|

|

||||||

|

|

September 21, 2015 When an Easy Fed Doesn't Help Stocks (and When It Does) Last week, the Federal Reserve chose to do nothing to move short-term interest rates away from zero after nearly 6 years of extraordinary policy distortion. As detailed below, the inaction of the Fed, and the failure of the stock market to advance in response, follows the script that I detailed in February. Policy makers at the Fed actually appear to believe – contrary to historical evidence and contrary even to the recent experience of numerous countries around the world – that activist monetary policy has meaningful and reliable effects on subsequent economic activity. It’s lamentable that otherwise thoughtful policy makers, much less journalists who cover these actions, show no interest in how weak these correlations are in actual data, and seem incapable of operating even the most basic scatterplot. Despite the spew of projectile money creation around the world, the global economy is again deteriorating. The main defense of the Fed’s inaction seems to be that years of zero interest rate policy have been hopelessly ineffective, so continued zero interest rate policy is necessary. As we’ve demonstrated previously, there’s no statistical evidence in the historical record to suggest that activist monetary policy has any relationship to actual subsequent economic activity (see The Beauty of Truth and the Beast of Dogma). Historically, monetary policy variables themselves can be largely predicted by previous changes in output, employment and inflation. That “systematic” component of monetary policy does have a weak correlation with subsequent economic changes. It’s unclear whether that’s purely incidental, or whether those systematic changes in monetary variables (such as short-term interest rates) are actually necessary for the weak effects that follow. I should be careful to note that monetary policy also seems to weakly influence confidence expressed in certain survey-based questionnaires. But that correlation emphatically does not translate into changes in actual output, income, or employment. Put simply, massive activist deviations from systematic monetary policy rules provide no observable economic benefit, but instead create fertile ground for speculative bubbles and crashes. Despite its wild grandiosity, Fed intervention was not what ended the global financial crisis. Recall that the global financial crisis ended – and in hindsight ended precisely – on March 16, 2009, when the Financial Accounting Standards Board abandoned FAS 157 “mark-to-market” accounting, in response to Congressional pressure from the House Committee on Financial Services on March 12, 2009. That change immediately removed the threat of widespread insolvency by making insolvency opaque. This might not have meant much if regulators had continued to insist on mark-to-market when evaluating bank solvency. But with regulators willing to go along, the global financial crisis ended with the stroke of a pen. Those who hail the March 2009 replacement of mark-to-market with mark-to-unicorn as a “necessary” response miss the point (though Iceland has actually done quite well relative to the rest of the world, despite initial disruption, by insisting on massive bank restructuring rather than playing extend-and-pretend). The point is that Fed intervention did not end the crisis, nor would a global financial crisis have occurred in the first place without combination of an activist Fed and a misregulated financial sector. Absent the restoration of Glass-Steagall and greater rules-based constraints on the Federal Reserve, none of the policy responses since 2009 (including Dodd-Frank) effectively reduce the risk of similar speculative bubbles and crises in the future. Fed easing certainly increased the stock of bank reserves and enabled banks to satisfy withdrawal demands during the crisis – the legitimate function of a central bank. Ben Benanke's violation of Section 13(3) of the Federal Reserve Act (which has since been rewritten by Congress to spell the law out like a children's book) also helped some financial insitututions illegally dump bad securities onto the public balance sheet. Despite these actions, Fed intervention did not produce the economic recovery. The entire recovery we’ve observed in the economy since 2009 has actually represented standard, systematic mean reversion. Indeed, as I demonstrated in March (see Extremes in Every Pendulum), the progress of the economy since 2009 has been somewhat below what would have been predicted from past values of non-monetary variables alone. Adding monetary variables does not meaningfully improve the power to explain either recent or historical economic fluctuations. Instead, the main impact of suppressed interest rates is to encourage yield-seeking speculation, to give low quality creditors access to the capital markets, to misallocate scarce saving, to subsidize leveraged carry trades, to reduce the long-term accumulation of productive capital, and to foment serial bubbles and crashes. Understand this in no uncertain terms: the only economic activities that are encouraged by zero interest rates are activities so marginal and unproductive that they can’t survive even a slightly higher hurdle rate, or where the primary cost of the activity is interest itself, such as leveraged speculative “carry” trades by hedge funds and financial institutions. What created the housing bubble and global financial crisis? The Fed’s policy of suppressing interest rates. That’s what drove investors to seek higher yields in mortgage debt (which had until then never experienced a widespread default crisis). Wall Street responded to the demand by creating more “product,” but the only way to do that was to lend to increasingly marginal borrowers – hence subprime and no-doc lending to anyone capable of drawing a breath. Institutions, largely under the protection of government insurance, then went about the slicing, dicing and repackaging of “financial engineering” to turn garbage into flowers. Other hedge funds and institutions further enlarged the bubble through speculative carry trades: borrowing heavily at cheap rates to finance massive leveraged purchases of collateralized mortgage securities. As that yield-seeking bubble was emerging, I observed, “why is anybody willing to hold this low interest rate paper if the borrowers issuing it are so vulnerable to default risk? That's the secret. Much of the worst credit risk in the U.S. financial system is actually swapped into instruments that end up being partially backed by the U.S. government. These are held by investors precisely because they piggyback on the good faith and credit of Uncle Sam.” The repeal of Glass Steagall (which would have prohibited banks to mingle insured banking with reckless speculation), and weak regulatory oversight certainly contributed to creating the global financial crisis. But the Federal Reserve’s suppression of interest rates was at the root of all of it. We are doing – we have already done – all of this again, only with different instruments. The low-doc loans of the housing bubble have been replaced by the covenant-lite debt of the recent bubble. Housing has been replaced by debt-financed equity repurchases and leveraged buyouts, taking the median stock to more extreme valuations than at the 2000 peak, and putting the capitalization-weighted S&P 500 within 15% of its peak 2000 valuation on measures (e.g. market capitalization to GDP or corporate gross value added) most strongly correlated with actual, subsequent total returns on stocks. From current valuations, investors should expect zero total return on the S&P 500 over the coming decade (see All Their Eggs in Janet’s Basket). Part of the reason the Fed found it so difficult last week to justify a move away from zero interest rates is that the Fed seems incapable of recognizing, much less admitting, the speculative risks it has created. The strongest reason to normalize monetary policy was to reduce those risks, but the proper time to have done that was years ago. At this point, obscene equity valuations are already baked in the cake on valuation measures that are reliably correlated with actual subsequent stock market returns. At this point, hundreds of billions of dollars of low-grade covenant-lite debt have already been issued at risk premiums that are next to nothing. The bursting of this bubble is no longer avoidable. If history is any guide, policy makers will manage the resulting disruption by the seat of their pants, since they seem incapable of learning from history itself. With the Fed showing no willingness to recognize the speculative risks of what it has done, it was left trying to justify a policy normalization based on an economy that remains uninspiring. Justifying a rate increase on a purely economic basis was impossible, but the logic of leaving rates unchanged was equally tortured – that zero interest rates have had so little impact on the real economy that a continuation of zero interest rates is actually justified. In the end, the Fed was forced to play the same “we expect the economy to strengthen soon” game it has been playing for years. Unfortunately, with new orders and order backlogs uniformly weak across numerous regional Fed and purchasing manager’s surveys, and with unsold inventories accumulating, the prospects for fresh economic weakness remain much stronger than the prospects for surprising near-term strength. In the end, we expect the following outcome to unfold over the coming quarters: a) the headline economic numbers will likely weaken rather than strengthen; b) the Fed will likely discover that the opportunity to normalize interest rates has passed; c) unless investors shift back to risk-seeking preferences, as evidenced by uniformity of market action across a wide range of internals, even fresh Federal Reserve easing can be expected to be accompanied by a steep market retreat. When an easy Fed doesn’t help stocks (and when it does) Investors who wonder why the stock market failed to advance on the Fed’s decision to leave interest rates unchanged would do well to understand that the market is following a script that has played out repeatedly across a century of market history. The short explanation is straightforward. When investors are risk-seeking (which we infer from the behavior of market internals), Fed easing tends to be very favorable for the stock market, because risk-free, low-interest liquidity is a hot potato to risk-seeking speculators. However, once investors become risk-averse, Fed easing has no favorable effect at all, on average, because low-interest liquidity is desirable to risk-averse investors. In short, the market response to Fed easing is conditional on the prevailing risk preferences of investors. The following is from my February 9 market comment earlier this year (see Expect a Decade of 1.7% Portfolio Returns from a Conventional Asset Mix).

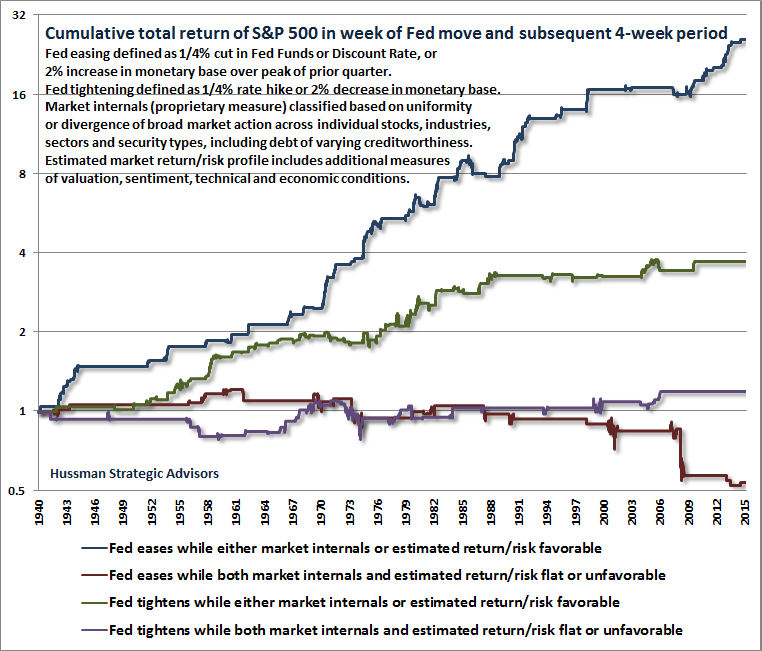

The chart below shows, in data since 1940, the relationship between Fed policy changes and subsequent market returns in the week of the policy change and the following 4 weeks. It’s the existing background condition of the market that actually determines the response. For purposes of illustration, we define a Fed easing as a cut of at least 0.25% in the Federal Funds rate or the Discount Rate, or an increase of 2% in the monetary base above the high of the prior quarter. Conversely, we define a Fed tightening as a hike of at least 0.25% in the Federal Funds rate or the Discount Rate, or a decrease of 2% in the monetary base below the low of the prior quarter. While our specific measures of market internals and estimated market return/risk profiles are proprietary, we’ve provided general details hundreds of times over the years. The essential feature of what we call “market internals” is uniformity of price action across numerous individual stocks, industries, sectors, and security types, including bonds of varying creditworthiness. The estimated market return/risk profile considers additional measures of valuation, sentiment, technical and economic conditions. What should be most evident in the chart below is that Fed easing benefits the market, on average, only when market conditions are already favorable from the standpoint of investor risk-preferences or the market return/risk profile. In contrast, Fed easing provides no benefit at all (and in fact is associated with steep market losses, on average), when neither of those background conditions is favorable. In response to Fed tightening, the market actually tends to advance over the following month, on average, provided that investors are already risk-seeking or the market return/risk profile is favorable. When investors are in a risk-off mood, Fed tightening has very little effect, but it’s actually preferable to Fed easing, mainly because Fed easing during risk-off conditions is typically a response to continuing economic deterioration.

As a technical note, the lines above overlap in a number of instances when a tightening and easing both took place within a 5-week interval, as occurred several times during the 1973-1974 bear market, for example. Also, while it’s not widely remembered, the last Fed tightening move was actually in February 2010, when the Fed raised the Discount Rate from 0.25% to 0.75% to discourage direct borrowing through the discount window. If you examine the 2000-2002 period, you’ll notice that the market responded to Fed easing by losing value, on average, as it did again during the 2007-2009 collapse. However, in the 2000-2002 collapse, most of the overall market damage was in periods that fell outside the 4-week period after a Fed move. In contrast, some of the most severe market losses during the 2007-2009 global financial crisis occurred immediately on the heels of Federal Reserve easing moves. Indeed, the S&P 500 lost over 40% of its value in a 12-week period between September-November 2008 as the Fed continued to frantically cut rates – an easing cycle that began several weeks before the 2007 market peak. Many investors seem to be hoping for QE4. They should be careful what they wish for, because in an environment of investor risk-aversion, the initiation of QE4 would very likely be associated with an outcome much like 2008 – it would likely be a response to unexpected economic deterioration. Unlike most of the period since 2009, investors no longer appear to have the risk-seeking preferences that supported speculation during previous bouts of QE. Since the third quarter of 2014, market internals have been decidedly unfavorable on our measures, as has the expected market return/risk profile that we classify on the basis of observable data. These shifts indicate that investors have subtly shifted from risk-seeking preferences to risk-averse preferences. In the chart above, this is a shift from the blue line at the top of the chart to the red line at the bottom. What will improve the outlook? It’s essential to understand how the recent half-cycle since 2009 has differed from history. In prior market cycles across a century of data, the emergence of an extremely overvalued, overbought, overbullish syndrome of market conditions was regularly accompanied or closely followed by deterioration in market internals, and in that environment (as we saw in both 2000-2002 and 2007-2009), Fed easing was ineffective in supporting the market. What quantitative easing really did in recent years was to reduce that overlap, by aggressively and intentionally encouraging yield-seeking speculation even after extremely overvalued, overbought, overbullish conditions had developed. In the face of QE, one had to wait until market internals deteriorated explicitly before taking a strongly negative market outlook. But while QE extended the risk-seeking of investors, it hasn’t been effective in supporting the market – even since 2009 – when weak market internals have signaled greater risk aversion among investors. At present, that’s exactly what we see. If market internals improve materially, conveying a signal that investors have shifted back to risk-seeking preferences, our immediate downside concerns would be postponed. The essential lesson of the recent half-cycle is that PROVIDED investors are already in a risk-seeking mode, as evidenced by a strong uniformity of market internals across individual stocks, industries, sectors and security types (such as debt securities of varying credit quality), quantitative easing tends to support further speculation regardless of obscene valuations. That risk-seeking environment, however, is no longer with us. Investors should remain alert that current market outcomes are likely to be repeatedly punctuated by air-pockets and panics, and given the extreme valuations we continue to observe on historically reliable measures, quite possibly a major market crash. Unfortunately, my sense is that investors are unwilling to recognize that current market conditions differ in a critical way from the conditions that persisted through most of the half-cycle advance since 2009. It’s easier to remember “Don’t fight the Fed” than “Don’t fight the Fed provided that the Fed is easing and investors have risk-seeking preferences, as evidenced by the uniformity of market internals.” The problem is that simplistic Fed-following would have encouraged investors to follow the Fed straight into some of the most violent market losses in history, including the entirety of both market collapses of 50% or more since 2000. As a side note, it’s also easier to remember “The trend is your friend” than “The trend is your friend until it becomes overextended and internals begin to deteriorate.” The second variant, however, is the one best supported by a century of historical evidence. The upshot is simple. Given unfavorable market internals, and given that we continue to classify the negative market return/risk profile as negative based on historically reliable measures, investors should not expect a favorable market response from the Federal Reserve’s decision to defer a rate hike. Every instance is different, but on average, stocks have lost value under present conditions. We continue to observe deterioration in leading economic measures, though we don’t yet observe enough weakness to anticipate a recession with confidence. From an investment standpoint, our focus continues to be on measures of investor risk preferences, and the market return/risk profile we identify based on conditions we observe at each point in time. As I’ve frequently noted, I expect that the best opportunity to establish significant market exposure will be at the point when a material retreat in valuations is joined by an early improvement in market internals. Despite the “permabear” label, the fact is that I’ve shifted to a constructive or aggressive outlook after every bear market over three decades as a professional investor, including years as a leveraged raging bull in the early-1990’s, early-2003 after the 2000-2002 collapse, and even late-2008 (though that 2008 shift was truncated by my 2009 insistence on stress-testing our methods of classifying market return/risk profiles against Depression-era data). Given my roots as a value investor, I’ve had difficulty not looking like an out-of-touch spoilsport by the peak of speculative bubbles, and then being treated as some sort of dark mastermind* by the completion of the cycle. The more evenhanded reality is simply that I test everything possible against the available evidence, address challenges as they arise, and let discipline take care of the rest. As Wayne Gretsky once said, “I skate to where the puck is going to be, not where it has been.” We've got a hypervalued market that's lost internal support. Until that shifts, recognize that the game has changed. I’ve been very open about the central challenge we faced in the advancing half-cycle since 2009, and how we addressed it - see A Better Lesson Than “This Time is Different” for the full narrative. Learn from that experience. Valuations are obscene here, and investment returns for the S&P 500 over the coming decade will be dismal as a result, most likely with deep interim losses along the way. But over shorter horizons, the response of the market to all other factors will be conditioned by the risk-preferences of investors, as conveyed by the uniformity or divergence of market internals. Even without material retreat in valuations, improved market internals would at least remove the urgency from our current concerns about potentially vertical market losses. We’ll take the evidence as it arrives, and our outlook will shift as conditions shift. *One of the most frequent stock photos accompanying news stories about my outlook pictures me in a shadowy, brooding pose. The shot was taken for a magazine by a rather famous British photographer during the financial crisis, and every time I smiled even slightly, he would yell “Wipe that smile off your face! This is global financial meltdown!” The shot still feels inauthentic, because a smile shows the capacity to find something to appreciate in everything one encounters. As my friend and teacher Thich Nhat Hanh says, “Sometimes your joy can be the source of your smile, and sometimes your smile can be the source of your joy.” I highly recommend it.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |