|

|

||||||

|

|

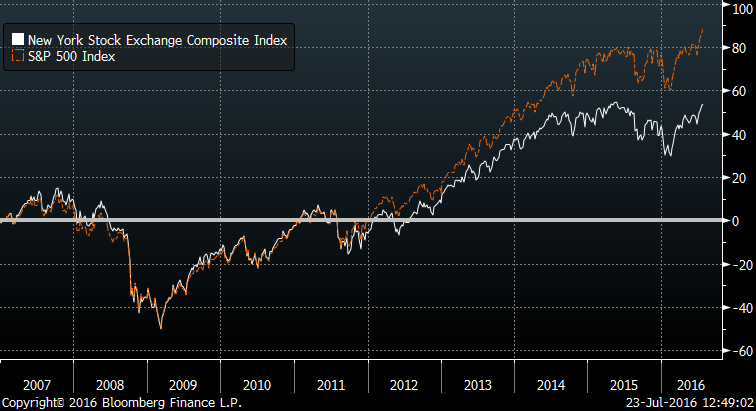

July 25, 2016 Speculative Extremes and Historically-Informed Optimism There’s a field in one of our data sets that rarely sees much play, being driven primarily by only the most extreme combination of overvaluation, overbullish sentiment, and overbought conditions we’ve identified across history. It’s one of a variety of such syndromes we track, and I’ve simply labeled it “Bubble,” because with a single exception, this extreme variant has only emerged just before the worst market collapses in the past century. Prior to the advance of recent years, the list of these instances was: August 1929, the week of the market peak; August 1972, after which the S&P 500 would advance about 7% by year-end, and then drop by half; August 1987, the week of the market peak; July 1999, just before an abrupt 12% market correction, with a secondary signal in March 2000, the week of the final market peak; and July 2007, within a few points of the final peak in the S&P 500, with a secondary signal in October 2007, the week of that final market peak. The advancing segment of the current market cycle was different in its response to historic speculative extremes. Air-pockets, panics and crashes had regularly followed these and lesser “overvalued, overbought, overbullish” extremes in every previous market cycle, and our reliance on that fact became our Achilles Heel during the advancing half of this one. In an experiment that will ultimately have disastrous consequences, the Federal Reserve’s policy of quantitative easing intentionally encouraged yield-seeking speculation in this cycle far beyond the point where these warning signals emerged. In other cycles across history, patient adherence to a value-conscious, historically-informed investment discipline was rewarded, if occasionally after some delay. In the advancing portion of this cycle, Ben Bernanke’s blind, stubborn recklessness made patient adherence to a value-conscious, historically-informed investment discipline itself indistinguishable from blind, stubborn recklessness. In mid-2014, we adapted our own investment discipline to address this challenge (see the “Box” in The Next Big Short for the full narrative). While lesser overvalued, overbought, overbullish syndromes in 2010 and 2011 were followed by significant market losses, the pattern changed once the Fed drove short-term interest rates to single basis points. In the face of these near-zero interest rates, one had to wait for market internals to deteriorate explicitly (indicating a shift toward risk-aversion among investors) before adopting a hard-negative market outlook. In a series of signals between late-2013 and the beginning of 2014, that rare “Bubble” signal emerged again. This time, however, it was accompanied by quantitative easing, a Treasury bill yield averaging just 0.03%, and uniform market internals across a broad range of individual stocks, industries, sectors, and security types (when investors are inclined to speculate, they tend to be indiscriminate about it). The S&P 500 retreated, but by just 3%, followed by an advance for several more months until market internals deteriorated early in the second-half of 2014. Since then, the broad market has essentially gone sideways, though capitalization-weighted indices such as the S&P 500 have recently clawed to new highs on enthusiasm about negative interest rates abroad (which I believe actually reflect fresh deterioration in global economic conditions across Britain, Europe, Japan, and China). Last week, market conditions joined the same tiny handful of extremes that defined the 1929, 1972, 1987, 2000 and 2007 market peaks. Still, the false signal near the start of 2014 (and lesser extremes before then), helpless in the face of single basis-point Treasury bill yields and uniform market internals, encourages a certain level of humility and flexibility. It’s clear that at least between late-2011 to mid-2014, the Fed engineered an environment that disrupted the typical response to extreme and previously reliable warning signs. In 2010 and 2011, lesser overvalued, overbought, overbullish extremes were followed by significant market losses, even though Treasury bill yields were only in the range of 10-15 basis points. In contrast, between late-2011 and mid-2014, T-bill yields averaged less than 5 basis points, and the majority of the intervening market gains overlapped the roughly one-third of that span when our present, adapted measures would encourage a constructive outlook (largely on the basis of favorable market internals). Currently, Treasury bill yields are about 30 basis points (higher than in 2010 and 2011), and while certain trend-following measures are favorable here, our overall evaluation of market internals is still mixed. Put simply, the mitigating factors are weaker here, but it’s not entirely clear what happens next. As Pauline Boss and Pema Chodron have both observed in different contexts, the only way to find peace in the face of ambiguity is the willingness to hold two diametrically opposed ideas in your mind at the same time: First, regardless of short-term speculation, the present yield-seeking speculative extreme is likely to be seen in hindsight as one of the three most reckless financial bubbles in U.S. history, on par with the 1929 and 2000 extremes. The present market cycle is likely to be completed by a collapse where a wholly run-of-the-mill outcome would be a decline of 40-55% in the S&P 500 Index. On the basis of valuation measures most tightly related to actual subsequent long-term market returns, we also estimate that the S&P 500 is likely to be lower 12 years from now, compared with current levels, though dividend income may push the total return just over zero on that horizon. We view all of these outcomes as unavoidably baked-in-the-cake as a consequence of current extremes. Despite this outlook, the uncomfortable possibility of further short-term speculation still exists. The extent to which we make that allowance is dependent on market internals and interest rate conditions. For now, they remain less supportive than speculators may imagine. As I detailed several months ago in Reversing the Speculative Effect of QE Overnight, moving the target Federal Funds rate from zero to 0.25% quietly (and perhaps inadvertently) had an effect that is observationally-equivalent to removing $1.7 trillion from the Federal Reserve’s balance sheet, back to where it was in 2009. A return to a zero target by the Fed would create greater pressure to speculate than remains at present. As for market action, despite record highs in capitalization-weighted indices, the broad market has had less traction, particularly since mid-2014. A more uniform improvement in market internals (reflecting indiscriminate speculation) could signal more durable risk-seeking among investors. The chart below shows the behavior of the broad-based NYSE Composite versus the S&P 500 Index (which has been more heavily driven by speculative, large-cap components). The performance gap that has blown out between these two indices is not just an indication of dispersion, but particularly since mid-2014, has also been a major, if temporary, headwind for hedged-equity strategies that hold a broadly diversified portfolio of stocks and hedge using the major indices. As of Friday’s close of 10805.04, the NYSE Composite remains below its June 2014 level of 11104.09, as well as its May 2015 record of 11239.66.

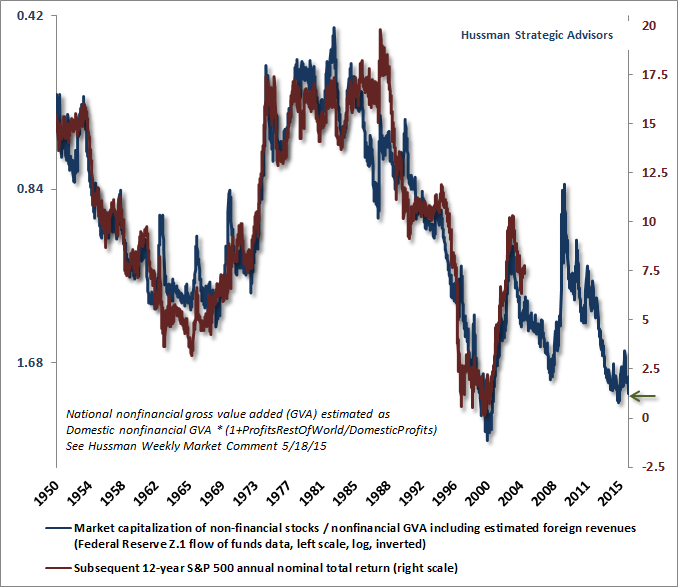

Fortunately, the ambiguity between long-term and near-term factors can be managed, because implied option volatility is just 12% and just 15.8% going out several months, which makes hedging market risk (or establishing negative exposures for those so inclined) unusually inexpensive, particularly in the context of strenuously overbought conditions, extreme valuations, and the potential for profound downside losses. To be clear, there’s no certainty that we’ve seen the last of the frantic yield-seeking panic that followed the post-Brexit shock to economic prospects, so there is risk to any investment position other than cash. Still, the rare extremes of current overvalued, overbought, overbullish conditions here, coupled with the absence (at least at present) of the factors that deferred their consequences between late-2011 to mid-2014, suggest that we may be observing the best opportunity to exit the U.S. stock market that investors will see in a generation. One can object; didn’t I incorrectly believe the same thing years ago, when similarly extreme conditions emerged with no consequence? Yes, I did. In mid-2014, I imposed conditions related to interest rates and market internals to avoid an excessive reliance on overvalued, overbought, overbullish syndromes. Unlike the 2011-2014 period, we’re not inclined to maintain a hard-negative outlook in response to overvalued, overbought, overbullish conditions if those mitigating factors are present, so our downside concerns will be deferred if market internals improve sufficiently, particularly if the Fed was to cut rates at these levels. Those adaptations would have changed our outlook during much of the recent half-cycle. But be careful about dismissing historically reliable evidence of obscene valuations and speculative extremes on the basis of that difficult narrative. Both a century of history, and our own experience in full market cycles before the recent half-cycle advance, argue against complacency here. Stronger market internals, particularly coupled with a move back to a zero Federal Funds target, would encourage at least a temporary surrender to speculative forces (albeit with a tight safety net if it was to occur near current valuations). I actually think it’s likely that we’ll see this combination over the completion of the current market cycle, but only after a steep retreat in valuations. That combination of improved valuation and early improvement in market action emerges over the completion of every market cycle, and is associated with the strongest estimated market return/risk profile we identify. As for the enticing concept of “helicopter money,” my impression is that many observers are using the term with no understanding of what they are talking about. Despite the uninhibited imagery it evokes, “helicopter money” is nothing but a legislatively-approved fiscal stimulus package, financed by issuing bonds that are purchased by the central bank. Every country already does it, but the size is limited to the willingness of a legislature to pursue deficit spending. Central banks, on their own, can’t “do” helicopter money without a spending package approved by the legislature. Well, at least the Federal Reserve can’t under current law. To some extent, Europe and Japan can do it by purchasing low-quality bonds that subsequently default, but in that case, it’s a private bailout rather than an economic stimulus. See, those central banks have resorted to buying lower-tier assets like asset-backed securities and corporate debt. If any of that debt defaults, the central bank has given a de facto bailout, with public funds, to the bondholder who otherwise would have taken a loss. So almost by definition, low-tier asset purchases by the ECB and Bank of Japan act as publicly-funded subsidies for bondholders, rather than ordinary citizens. My sense is that if the European and Japanese public had a better sense of this, they would tear down both central banks brick-by-brick. As for the U.S., I’d actually be quite comfortable with a reasonable amount of “helicopter money” provided that the accompanying fiscal stimulus package was focused, not on consumption, but on productive investment at the public, private and individual level (infrastructure, investment and R&D tax credits, workforce training, education, and so forth). It’s the absence of productive real investment, which since 2000 has slumped to a small fraction of its historical growth rate, along with the encouragement of rank yield-seeking speculation by the Fed, that has repeatedly injured the U.S. economy, and is likely to insult the economy with further crises before any durable lessons are learned. Here and now, really the only factor that mitigates crash risk, and encourages us to refrain from pounding the tables about immediate market loss, is that some trend-following components in our measures of market internals have become constructive during the recent advance, though not enough - at least as yet - to shift their overall status. In the absence of stronger mitigating conditions, mirroring the late-2011 to mid-2014 period, the decision-making of investors should consider the breathtakingly negative outcomes that have generally followed similarly overvalued, overbought, overbullish extremes. In any event, don’t allow your decision-making to be driven by “fear of missing out” at what is already one of the most extreme points of speculative overvaluation in history. The current half-cycle market advance is remarkably long-in-the-tooth. There little basis for investment at these valuations - only speculation. Without a strong safety net, that speculation amounts to an attempt to gather pennies under a chainsaw. In recent weeks, we’ve heard some rather ignorant talk of an ongoing “secular bull market” that presumably has years to go. Unfortunately, these analysts don’t appear to recognize that secular bull markets have typically started from valuations literally one-quarter of their present level (see 1949 and 1982), and far below those observed at the 2009 low. With the exception of the 2000 extreme, every secular bull market has died before reaching even the current level of valuations. Moreover, even if this were a secular bull, one would still expect a cyclical bear from current extremes. By our estimates, investors can expect to scrape out scarcely more than 1% in nominal annual total returns in the S&P 500 Index over the coming 12-year period. We expect that all of this will be from dividends, and that investors will experience a steep roller-coaster of drawdowns and volatility in the interim. The index itself is likely to be below current levels 12 years from today. Even the lowly returns available from cash will likely serve investors better. Of course, we expect the discipline of investing in alignment with the market’s expected return/risk profile, as it changes over the course of the market cycle, to do far better still. As I’ve noted many times, only a pessimist believes that investors are forever doomed to suffer these elevated valuations and dismal long-term return prospects. Only those who are historically uninformed believe that valuations have no relationship to subsequent returns, or place their faith in scraps of analytical debris like the “Fed Model” without examining their poor correlation with actual subsequent market returns. Conversely, it is an act of historically informed optimism to expect this market cycle, like all market cycles, to be completed. Every market cycle in history has drawn valuations to levels that have offered disciplined investors far higher return prospects than are available at present. Because prospective 12-year annual market returns have never failed to reach at least 8% by the completion of a market cycle, regardless of the level of interest rates, we view a 40% market decline as a rather minimal target over the completion of this market cycle. Even a 55% loss would be merely run-of-the-mill from current extremes. We recognize that short-term speculative factors will periodically mitigate the immediacy of these risks, and we’ve adapted to that. We wouldn’t rely too much on this at present, but we’ll take new evidence as it comes. The chart below is a reminder of where the most reliable measures of valuation stand, comparing the current ratio of nonfinancial market capitalization to corporate gross value-added (blue line, on an inverted log scale), along with the actual subsequent S&P 500 nominal annual total return over the subsequent 12-year period (red line, right scale).

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |