|

|

||||||

|

|

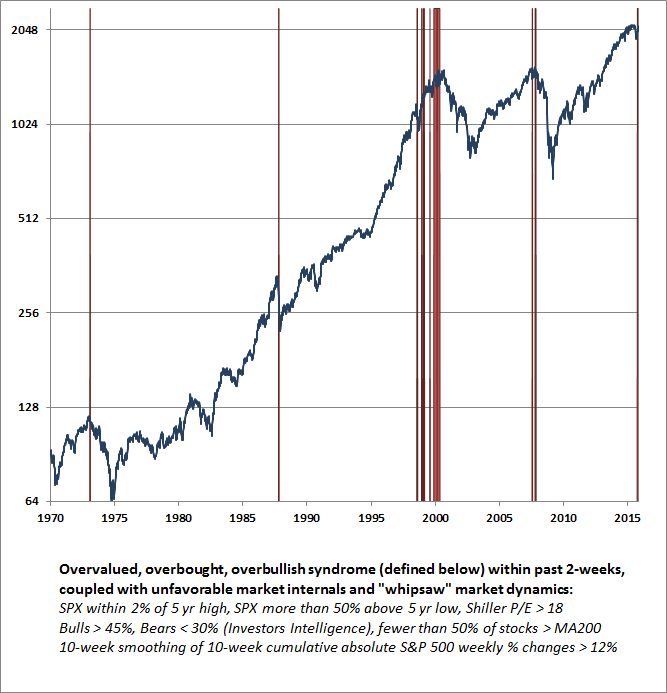

November 9, 2015 Psychological Whiplash Investors have experienced a great deal of whiplash in recent months. After a rapid but relatively contained retreat in August and September, the stock market has rebounded to within 2% of its May record high. Only weeks ago, investors were concerned about economic deterioration. As of Friday, strength in nonfarm payrolls has suddenly convinced investors that a December rate hike by the Fed is all but certain. From an economic standpoint, my impression is that this whiplash is largely psychological, and has very little to do with any underlying change in economic fundamentals. Instead, it reflects a tendency to respond to all economic data as if it is coincident (reflecting the current state of the economy) rather than carefully distinguishing leading data — primarily new orders and order backlogs, from coincident data — primarily income and production, from lagging data — employment figures, particularly payrolls and the unemployment rate, which are essentially the most lagging data series in economics. The overall signal we draw from the economic data continues to lean much more toward deterioration than to strength. Friday’s data was undoubtedly a blowout number, at 271,000 new jobs, but it’s important to recognize that payroll data is a lagging, not leading, measure of economic activity. Indeed, extremely high payroll figures often immediately preceded recessions prior to 1990, though we haven’t seen that in recent economic cycles. What’s true most generally is that economic data proceeds in a sequence that moves from financial indicators, to new orders, to production and income, and finally to employment. As I noted in February: “The combination of widening credit spreads, deteriorating market internals, plunging commodity prices, and collapsing yields on Treasury debt continues to be most consistent with an abrupt slowing in global economic activity. Generally speaking, joint market action like this provides the earliest signal of potential economic strains, followed by the new orders and production components of regional purchasing managers indices and Fed surveys, followed by real sales, followed by real production, followed by real income, followed by new claims for unemployment, and confirmed much later by payroll employment. Stronger conclusions, particularly about the U.S. economy, will require more evidence, but from a global perspective, these pressures are already quite evident.” An evaluation of this sequence may provide a somewhat more tempered view of economic conditions than Friday’s employment figure, taken by itself, might suggest. First, recognize that in the context of divergent market internals across a broad range of individual stocks, the kind of whipsaw stock market behavior we’ve seen in recent months has historically been more characteristic of market topping processes than not. One way to measure this whipsaw movement is to examine cumulative absolute weekly percentage changes in the market over the most recent 10-week period. Those familiar with nonlinear analysis will recognize this as a sort of “fractal ruler”; much like measuring the length of a coastline by adding up all of the edges, which capture the irregular shoreline better than simply drawing a straight line. When significant market whipsaws have occurred along with recent overvalued, overbought, overbullish conditions and flagging participation from the broad market, steep market losses have often followed. We observed the same thing in 1973, 1987, 2000 and 2007. Still, a clear improvement in market internals would defer our immediate concerns.

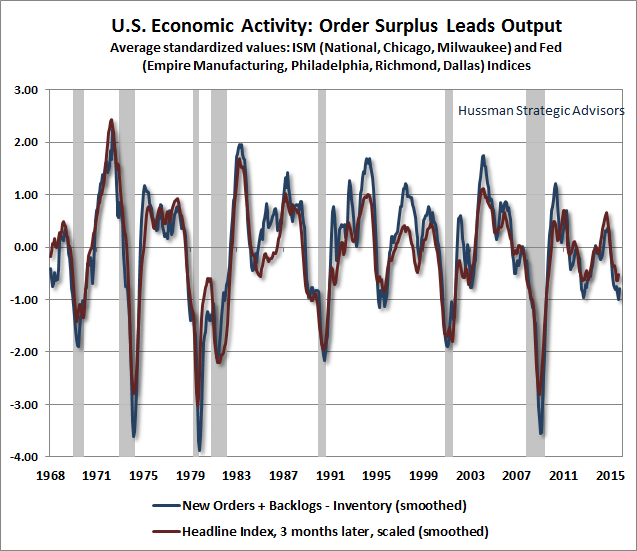

Moving to economic data, the next chart presents what I’ve called the “order surplus” indication from regional Fed and purchasing managers surveys: new orders + order backlogs - inventories. This measure tends to lead changes in headline production figures by about three months. Clearly, deterioration of the recent magnitude is not consistently associated with recession, although recessions have been frequent enough to be of some concern even here. As Bill Hester recently observed, the current level of economic activity has had a much higher probability of being recessionary in periods when the S&P 500 was also weak — for example, below its level of 6 months earlier, or below its 12-month moving average. The fact that the S&P 500 is currently within about 1% of those levels suggests some level of economic concern already, but our concerns would be substantially amplified in the event of fresh and significant equity market weakness.

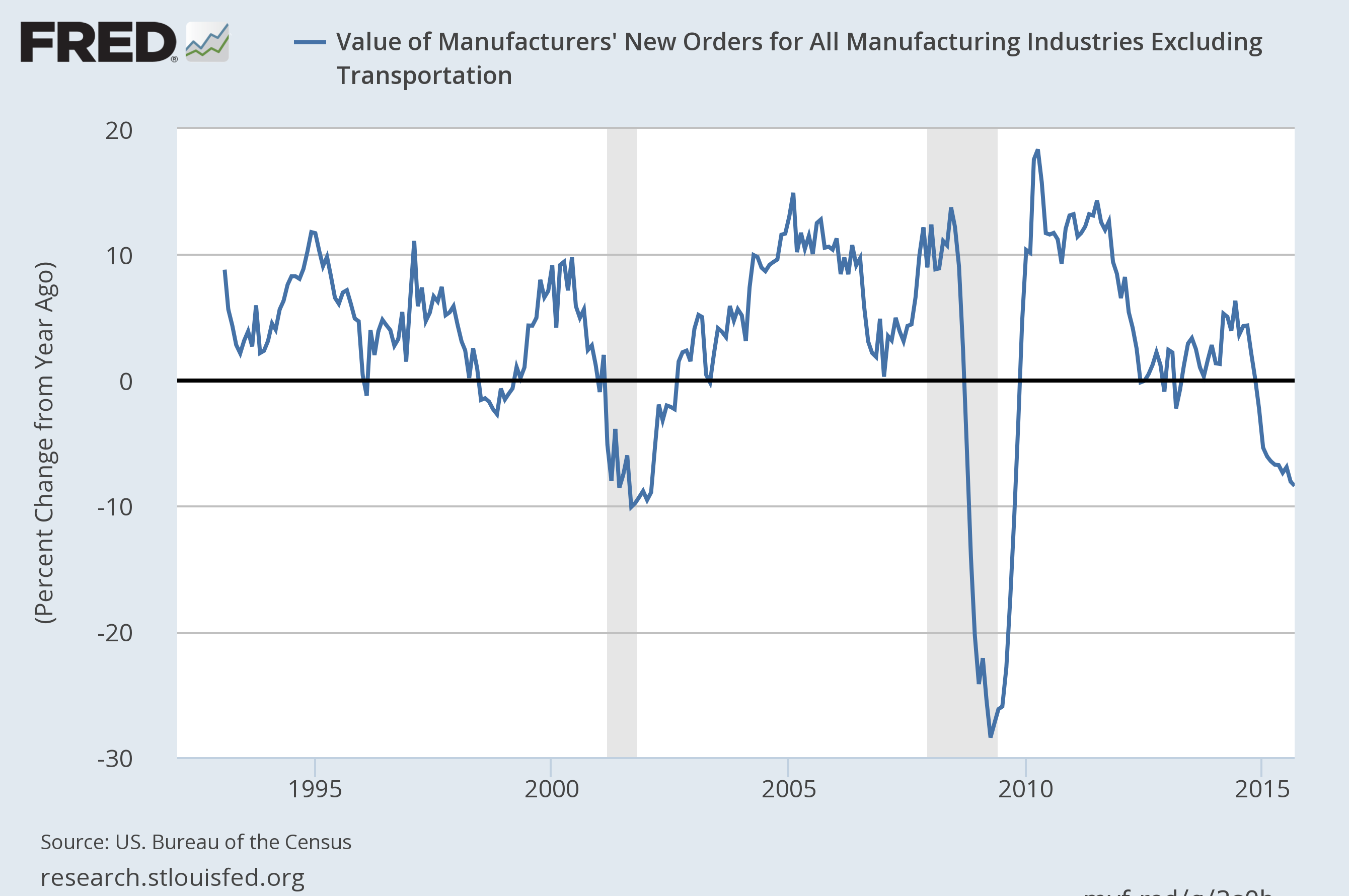

When we examine new orders as actually reported by businesses, we see similar weakness, which suggests the likelihood of slower production in response. The chart below shows the year-over-year growth of manufacturers new orders excluding transportation (new orders are down year-over-year even including transportation but aircraft orders are particularly volatile and add month-to-month noise).

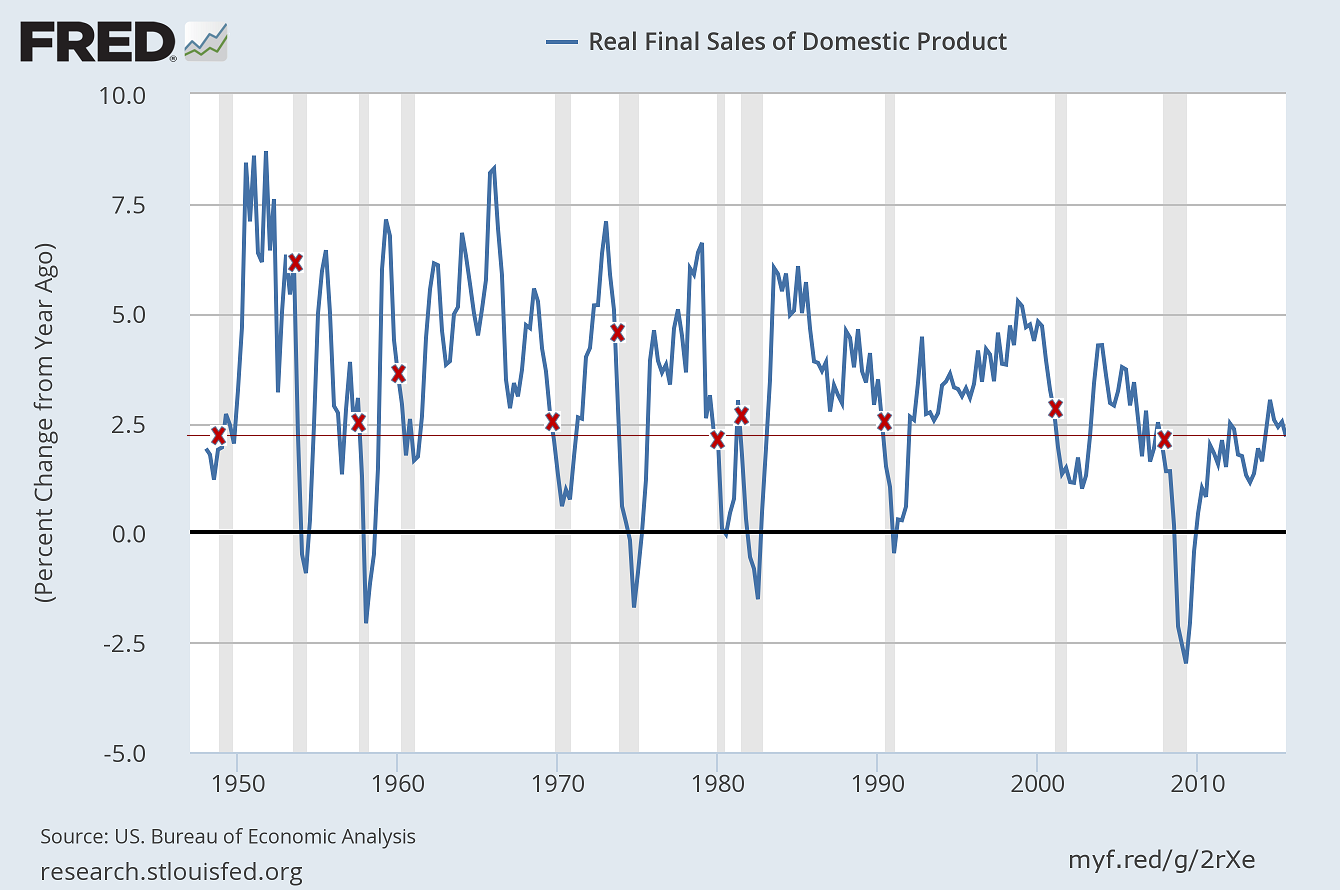

The deterioration in new orders and order backlogs is now well-developed, and these are leading indicators of economic activity. Sales, production and income are coincident indicators, and are presented below. Note first that while real final sales are not contracting, they rarely show year-over-year contraction until well into a recession (if at all). Indeed, the current level of year-over-year growth in real final sales is already equal to or below the level observed at the beginning of prior U.S. recessions. That said, we also observed a greater slowdown a few years ago that was not associated with a fresh recession, so the current slowdown may prove to be a false signal. We would infer a much higher probability of an economic contraction if current economic data was coupled with fresh equity market weakness.

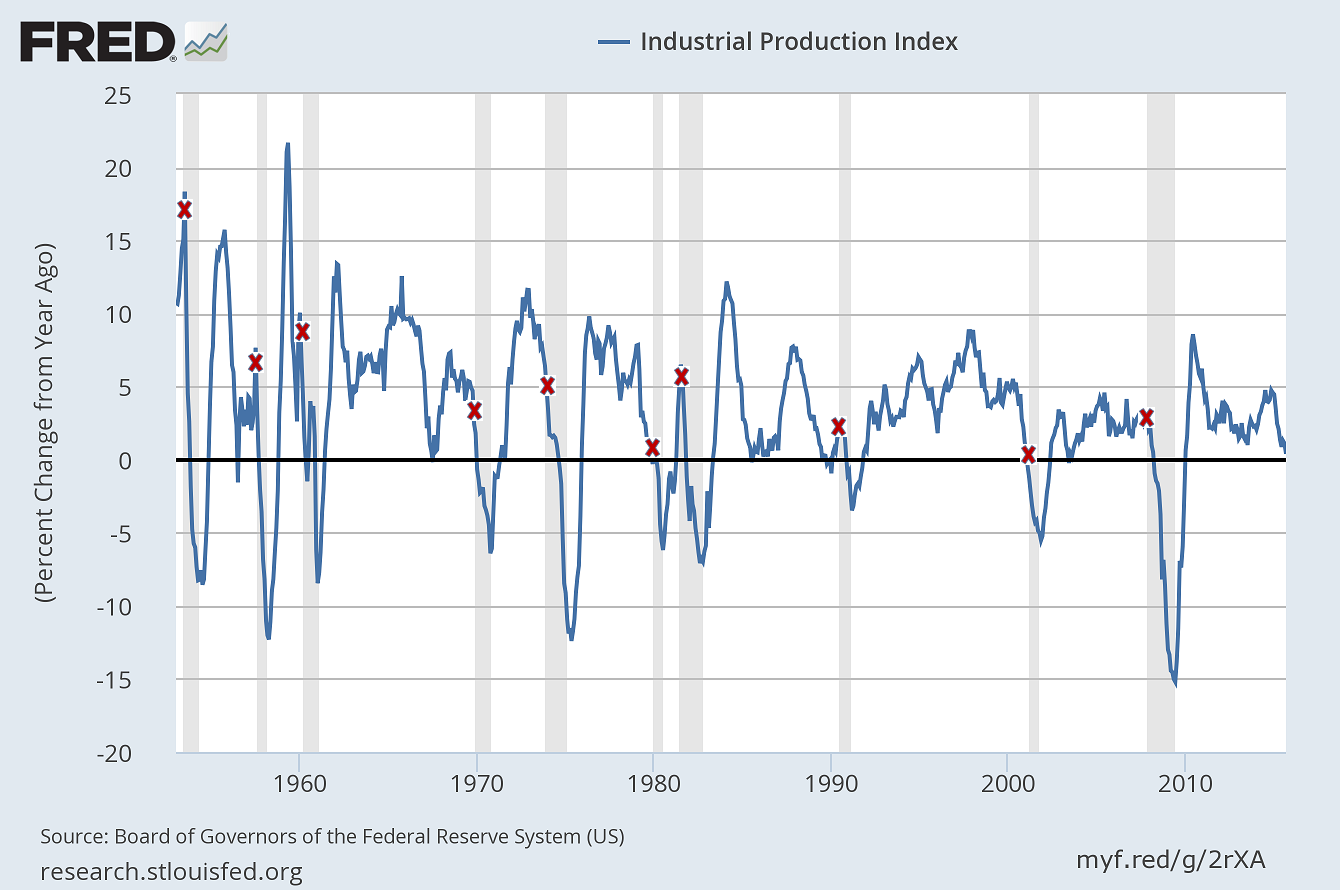

Similarly, we don’t presently observe a year-over-year decline in industrial production, but note that the current rate of growth is already below the level that prevailed at the beginning of prior U.S. economic recessions.

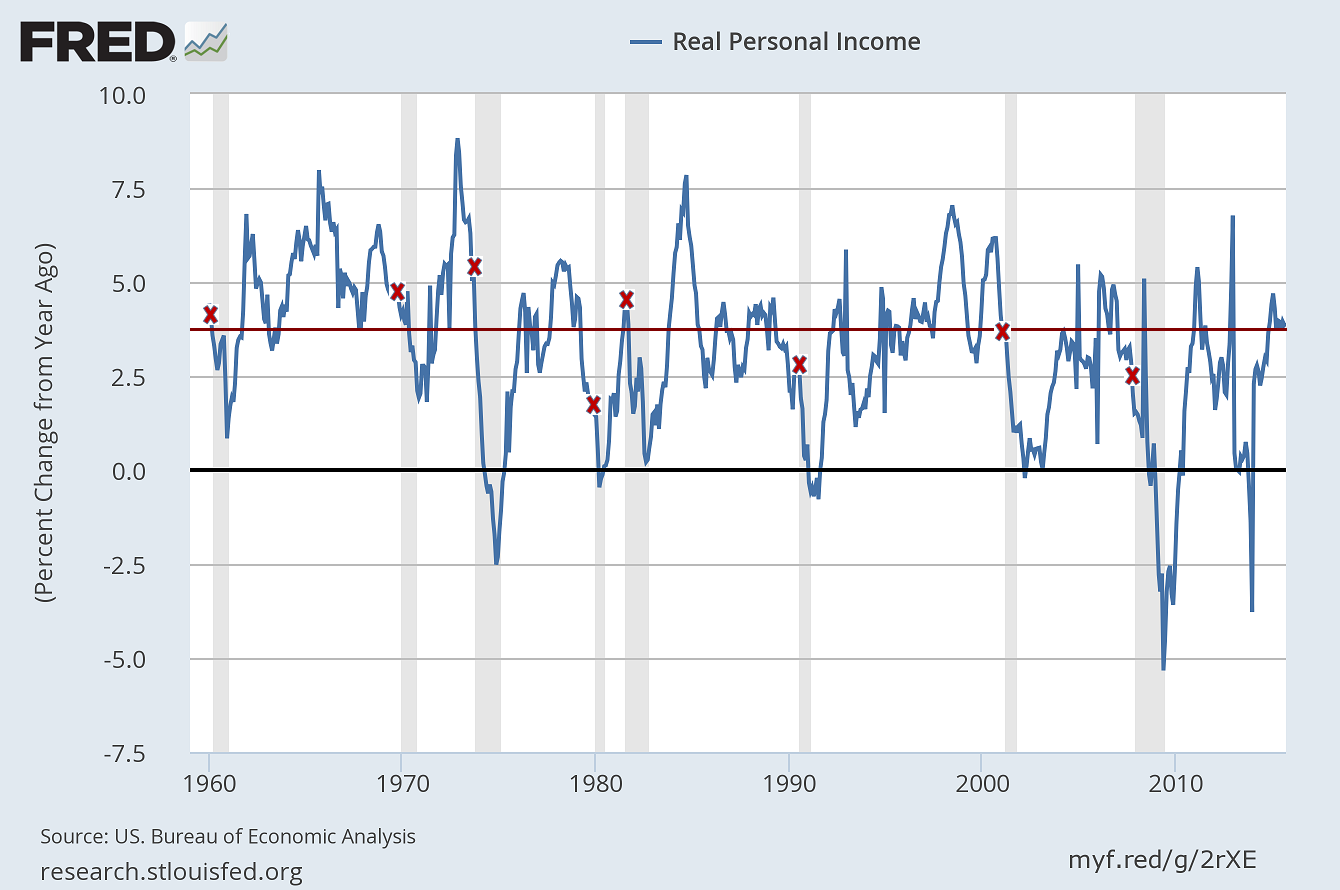

Real income is more volatile, yet only occasionally contracts outright during recessions. At present, we don’t observe a material slowing, which would normally accompany the start of a recession. In the sequence of economic events that normally precede an economic downturn, our expectation is that real income — not yet employment — is most likely the next economic measure that is vulnerable to deterioration.

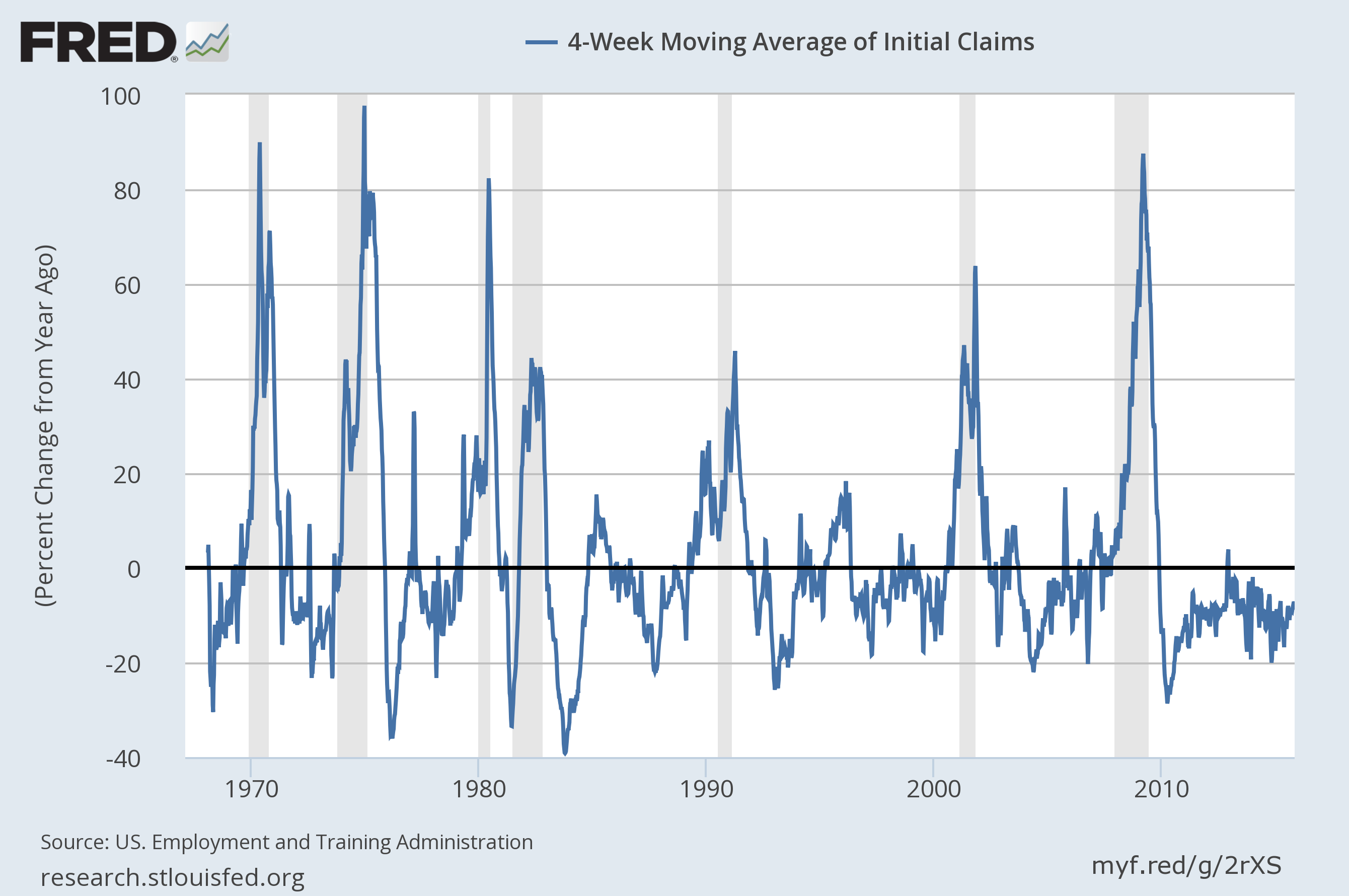

Moving to employment measures, investors should recognize that these are always the last to deteriorate and the last to improve during the economic cycle. Among them, new claims for unemployment tend to move first, with payrolls following later, and the unemployment rate moving last. New claims for unemployment tend to spike rapidly as a recession emerges. Accordingly, a year-over-year increase in new claims of about 20% (which would currently equate to a level of about 340,000 weekly new claims) would create a significant concern of a new recession in progress, particularly if coupled with other evidence such as equity market weakness and slowing growth in real personal income.

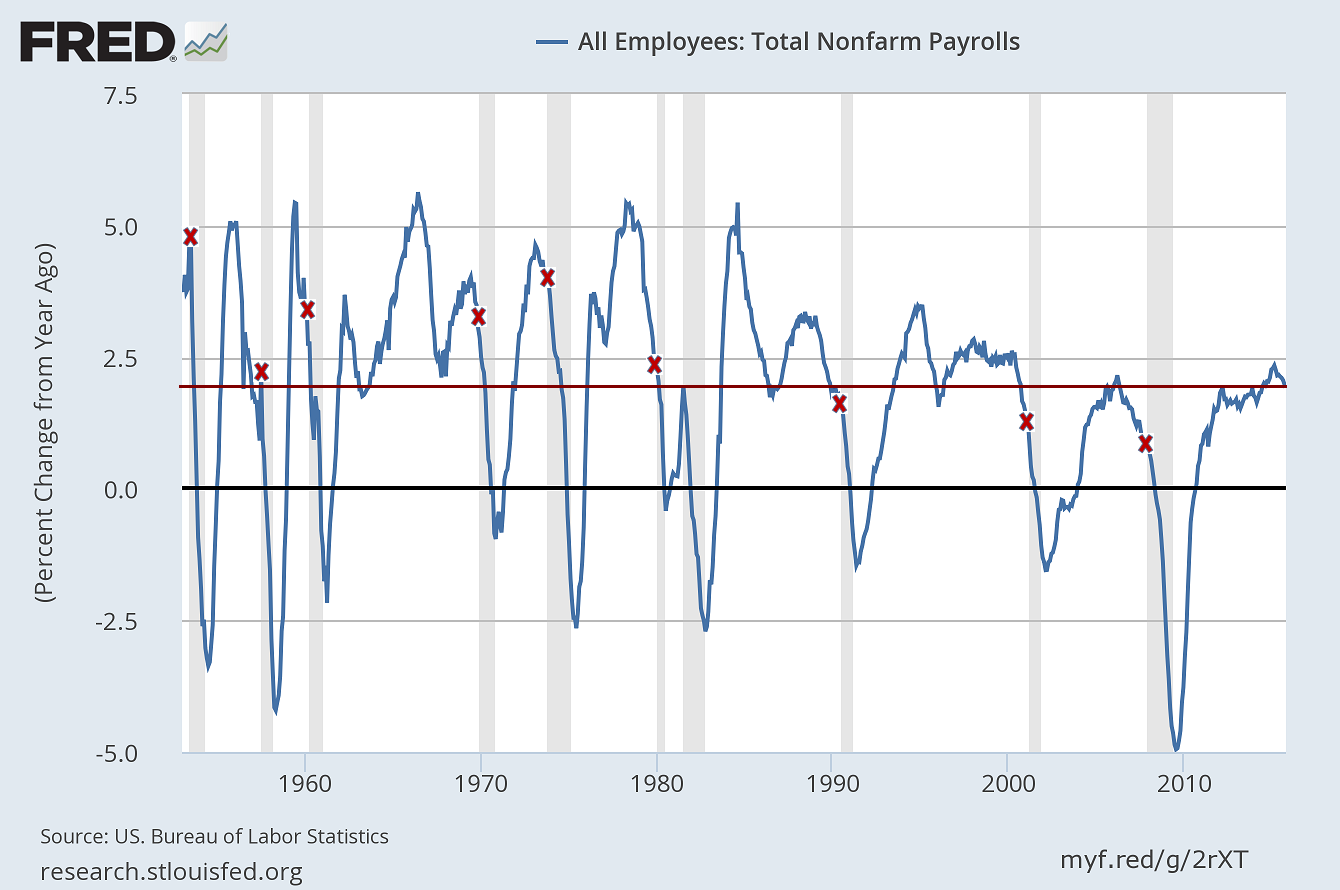

Finally, note that we typically do not observe a year-over-year decline in non-farm payrolls until a recession is already well underway, and payroll losses don’t moderate until the recession is already over. Emphatically, payrolls are among the most lagging economic indicators available. The majority of U.S. recessions have started with year-over-year growth in nonfarm payrolls above current levels. Only the three most recent recessions began at lower growth rates.

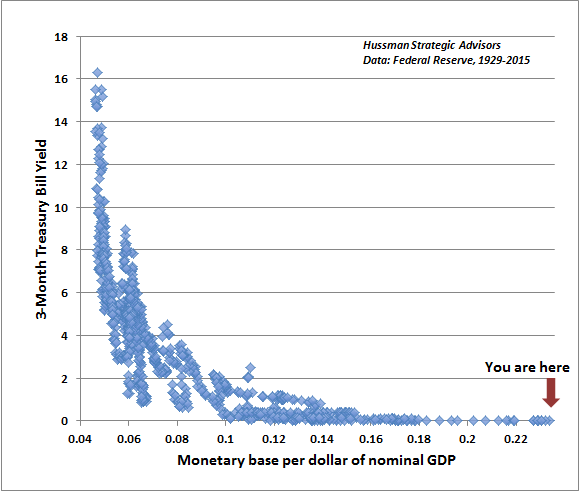

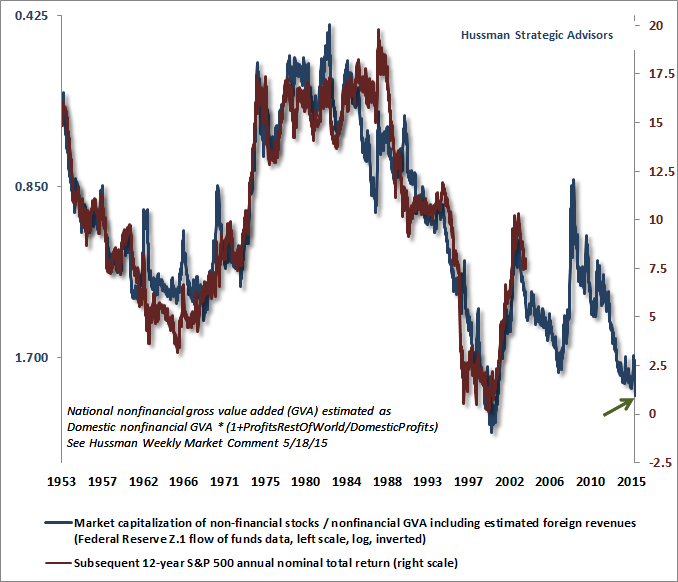

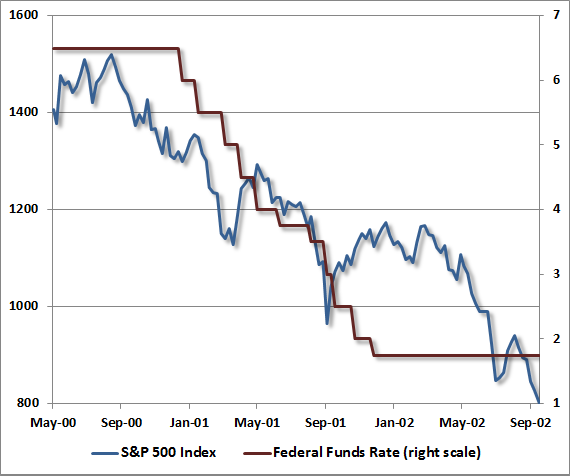

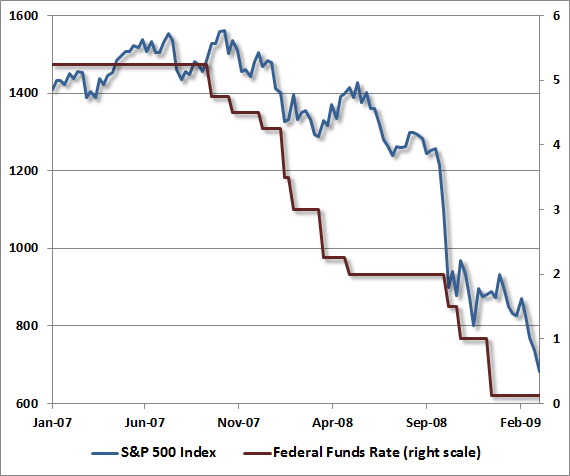

I’ll emphasize again that while I do view the economic picture as being consistent with progressive deterioration and a growing risk of recession, there is presently not enough evidence to expect a U.S. recession. Among the evidence that would shift our expectations in this regard would be: material equity market deterioration, further weakness in regional Fed and purchasing managers indices, a slowing in real personal income, a spike in new claims for unemployment toward the 340,000 level, an abrupt drop in consumer confidence about 10-20 points below its 12-month average, and at least some amount of slowing in employment growth and aggregate hours worked. For now, the main point is that the whiplash that investors are feeling with respect to the economy largely reflects the lack of distinction being made between leading and lagging measures of economic activity. Payroll reports, in particular, are among the most lagging indicators available. They don’t inform investors where the economy is going, particularly when they are at odds with leading measures such as new orders and order backlogs. Instead, employment data largely reflect the general condition of the economy months earlier. Notes on Federal Reserve policy As for the Federal Reserve, there is simply no evidence in the historical data that activist departures of monetary policy from relatively straightforward rules (such as the Taylor Rule) have any impact on the real economy. Frankly, I believe that the Fed should have raised rates years ago. Emphatically, the next recession, the next equity bear market, and the accompanying collapse in low-quality covenant-lite debt will not be the result of the Fed tightening rates, but will instead be part of economic and financial dynamics that are already baked in the cake. My view is that even if the Fed does not, by December, have the same case for raising rates as the recent employment report seems to provide, the Fed should in any event immediately discontinue reinvesting principal as assets on the Fed’s balance sheet mature. Holding the Fed’s balance sheet constant, the only way to raise rates is to pay banks interest on idle excess reserves, and the main effect of that will simply be to draw currency into the banking system and make excess reserves even larger than they already are. In my view, raising interest on reserves isn’t the first priority anyway. Without hiking the amount that the Fed pays banks to hold idle bank reserves, the Fed would have to contract its balance sheet by about $1.4 trillion before market forces would raise rates even to a fraction of 1%. In other words, fully $1.4 trillion of needless excess zero-interest liquidity could be removed from the financial system without pressuring rates higher (chart). That removal would go a significant way toward reducing the mountain of zero-interest hot potatoes that have provoked economically fruitless and financially reckless speculation. As long as zero-interest reserves are in circulation, somebody has to hold them at every point in time. The only way to get rid of them is to pass them on to someone else, typically by buying a more speculative security, at which point the seller of that security receives the zero-interest cash. Fed-induced yield-seeking speculation is precisely what drove investors to seek refuge in mortgage securities, provoked the housing bubble, and ultimately produced the worst economic collapse since the Great Depression. Anyone who doesn’t recognize that the Federal Reserve has done the same thing again — this time focused on the U.S. equity market and the market for low-grade junk and covenant-lite debt — is not paying attention to historically reliable data. On valuation measures most strongly correlated with actual subsequent S&P 500 nominal total returns, we presently expect negative total returns for the S&P 500 on a 10-year horizon, and total returns averaging only about 1% annually over the coming 12-year period (chart). The Fed has not raised future investment returns; it has encouraged speculation that has raised current prices. This has lowered prospective future investment returns to zero or negative levels on equities and low-grade debt for the foreseeable future. In essence, the economic value of time has been driven to zero. The incentive to save has been trampled. The Fed seems to want this in order to discourage investors from saving and encourage them to spend. Investors who refused to take the speculative bait may have been the first casualties of the Fed’s policies. But now, it is investors who remain fully invested in obscenely overvalued equities and junk credit that have become the unwitting dupes in this game. If the Fed cannot force people to abandon saving behavior with zero interest rates, some members of the FOMC have openly talked about driving interest rates to negative rates to “stimulate” spending. This is not economics, it is megalomaniacal sociopathy. Centuries of economic history warn that this speculative episode, too, will end in a collapse. Look — despite our enviable position in 2009, having anticipated both the 2000-2002 and 2007-2009 market plunges (and recessions) as well as the advance in-between, we still had to learn the hard way in recent years not to block the path of reckless speculation as long as it’s sufficiently robust to produce uniformly favorable market internals — even if we view valuations as obscene and the economic theory behind the speculation to be wholly counterfactual. Unlike prior cycles across history — and this was really the difficulty in this half-cycle — even extreme overvalued, overbought, overbullish syndromes were not enough to counter the speculative siren’s song of QE, provided that market internals were favorable. On the other hand, both historically and even since 2009, when investors have shifted toward risk-aversion, as evidenced by divergent market internals, rich valuations and fragile economic foundations have typically resulted in steep market losses. It’s tempting to believe that Fed easing can bail the economy and financial markets out of the consequences of this speculation. Unfortunately, that belief requires a selective memory. Recall 2000-2002 (chart) and 2007-2009 (chart): no amount of Fed easing is supportive of stocks or the economy once investors shift to risk-aversion (because in that environment, low interest liquidity is a desirable asset rather than an inferior one). While every economy is different, investors should recognize that suppressed interest rates have never supported permanently rich stock market valuations anywhere. Recall, for example, that Japanese stocks plunged by -62% in 2000-2003 and -61% in 2007-2009 despite interest rates that never exceeded half of one percent. Every day that goes by without the Fed moving to normalize the size of its balance sheet is a day that contributes to an ultimately more destructive outcome. On a 10-12 year horizon, we expect the total return of the S&P 500 to fall short of 1% annually, and given that more than that amount is likely to represent dividends, it follows that we expect the level of the S&P 500 Index to be lower 10-12 years from now than it is today (recall a similar outcome after the 2000 peak). On a shorter horizon, market action remains unfavorable as well, which leaves prospective outcomes skewed to the downside, but we don’t need to take a particularly strong near-term view. Stocks appear to be in an extended top formation much like 2000 and 2007, so our inclination is more toward patient discipline than aggressive expectations of imminent market losses. On the economic front, I believe that the most consistent interpretation of the data is that of an economy that is generally deteriorating, but where the weakness in leading indicators hasn’t filtered through to the most lagging ones. It’s unclear how much evolution we’ll observe in this process by December, and therefore it’s unclear whether the Fed will still have an apparent “case” to raise rates at that time. From an economic standpoint, I don’t believe it matters, and even from a financial standpoint, I think that the Fed has already done irrecoverable damage that will have its consequences over the completion of this market cycle. At best, the Fed can mitigate additional damage by moving more quickly to cease reinvesting principal as assets on its balance sheet mature. If market internals improve, we’ll take a signal that investors have shifted back to risk-seeking, and that would ease our near-term concerns, but wouldn’t materially change our expectations for a market loss on the order of 50% or more over the completion of the current cycle. We’ll change our outlook as the evidence changes.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}