|

|

||||||

|

|

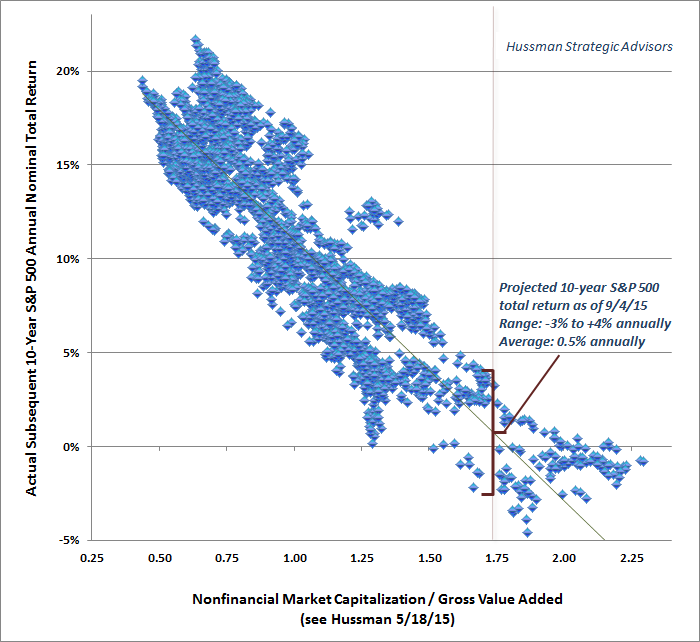

September 7, 2015 That Was Not a Crash Following the market decline of recent weeks, the most reliable valuation measures we identify now project average annual nominal returns for the S&P 500 of about 0.5% in the next 10 years. On a broad range of historically reliable valuation measures (see Ockham’s Razor and the Market Cycle) the May peak in the S&P 500 reached valuations averaging about 114% above run-of-the-mill historical norms – more than double the valuation levels that have historically been associated with the 10% average expected market returns that investors have enjoyed over the long-term. At present, those measures have retreated to about 92% above historical norms. Keep in mind that low interest rates don’t raise the estimated 10-year expected return on stocks from the current 0.5% level. Low interest rates only make the low expected return on stocks somewhat more “acceptable” because the alternatives are similarly dismal. The Federal Reserve’s policies of zero interest rates and quantitative easing have done nothing but to encourage yield-seeking speculation, bringing valuations to extreme levels, and leaving prospective future investment returns equally depressed. Those who assert that high equity valuations are “justified” by low interest rates are actually (and probably unknowingly) saying that 0.5% expected returns on equities over the coming decade are a-okay with them. But it’s critically important to understand that while low interest may help to explain why current market valuations have been driven to obscene levels, low rates do not change the relationship – the correspondence – between elevated valuation levels and dismal subsequent long-term market returns. The chart below shows the relationship between the most reliable valuation measure we identify (MarketCap/GVA) versus actual subsequent S&P 500 total returns over the following decade. The current level of valuations is associated with a likely range of 10-year returns between about -3% and +4%, with an average expectation of 0.5% annually.

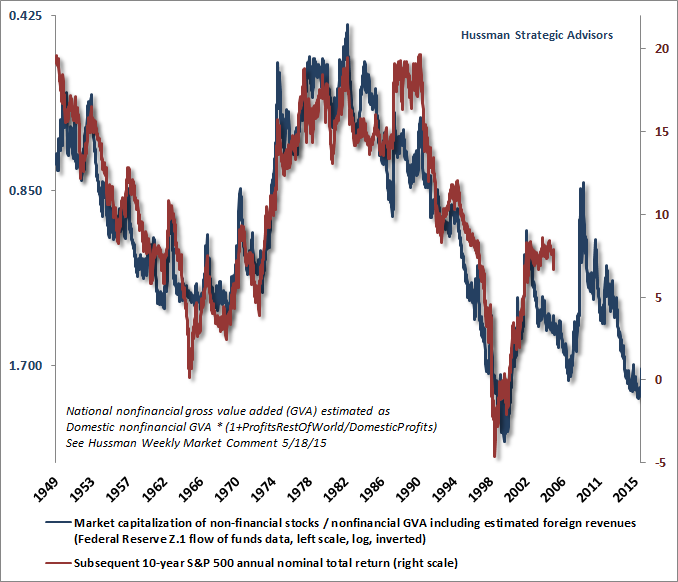

The following chart shows the same data from a time-series perspective. Try the identical analysis with other popular valuation indicators and you’ll see why we rely on MarketCap/GVA and similar variants such as price/revenue, market cap/GDP and our margin-adjusted version of the Shiller P/E. We see all kinds of valuation metrics trotted out by analysts as if they’re meaningful. It’s only when investors examine the historical data (or live through the consequences of failing to do so) that they realize how little relationship many popular valuation metrics have with actual subsequent market returns. For our part, we insist on evidence. It makes us much less fun to hang around with at parties if the conversation turns toward the markets.

Market conditions will change. Look at every market cycle in history, and you’ll see that prospective market returns have always approached 9-10% or more in every market cycle – even when interest rates were similar to current levels (prior to the mid-1960’s). The best opportunity to boost investment exposure is at points in the market cycle where a material retreat in valuations is joined by broad improvement in market internals. That was not a crash The market decline of recent weeks was not a crash. It was merely an air-pocket. It was probably just a start. Such air pockets are typical when overvalued, overbought, overbullish conditions are joined by deterioration in market internals, as we’ve observed in recent months. They are the downside of the “unpleasant skew” that typically results from that combination – a series of small but persistent marginal new highs, followed by an abrupt vertical decline that erases weeks or months of gains within a handful of sessions (see Air Pockets, Free-Falls, and Crashes). Actual market crashes involve a much larger and concerted shift toward investor risk-aversion, which doesn’t really happen right off of a market peak. Historically, market crashes don’t even start until the market has first retreated by 10-14%, and then recovers about half of that loss, offering investors hope that things have stabilized (look for example at the 1929 and 1987 instances). The extensive vertical losses that characterize a crash follow only after the market breaks that apparent “support,” leading to a relentless free-fall that inflicts several times the loss that we’ve seen in recent weeks. Our strategy is to align our investment stance with the market return/risk profile we identify based on observable conditions. There’s no need to make projections about a crash, but it’s fair to say that we can’t rule it out given that every major crash in history has emerged from the 8% of historical market conditions matching what we currently observe (see Risk Turns Risky for a review of cumulative market losses in this subset of history). We can only say that on average, stocks have continued to lose considerable ground under the return/risk classification we identify here, so we remain defensive. The reason why the word “crash” has been bandied about to describe the recent selloff, I think, is partly because investors have lost all perspective of the losses that have historically been associated with that word, but mostly because it gives market cheerleaders the needed "cover" to encourage investors to continue speculating near record market valuations. After all, everyone “knows” that investors shouldn’t sell after a crash, thus the endless flurry of articles advising “selling in a crash is a textbook mistake,” “selling off stocks during a crash is a terrible idea”, “whatever you do, don’t sell”, “market crash: don’t rush to press the panic button,” “the worst investing move during a market crash,” ... you get the idea. Hand-in-hand with the exaggeration of the recent decline as a “crash” and “panic” is the exaggeration of investor sentiment as being wildly bearish. The actual shift has been from outright bulls to the “correction” camp, but that’s a rather meaningless shift since anyone but the most ardent bull would characterize current conditions as being at least a market correction. Historically, durable intermediate and cyclical lows are characterized by a significant increase in the number of outright bears. That’s not yet apparent here. Indeed, Investors Intelligence still reports the percentage of bearish investment advisors at just 26.8%. It’s generally true that one doesn’t want to sell stocks into a crash (as I've often observed, once an extremely overvalued market begins to deteriorate internally, the best time to panic is before everyone else does). Still, the recent decline doesn’t nearly qualify as a crash. For the record, those familiar with market history also know that even “don’t sell stocks into a crash ” isn’t universally true. Recall, as an extreme example, that from September 3 to November 13, 1929, the Dow Industrials plunged by -47.9%. The market briefly recovered about half of that loss by early 1930. Even so, it turned out that investors would ultimately wish they had sold at the low of the 1929 crash. By July 8, 1932, the Dow had dropped an additional -79.3% from the November 1929 trough. In any event, the recent market retreat, at its lowest closing point, took the S&P 500 only -12.2% from its high, and at present, the index is down just -9.7% from its highest closing level in history. To call the recent market retreat a “crash” is an offense to informed discussion of the financial markets. To understand the market cycle is to understand this: Valuations are the primary driver of long-term investment returns, but returns over shorter portions of the market cycle are driven by the attitude of investors toward risk, and the most reliable measure of this is the uniformity and divergence of market internals across a broad range of individual securities, industries, sectors, and security types, including debt of varying creditworthiness. When investors are risk-seeking, even extreme valuation may have no immediate consequence. When investors shift to risk-aversion, previously irrelevant overvaluation can suddenly matter with a vengeance. Given the market return/risk profile we currently identify, we doubt that what the Fed does in September will make much difference in the ultimate outcome of this market cycle. As for shorter-run outcomes, the effect of Fed policy on the financial markets is determined by the risk-seeking or risk-aversion of investors, so the thing to watch is the behavior of market internals. Despite hypervalued and overbullish market conditions, quantitative easing encouraged much more sustained risk-seeking in recent years than we’ve observed in prior market cycles across history. Overvalued, overbought, overbullish extremes that were historically followed by rather immediate market collapses were instead followed in recent years by continued speculation. One had to wait for market internals to explicitly deteriorate before taking a strongly negative market outlook (see A Better Lesson than “This Time is Different”). However, we also know from a century of history, including the 2000-2002 and 2007-2009 plunges, that monetary easing does nothing to prevent hypervalued markets from collapsing once investor preferences shift toward risk-aversion. That shift has been evident since the third quarter of 2014 through increasing dispersion and deterioration in market internals. On real wealth and paper losses Keep in mind that when paper wealth is “lost,” nobody gets it. Quantitative easing has not made the nation “wealthier”, nor will the massive paper loss we expect over the completion of the market cycle make the nation “poorer.” As I detailed in June (see When Paper Wealth Vanishes): “As in equal or lesser speculative bubbles across history, there’s a common delusion that elevated stock prices represent wealth to their holders. That is a fallacy, and we can hardly believe that given the collapses that followed the 2000 and 2007 extremes, investors (and even Fed policymakers) would again fall for that fallacy so readily. The actual wealth is in the cash flows that are ultimately delivered into the hands of shareholders over time. Individuals can realize their paper wealth by selling now to some other investor and receiving cash in return, but only a small proportion of investors can actually convert current paper wealth into cash by selling to other investors without disrupting the bubble. The new buyer then receives whatever cash flows the stock delivers into the hands of existing holders, and can eventually sell the claim to the remaining stream of future cash flows to yet another investor. Ultimately, a share of stock is nothing but a claim on the long-term stream of cash flows that will be delivered into the hands of its holders over time. The current price and the future cash flows are linked together by a rate of return: the higher the price you pay today for a given stream of future cash flows, the lower the rate of return you can expect achieve by holding that investment over the long-term.” Emphatically, the wealth of a nation is not measured by the price that the most reckless speculator will pay for the last few shares that change hands at the most exuberant moment of a bull market, multiplied by the entire number of shares outstanding. No, the wealth of a nation is its accumulated stock of productive real investment, human capital, and resources. Everything else cancels out because every security owned by some holder is also the liability of some issuer (see Stock Flow Accounting and the Coming $10 Trillion Paper Loss). Securities are ownership claims on a long-term stream of future cash flows. Paper gains don’t create aggregate wealth, and paper losses don’t destroy it. Think of it this way. Suppose a security promises you a $100 payment 10 years from now. If you pay $32 for that security, you’ll get a 12% annual return on your money. If you pay $122 for that security, you’ll get a -2% annual loss on your money. Does the economy have more “wealth” in the second case? No. The security represents $100 in 10 years, regardless. Now, you may be able to sell the security to someone else for $122, and let them hold the bag over the next 10 years. In that case, you may end up with more wealth, but your gain will come at someone else’s loss. In short, aggregate wealth does not increase just because securities become overpriced. Aggregate wealth is not destroyed just because valuations normalize. Put simply, many investors, and even some policy makers at the Federal Reserve, are under the delusion that paper market capitalization represents real wealth to the economy as a whole. The truth is that the wealth is in the productive assets of the economy and the long-term stream of cash flows they generate. Price fluctuations can certainly affect the distribution of wealth. Those who repeatedly buy stocks from others at depressed prices, and sell them to others at elevated prices, will accumulate the purchasing power of others. Those who repeatedly do the opposite will surrender their purchasing power to others. But the aggregate wealth of the economy as a whole is unaffected by those price fluctuations. Active or passive, review your portfolio here There’s no way for the economy to somehow “lock in” the paper gains that yield-seeking speculation has produced in recent years. Every share of stock that has been issued has to be held by someone at every point in time until it is retired. For every seller, there has to be a buyer who will hold stocks over the completion of this market cycle. For that reason, there’s no sense at all in encouraging investors, in aggregate, to exit stocks – it’s impossible to do so. For our part, we’re not encouraging investors to sell (or to buy) but rather to act quickly to make sure that their own portfolios are actually aligned with their personal risk tolerance and the horizon over which they expect to spend their funds. Yes, from our perspective, even the 2.13% yield on 10-year Treasury bonds will probably exceed the 10-year total return of the S&P 500 over the coming decade, and with far smaller interim losses. From our perspective, it’s appropriate to consider valuations and market action, which hold us to a hard-defensive stance here, but which we also expect to encourage a fully-invested or leveraged market outlook after a material retreat in valuations is joined by improved market internals. We’re full-cycle investors, and we adhere to that full-cycle discipline. Passive buy-and-hold investors follow a different discipline, and may not share our expectation about market returns, which is fine. Yet even for investors who have no particular view about future market returns, two considerations are still critical here. First, align your portfolio with your risk tolerance. Even passive investors should recognize and allow for the reasonable potential for a 40-55% market loss from the recent market high, and ensure that they would be able to maintain their investment discipline in the event a market loss of that size actually occurs (as it has in recent market cycles). We don’t see any particular reason to expect valuations to be drawn to a secular low like 1949, or 1974, or 1982, but investors should still understand that those lows correspond to valuation levels that were literally one-quarter of what we observed at the recent market peak (see the charts above). Second, align your portfolio with the horizon over which you actually expect to spend the funds. Recognize that from a duration standpoint, the S&P 500 is effectively a 44-year instrument here – though duration would drop to about 27 years if valuations return toward historical norms. While it actually takes some tedious mathematics to demonstrate it, it turns out that provided that dividend payments grow relatively smoothly over time, the duration of the S&P 500 is well approximated by the S&P 500 price/dividend ratio – regardless of the growth rate of dividends. As an example of how we think about aligning passive equity allocation with market duration, suppose that an investor has no particular view about future market returns. If that investor expects to spend down the investment portfolio an average of 20 years into the future (spending some funds sooner, and some funds later), that investor might target about 20/44 = 45% of portfolio value in equities. One might object that changing the allocation as valuations change is market timing and not passive investing. We strongly disagree. Aligning the duration of one’s investment portfolio to be consistent with the expected spending horizon is one of the most basic principles of sound financial planning. I’ve regularly discussed these principles for passive investors over the years. I certainly don’t discourage investors from adhering to a passive investment discipline if it fits well with their investment views and financial goals, but I do think that many passive investors overestimate their ability to maintain discipline in a downturn, and fail to align their portfolio with their investment horizon, particularly as market duration changes over the cycle. Even for passive investors, the appropriate allocation to stocks is inverse to their duration, because it’s essential to consider the horizon over which the funds will be spent. As a reminder of how this all works, see my January 5, 2009 market comment – Portfolio Rebalancing: Don’t Ignore Duration, when I noted that the appropriate investment exposure for passive investors had increased substantially compared with 2007, as a result of significantly improved valuations and a corresponding shortening of market duration. The bottom line is this. Think carefully about your own tolerance for risk, with a clear understanding that a 40-55% market loss from the recent high would be a historically run-of-the-mill reversion to quite ordinary valuation norms. Also think carefully about your investment horizon. If you need to spend the funds within a short number of years, you really shouldn’t have more than a modest fraction of those assets in equities here, unless you want the ability to follow through on your spending plans to be highly sensitive to market outcomes.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |