|

|

||||||

|

|

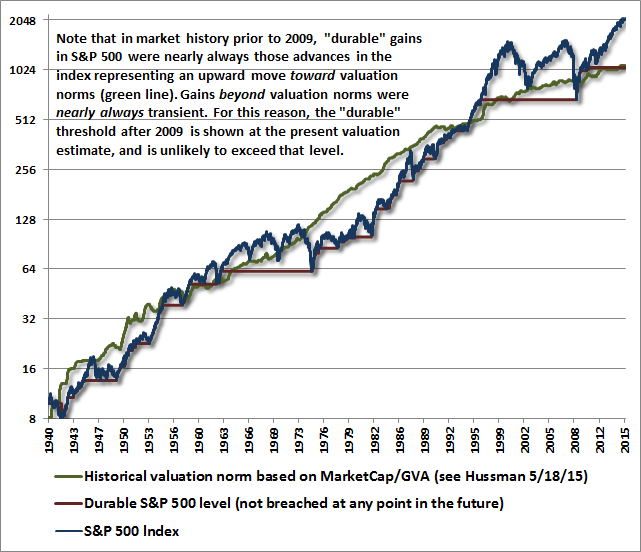

June 29, 2015 Durable Returns, Transient Returns Over the course of three speculative bubbles in the past 15 years, I’ve often made the distinction between “durable” investment returns and transient ones. At any point in time, the cumulative long-term return of the stock market equals the gain that investors can reasonably assume will be durable (in that it is unlikely to be surrendered in the future), plus whatever market gain investors should assume will be entirely wiped out over the course of the present or future market cycles. As it turns out, those two components can be identified with surprising accuracy. We can understand the distinction between durable gains and transient gains by inspecting market history and asking this question: was the prevailing level of the stock market (or its cumulative total return) observed again at a later date? We define that level as “durable” only if it was not observed again in the future. By contrast, a market gain that is subsequently wiped out over the completion of the market cycle is clearly transient in hindsight. Can investors identify the difference before the fact? The chart below shows the S&P 500 Index (blue line) along with the “durable” portion of market gains in data since 1940 (red line). In cycles prior to the half-cycle advance since 2009, the level of the S&P 500 is identified as durable if the market never traded lower at any point in the future. The green line shows the estimated historical valuation norm of the S&P 500 on the basis of MarketCap/GVA (nonfinancial market capitalization / corporate gross value added). The values from 1940 to 1947 are imputed based on the average relationship between GVA and nominal GDP. For a reminder of how strongly this measure is related to actual subsequent market returns, see When You Look Back On This Moment In History. Notice that the red line of durable S&P 500 market levels is almost invariably below the green line representing historical valuation norms. This demonstrates one of the central lessons of value-conscious investing: durable market gains are associated with market advances toward historically normal valuations, while transient market gains are associated with market advances that move beyond historically normal valuations. Because of that historical regularity, the “durable” threshold after 2009 is shown at the present valuation norm, and is unlikely to exceed that level, which is roughly half of the current level of the S&P 500.

[Geek's Note - For any given valuation metric X with historical norm Xn, the corresponding valuation norm for the S&P 500 at any point in time is simply the current S&P 500 level * Xn/X] I should mention that if the S&P 500 was to decline below its 2009 trough, the long red line extending from 1996 to 2009 would have to be redrawn. Such a loss would imply significant undervaluation, while a retreat to current valuation norms (somewhere in the 940-1030 range on the S&P 500, based on the most historically reliable metrics) would represent an ordinary, run-of-the-mill outcome for the completion of the current market cycle given present valuations. We certainly don’t rely on a 50% market loss, but we should absolutely allow for it. In this context, it should not be terribly surprising that the 2000-2002 market decline wiped out the entire total return of the S&P 500 – in excess of Treasury bill returns – all the way back to May 1996, or that the 2007-2009 decline wiped out the entire total return of the S&P 500 – in excess of Treasury bill returns – all the way back to June 1995. Those losses were already baked in the cake. Of course, a decline below historically normal valuation can restrain market returns for a much longer period. The fact that the 1982 low for the S&P 500 was within 10% of the 1966 high was the result of a move from secular overvaluation to secular undervaluation over that 18-year period, even though the level of overvaluation in 1966 was nowhere near present levels. Investors don’t seem to appreciate what they’ve actually done as a result of the yield-seeking speculation encouraged by the Federal Reserve in recent years. As detailed more fully in prior comments (see, for example, All Their Eggs in Janet’s Basket) investors have priced equities for zero returns over the coming decade, with the likelihood that by the end of the present market cycle, every bit of total return, every zig and zag of the market since 2000, will be wiped away for naught. Why? Because even the 4.1% annual total return in the S&P 500 since the 2000 market peak has been achieved only by driving market valuation to what is now the second-highest extreme in history, eclipsing every historical record except that 2000 peak, and beyond those of 1929, 1937, 1966, 1973, and 2007. How much of a market loss is needed to wipe away 15 years of 4.1% annual total returns? About 45%; less than the market lost in either of the 2000-2002 or 2007-2009 plunges, and not even enough to bring current market levels to historically reliable valuation norms (certainly not below those norms, as most prior market cycles have done). The expectation of such a loss is not some worst-case scenario. In the context of more than a century of market history, it is the run-of-the-mill expectation for the completion of the current market cycle. When speculation is reasonable Emphatically, I am not suggesting that one should seek to be invested in stocks only when the potential return of the market itself is expected to be durable. Rather, one should recognize the environment that is operating at any given moment. When expected market returns are likely to be durable, the ability to exit is not particularly important provided a sufficiently long investment horizon. When expected returns are likely to be transitory, one should realize that one is speculating, and the ability to exit can be valuable or even critical. If there is one lesson to draw both from our successes prior to the recent half-cycle, and from the awkward transition from our pre-2009 methods to our present methods of classifying market return/risk profiles (see A Better Lesson Than “This Time is Different” for a full narrative), it is this. The near-term outcome of speculative, overvalued markets is conditional on investor preferences toward risk-seeking or risk-aversion, and those preferences can be largely inferred from observable market internals and credit spreads. The difference between an overvalued market that becomes more overvalued, and an overvalued market that crashes, has little to do with the level of valuation and everything to do with investor risk preferences. Yet long-term investment outcomes remain chiefly defined by those valuations. In effect, durable long-term market returns obey valuations, while transitory market returns obey the risk preferences of investors (which we infer from observable market internals and other risk-sensitive measures like credit spreads). It may be reasonable to speculate in an overvalued market, provided one is highly attentive to market internals and other factors. But when investors don’t recognize which environment they are operating in, they miss opportunities to exit hypervalued markets even after market internals have deteriorated and investors have shifted toward risk-aversion, as we warned they had done in October 2000, and July 2007, and as they have today. Examine the data above, and in the accompanying links, and choose the narrative you believe. One is fiction – that stocks will rise endlessly on a glorious path forged by unicorns from the sparkling dust of Janet Yellen’s golden slippers, and that I’m an evil permabear sitting in a stone and glass fortress built into the side of a volcano, stroking a hairless cat. The other is nonfiction – that the current advance is the third financial bubble in 15 years, that the most historically reliable valuation measures are now at the second most extreme point in a century of history, that my valuation concerns in the prior two bubbles – as well as my optimism at the troughs – were all wildly vindicated by the completion of those cycles, and that despite my stumble in the recent cycle that inadvertently resulted from my insistence on stress-testing our methods against Depression-era data, a century of market history suggests that every bit of the stock market’s total return since 2000 has been transient, and stands to be wiped out. The only thing that has truly been “different” about the half-cycle since 2009 is that QE disrupted the prior historical tendency for overvalued, overbought, overbullish conditions to devolve more immediately into market losses. Yet even since 2009, as in market cycles throughout history, the market has experienced significant average losses in conditions that have joined extreme valuations with deterioration in market internals (see The Ingredients of a Market Crash). That is the situation we currently observe. Despite extreme valuations, our concerns would become much less pointed if market internals and credit spreads were to become favorable on our measures. The Roseanne Roseannadanna market Much of the investment world seems to view present conditions as a “Goldilocks market” where economic growth is positive enough to avoid recession, but not fast enough to provoke the Federal Reserve to hike interest rates. Even if these views on economic growth and Federal Reserve policy are correct, it hardly follows that stock prices will advance. S&P 500 returns are only weakly correlated with year-over-year GDP growth and have near-zero correlation with year-over-year changes in earnings. Likewise, the stance of the Federal Reserve has much less power to distinguish investment outcomes than investors seem to believe, which they might realize even by remembering that the Fed was easing aggressively and persistently throughout the 2000-2002 and 2007-2009 market collapses. In contrast, we find profound differences in market outcomes across history depending on the combined status of valuations, market internals, and broader measures of market action (which include, for example, overvalued, overbought, overbullish syndromes). Some of these combinations, from most to least favorable, are: 1) Favorable valuations that are newly joined by a shift to favorable market internals; The problem with obscene valuations and unfavorable market internals, coming off of an extended period of overvalued, overbought, overbullish conditions is that this environment couples low risk premiums with upward pressure on those risk premiums, which is the formula for a market collapse. If one reviews prior historical instances where market conditions were similar, the main question was generally not whether significant losses would unfold. The main question also wasn’t when significant losses would unfold: once market internals had deteriorated, the most reliable answer was “maybe immediately, probably shortly, and maybe after some churning.” Whether the plunge began rather immediately – as in 1929 and 1987 – or after several months of sideways distribution – as in 2000 and 2007 and perhaps today – it was nearly impossible to narrow the time frame, at least on any measure we’ve tested across history. Moreover, instances where severe losses did not emerge were typically instances where market internals improved enough to shift the return/risk profile to a different and more favorable classification. Accordingly, we remain highly defensive here, but the immediacy of our concerns would be reduced if market internals and credit spreads were to improve. So the question is typically not “whether,” and the question of “when” is unpredictable in the short run and forgotten in the sheer scope of what happens over the completion of the cycle. There is always a question of what investors will focus on as the catalyst for market losses, yet even the “what” is largely irrelevant, and is typically identified after the fact anyway. After the 1987 crash, investors blamed an unfavorable trade balance report as the reason behind the crash. The trade balance really had nothing to do with it, except for being the most unfavorable economic report that could be found in the vicinity of the crash. Significant news items tend to concentrate selling decisions that contribute to abrupt losses, but those losses are already inevitable once valuations become extreme. In the current cycle, the catalyst might be European bank leverage (which is the main reason Greece is a concern), credit concerns related to covenant lite junk debt, economic weakness, investor concern about monetary shifts, or possibly by wholly unanticipated events. But the “catalyst” will merely affect the timing of the losses. This is not a Goldilocks market. No, this is a Roseanne Roseannadanna market (Gilda Radner’s character from Saturday Night Live). Though investors seem to believe that catalysts for a market plunge should be known ahead of time, they’re likely to learn in hindsight that the specific catalyst didn’t matter. History teaches that once obscene valuation is coupled with overvalued, overbought, overbullish extremes, and is then joined by deterioration in market internals, the outcome is already baked in the cake. Afterward, investors discover “Well Jane, it just goes to show you... It’s always something. If it’s not one thing, it’s another.” Understand that now. Once extreme valuations have been established, further market gains have always been transient. Once market internals deteriorate, it’s a signal that investors have shifted from risk-seeking to risk-aversion. At that point, there is no specific event that must be known in advance. One need only have an appreciation for the inevitable swing of the pendulum from extreme euphoria to extreme fear that has characterized the financial markets for centuries. The “catalyst” is rarely appreciated as a catalyst until after severe market losses have already occurred, and in many cases, that catalyst is simply an event that concentrated selling plans that were already being contemplated. If it’s not one thing, it’s another. But it’s always something. The message here is not “sell everything.” The message is to understand where we are in the market cycle from the standpoint of a century of reliable evidence, and to act in a way that meets your investment objectives. Align your portfolio with careful consideration for your tolerance for losses over the market cycle; with your willingness to miss out on interim market gains should they emerge; with the horizon over which you will actually need to spend from your investments; with the extent that you believe that history is actually informative for making investment decisions; with the extent to which alternative investment outlooks are supported by evidence, ideally spanning numerous market cycles. Henny Youngman used to tell a story about a guy who hears a little voice in his head singing “Go to Las Vegas.” So the guy immediately turns his car around and heads for Las Vegas. The voice sings “Go to the roulette table.” The guy goes to the roulette table. The voice sings “Put $10,000 down on red.” The guy puts $10,000 down on red. He loses. The voice says, “Hey, how ‘bout that?” I shared that story with readers in mid-2007 as the market approached its peak before the global financial crisis, noting: “Investors are hearing a thousand little voices here telling them to ‘ride the bull,’ that stocks have a ‘floor’ under them, and that valuations are cheap. Whatever risks investors choose to take, they would do well to recognize that if those risks go terribly wrong, most of those little voices will be passive observers with nothing to say but ‘Hey, how ‘bout that.’” “There are clearly points where the market has speculative merit on the basis of broad market action and favorable internals, even if valuations don't provide much investment merit. But there are also points where investment merit is clearly absent and speculative trends become strikingly overextended. Then the only reason for speculating is that investors are speculating. On average, those periods turn out badly.” The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |