles than investors appear to have today. We can view the journeys of Sisyphus in these charts with an understanding of why investors felt no discomfort, despite the fact that they were about to lose a significant fraction of their assets. As Camus asked, “Where would his torture be, indeed, if at every step the hope of succeeding upheld him?”

Is this time materially different from 1929, 1972, 1987, 2000, or 2007? We doubt it. In the chart of overvalued, overbought, overbullish extremes below, I’ve replaced the Shiller P/E (which is a lightning rod) with a variant that I introduced in the 1990’s, basing the P/E multiple on the highest level of trailing earnings observed to-date – surely an optimistic and forgiving measure today given that profit margins are about 70% above historical norms, but one that signals rich valuation regardless. We certainly can’t rule out movements further up the mountain (though to us, 2013 was largely a replay of 1999), but those movements are likely to appear small in the context of what will be erased over the completion of the cycle.

Despite the inevitability of the descent of Sisyphus’ stone following these peaks, that inevitability should be the source of great optimism – not for current opportunities, but for future ones. Those with fidelity to informed discipline need only remain in the present moment, responding to the evidence as it changes, without needing to judge advances or declines as fortunate or unfortunate. The benefits of that discipline emerge over the course of the cycle even if some events seem unwelcome. Likewise, the existentialist Camus understood the cycle of things, and properly recognized the value of even the descent, without needing to judge it as tragic: “If the descent is thus sometimes performed in sorrow, it can also take place in joy. There is no sun without shadow, and it is essential to know the night. I leave Sisyphus at the foot of the mountain! One always finds one’s burden again. But Sisyphus teaches the higher fidelity that negates the gods and raises rocks. The struggle again toward the heights is enough to fill a man’s heart. One must imagine Sisyphus happy.” Instant Karma I’m sometimes viewed as an evil quant, sitting in a dimly lit room, stroking a hairless cat ironically named Mr. Whiskers, and hoping for the worst. That’s undoubtedly because of my view that all of the market’s gains since roughly April 2010 are likely to be wiped out in a rather ordinary completion to the present market cycle, coupled with my broader criticisms of Fed-induced speculation and other ill-conceived policies. If you’ve been with us for a while, you know that I take no joy in market plunges, and my adamant concern about severe losses this time around reflects an extreme discomfort with having been right about the other two 50% losses in recent memory (not to mention becoming constructive in-between, though my fiduciary stress-testing inclinations in 2009 clearly did us no good in the face of QE – see Setting the Record Straight for the full narrative). Some also have the impression that our objective is to talk the markets down, in a way that interferes with their bullish outlook. The reality is this. While we certainly hope to provide evidence and data sufficient for disciplined investors to maintain their confidence in our full-cycle approach, we have no particular desire to convert disciplined buy-and-hold investors or reckless speculators to our views (though I do think “buy-and-hold” investors with horizons shorter than 7-10 years have poorly matched their strategy with their objectives). Meanwhile, given that the majority of my income is directed to charity, I have a rather vested interest in doing good for others over time (undoubtedly, my particular focus on finance and autism research demands unusual patience, long horizons, a deep respect for evidence, and no expectation that progress evolves smoothly). Yet as much as we focus on the long-term good, equilibrium creates an unfortunate constraint: by encouraging one investor to defend their financial security by selling overvalued stocks, the result is that someone else must end up buying the stock at these same levels. That poor soul, we expect, is likely to be worse off for the trade. That may explain my philosophical aversion to speculating in steeply overvalued markets, and my ethical objection to policies like quantitative easing that encourage it. In order to profitably exit that speculation, someone else must be guaranteed misery. In a financial market where price signals encourage savings to be allocated toward productive uses, what helps an individual investor often helps the entire economy. But in a severely distorted and speculative market, any effort to help one investor is really quite a zero-sum game that requires someone else to be injured. This is just an unhappy result that years of quantitative easing have now foisted upon us. Accordingly, I am changing my guidance. For those investors who trust our analysis and discipline, no change of course is encouraged. But for those who find our work to be a constant source of irritation to be regarded with open disdain, I am retracting all of it herewith – for you alone mind you – and I leave you free to buy with both hands to whatever extent you are inclined. Not that I encourage it really – that would be bad Karma – but someone is going to have to hold equities at these prices. It would best be those who are fully aware of our concerns and prefer to reject them. So the more you dislike my work, and particularly if you are nasty about it, I have no objection to you accumulating – perhaps on margin – as much stock from other investors as possible. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes The Hussman Funds maintain a defensive stance toward stocks, with a moderately constructive stance toward precious metals and Treasury securities. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |