|

|

||||||

|

|

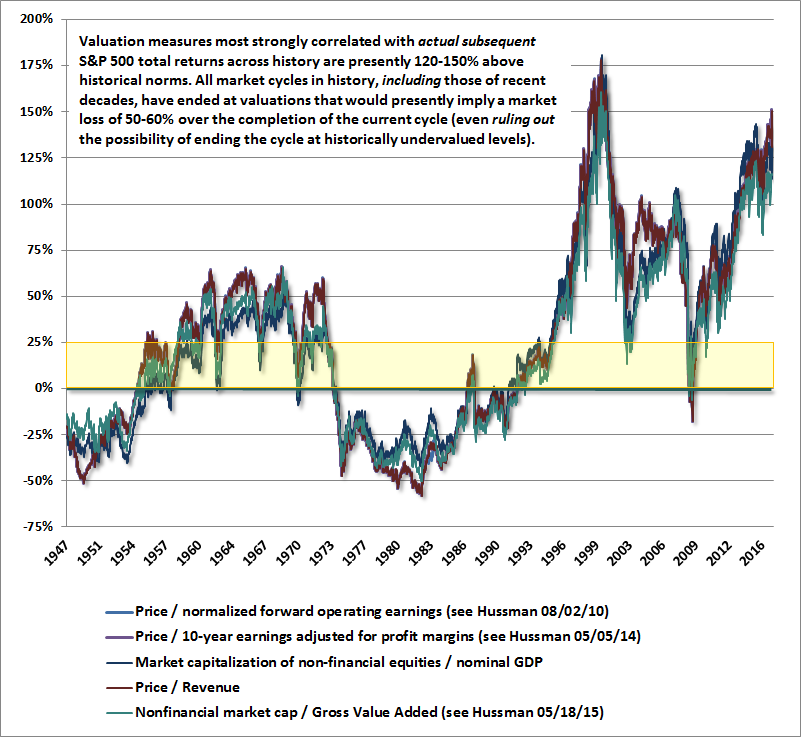

January 9, 2017 The Economic Risk of Ignoring Arithmetic “Let us not, in the pride of our superior knowledge, turn with contempt from the follies of our predecessors. The study of errors into which great minds have fallen in the pursuit of truth can never be uninstructive... Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one... Truth, when discovered, comes upon most of us like an intruder, and meets the intruder’s welcome... Nations, like individuals, cannot become desperate gamblers with impunity. Punishment is sure to overtake them sooner or later.” Charles MacKay, Extraordinary Popular Delusions and The Madness of Crowds, 1841 When we observe the greatest follies of our predecessors, the episodes of speculative madness that come most immediately to mind are the pre-crash bubble peaks of 1929, 2000, and to a lesser extent, 2007. Unfortunately, we are in the midst of yet another episode of equivalent speculative madness, but one that will only be recognized in hindsight, and in the recollections of our children. They too are likely to take pride in a feeling of superior knowledge, forgetting the same lessons, and eventually creating another bubble and collapse of their own. The herd mentality is human nature. As in 2000-2002 and 2007-2009, when the S&P 500 collapsed by 50% and 55% respectively, we’ll likely see that herd mentality expressed on the downside soon enough. That also is human nature. The stock market bubble that ended with the September 1929 peak began in August 1921, running just a few days beyond 8 years in duration. The bubble that ended with the March 2000 peak began in October 1990, running fully 9 years and 5 months in duration. Those two episodes represent the longest bull markets in U.S. history. The current half-cycle began at the March 2009 low, and has now run 7 years and 10 months in duration, making it the third-longest advance in history, placing it just 2 months short of the 1929 instance, but a full year and 7 months short of the 2000 instance. What’s notable here is that by the time the bubbles that ended in 1929 and 2000 reached a duration similar to the present, they were already experiencing a significant increase in volatility and the frequency of corrections. From a time-perspective, for example, 7 years and 10 months into the bull market that began in October 1990, it was August 1998, about the point that the S&P 500 took a nearly 20% dive. By July 1999, the S&P 500 had eclipsed its mid-1998 high, followed by a correction of over -12% during the next 13 weeks (taking the net gain from mid-1998 to just 5%). The S&P 500 then rallied again into December 1999, followed by a nearly -10% correction over the next 8 weeks. Immediately after the final market high in March 2000, the S&P 500 quickly gave up more than 11% in the following month, wiping out a year of gains, and the bear market had hardly even started. Likewise, by the time the bull market from the 1921 low extended into late-1928, the market became much more susceptible to corrections. Following a peak in November 1928, the Dow Jones Industrial Average lost nearly -13% in a month. The next peak in February 1929 was followed by a -8% correction over the following two weeks. A fresh high in May 1929 was followed by a -10% correction over the following four weeks. The final high in September 1929 was followed by an initial drop of nearly -15% over the next 6 weeks. Put simply, once the bull market was as mature as the present one has become, further market gains were not smooth. Nor were they ultimately durable. From a valuation perspective, the current run is similarly mature. The most reliable market valuation measure we’ve identified across history (having the strongest correlation with actual subsequent market returns) is the ratio of nonfinancial market capitalization to corporate gross value-added (MarketCap/GVA), with Warren Buffet’s old favorite, the ratio of market capitalization to gross domestic product, just slightly behind, followed somewhat further by a variety of measures that normalize earnings in one way or another (by comparison, neither the ratio of price/forward operating earnings nor the Fed Model even come close). By the time valuations reached levels similar to recent extremes during the advances toward the 1929 and 2000 bubble peaks, it was already mid-1929 and late-1999, respectively. The market losses over the subsequent 10-12 year periods directly reflected the extent of the corresponding overvaluation. At present, we estimate S&P 500 nominal total returns averaging just 0.8% annually over the coming 12-year horizon. If our measures of market internals were to improve materially, particularly across interest-sensitive sectors, we would be inclined to allow leeway for valuations to become even more extreme. But in the end, richer valuations would only imply steeper losses over the completion of the current market cycle, and even weaker returns on a 10-12 year horizon. For a review of current valuation extremes, see Economic Fancies and Basic Arithmetic. As we enter 2017, the great risk for investors is not in missing out in an exhausted run that already rivals the 1929 and 2000 extremes, but in failing to contemplate a 50-60% market retreat over the completion of the current cycle. The chart below presents some of the most reliable valuation measures we follow, showing percentage deviations from their pre-bubble norms. S&P 500 forward earnings and revenues are imputed prior to 1980 based on their relationships with available data having a longer history. The measures below have correlations as high as 94% with actual subsequent S&P 500 total returns, particularly on a 10-12 year horizon. At present, they range between 120% and 150% above their respective historical norms. A run-of-the-mill cycle completion, even ruling out historically undervalued levels, would imply a 50-60% market loss.

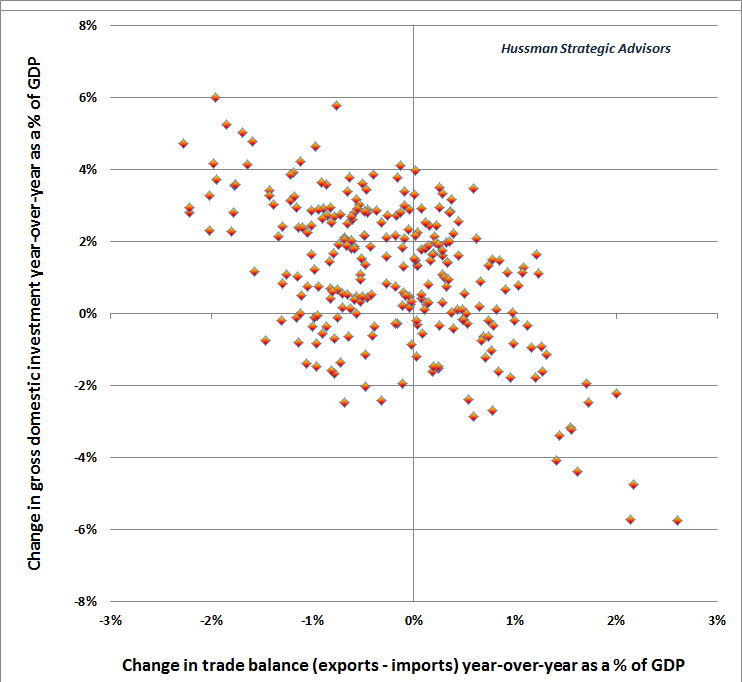

We’re certainly open to the possibility that market internals will shift to a more favorable condition (when investors are inclined to speculate, they tend to be indiscriminate about it, so the uniformity of market action across a broad range of individual stocks, industries, sectors and security types is a useful measure of investor risk-preferences). Yet while a constructive shift would at least temporarily suspend our hard-negative market outlook, a strong safety-net would remain imperative. Even in a bullish world where the current advance might extend to match or surpass the duration and valuation extremes of the 1929 and 2000 bubbles, investors should brace themselves for amplified volatility in the near-term. The economic risk of ignoring arithmetic I’ve previously detailed why arithmetic of demographics and productivity suggests a likely central tendency of less than 2% annually for real GDP growth over the coming 8 years, with even 3% growth being both optimistic and rather implausible. Increased allocation of savings toward productive investment would certainly benefit the country over a period of decades, but is unlikely to materially alter the course of economic growth over the span of a few years. In my view, the primary economic risks here are clearly to the downside: years of Fed-induced yield-seeking speculation have already set the financial markets up for an equity market collapse on the order of 50-60% over the completion of the current market cycle, coupled with a secondary crisis in a mountain of covenant-lite debt, as the indebtedness of U.S. corporations (even after netting out cash holdings) has been driven to record levels relative to corporate gross value-added. To understand our muted enthusiasm about the economy here, recall that GDP growth is driven by the sum of employment growth and productivity growth. While there may be some vicarious gratification in the idea of “getting tough” with companies about domestic jobs and imports, the fact is that even if we assume a 2% unemployment rate in 2024, built-in labor force demographics would still limit annual growth in U.S. employment to just 0.7% annually in the interim. That demographic fact will not be altered by the disturbing practice of singling individual companies out for intimidation, as a substitute for informed, uniform policies and equal treatment under the law. From an economic standpoint, the spectacle is little but a carnival sideshow, because the job numbers at issue are absurdly small relative to the ordinary turnover of the U.S. labor force. In 2016, for example, there were 5.2 million jobs created in an average month, with an average of 5 million job separations, for a net increase in payrolls averaging about 200,000 jobs per month (JOLTS data - yes, employment turnover is that high). Entertainment value aside, the likely contribution of employment growth to GDP growth in the coming years is likely to be in the range of 0.2-0.7% annually, barring an economic recession that could pull this figure to negative levels. Aside from short-run outcomes, any durable and sustained acceleration in GDP growth will have to come from productivity growth. That, in turn, is highly dependent on gross domestic investment (broadly defined to include intangible investments such as education and job-training initiatives to boost labor productivity). This is the component of economic growth that faces the largest downside risk in the coming years. See, productivity growth is highly dependent on growth in gross domestic investment, and it’s here where the incoming administration seems to have little understanding of economic arithmetic. Part of that arithmetic can be expressed as the “savings-investment identity,” which is not a theory but an accounting equality. We can state it as follows. U.S. gross domestic investment is always identical to the sum of: household savings, government savings, corporate savings, and savings acquired from foreigners. The other bit of arithmetic has to do with trade. You can think of it this way. For every dollar of “stuff” we import from foreign countries, we have to pay for it by transferring an equal value of “stuff” in the other direction. That stuff can either be goods and services, or securities. We obtain the savings of foreigners by exporting securities to them, rather than goods and services. But here’s the accounting hitch. A net import of foreign savings is equivalent to running a trade deficit. By exporting more securities than we import, we obtain foreign savings to finance U.S. gross domestic investment, but it must then also be true that we’re exporting fewer goods and services than we import. Here’s the problem: pursue a policy to reduce the trade deficit, and you automatically (and possibly unintentionally) pursue a policy to reduce the import of foreign savings. Now, that may be all well and good when domestic sectors are running surpluses. If the combined savings of households, businesses and the government are more than enough to finance our own gross domestic investment, the U.S. can run a trade surplus and can lend the excess savings to the rest of the world, becoming a net creditor. The problem is that’s not anything close to the position of the United States. Our nation relies heavily on the import of foreign savings to finance our gross domestic investment. If the new administration pursues larger fiscal deficits, that financing gap will become greater, not smaller. If it pursues larger fiscal deficits (reducing government saving to even more negative levels) while also pursuing punitive trade policies and import restrictions (reducing the import of foreign saving), the net effect will be to crowd out and sharply restrain gross domestic investment. In theory, a boost to the sum of household and corporate savings could ease the gap, but in practice, the two are negatively correlated, because the corporate share of GDP is relatively high when wages and salaries are low as a share of GDP, and also because boosting household savings by refraining from consumption tends to depress corporate earnings and resulting saving. The bottom line is that large and sustained increases in U.S. gross domestic investment have always been achieved by financing a substantial portion of the increase with foreign savings. Booms in U.S. gross domestic investment are systematically associated with “deterioration” in the trade balance. Conversely, declines in U.S. gross domestic investment are systematically associated with “improvement” in the trade balance. The chart below provides a good picture of how this relationship looks in practice, in data since 1947.

Outcomes are not independent of initial conditions. While there are certainly policy shifts that could encourage greater productive investment and raise the long-run trajectory of economic growth, no shift in economic policies is likely to produce rapid, sustained economic growth in the next few years because the underlying factors that drive rapid, sustained growth aren’t presently in a position to support it. GDP growth is the sum of employment growth plus productivity growth. Strong employment growth typically emerges when there is a relatively large pool of available and unemployed labor, because that pool of available labor provides the economy room to run. Strong productivity growth requires expansion in gross domestic investment, which in turn is enabled by deterioration in the trade deficit. As a result, rapid productivity growth typically begins from points where the trade deficit is relatively narrow or even in surplus. That’s why the economic booms following the 1982 and 1990 recessions were so strong - both expansions started from a high unemployment rate coupled with a trade surplus. At present, we’ve got a low unemployment rate and a rather deep and persistent trade deficit. Rapid growth will emerge from much different conditions than we observe at present, and one doesn’t want to be exposed to a great deal of economic risk in the interim, because the risk during that transition period is emphatically to the downside. We are left, then, with a hypervalued and mature market advance that now rivals the two greatest speculative mistakes in U.S. history; with extreme overvalued, overbought, overbullish conditions coupled with a tightening Federal Reserve and dispersion across key measures of market internals; with an incoming administration that by all evidence values spectacle and coarse provocation over diplomacy and informed, dignified leadership; and with an economic agenda so lacking in the foundations of basic arithmetic that a needless retreat in U.S. gross domestic investment may be the unintended consequence. As for stocks, last week, my friend Jesse Felder published a piece headed with a cartoon of Lucy snatching away a football while a trusting Charlie Brown tumbles upside-down after attempting a kick, imagining that this time might be different. This time will not be different. Look carefully at the advances that led to the 1929 and 2000 peaks, but look only backward, ignoring what was ultimately to come. Look at the 2007 peak, or the 1972 peak, or the 1987 peak, with the same backward-looking perspective. Overvalued bull markets lure investors to hold on precisely by convincing them that at every seemingly overvalued point in the recent past, prices have triumphed to achieve even higher levels. It’s important to recognize that during the majority of those preceding advances, extreme overvalued, overbought, overbullish syndromes were absent, and market internals typically demonstrated broadly positive uniformity, indicating that investors remained inclined to speculate despite rich valuations. In contrast, in market cycles across history, by the time extreme valuations were joined by extreme overvalued, overbought, overbullish syndromes and deteriorating market internals, whatever potential gains remained were purely transient, and were overwhelmed by losses over the completion of the market cycle. The half-cycle since 2009 was different only in that the Federal Reserve’s deranged policy of zero interest rates and quantitative easing encouraged investors to continue speculating long after extreme overvalued, overbought, overbullish syndromes emerged. The extension of this speculation was admittedly frustrating for us. In the presence of zero interest rates, one had to wait for internals to deteriorate explicitly. Even after the adaptations we introduced in mid-2014, the combination of an extended top-formation and a performance-chasing rush toward passive indexing hasn’t created much opportunity to demonstrate the benefit of historically-informed, value-conscious investment discipline. Still, we’ve demonstrated the benefits of our integrated discipline nicely in previous complete market cycles, and we remain convinced that it is well-suited to navigate the completion of this cycle and those to come. While we’re seeing persistent signs of dispersion, particularly across interest-sensitive sectors, my sense is that investors are mistaking the market gain in 2016 as a repudiation of the idea that extreme valuations, dispersion across market internals, and overextended conditions are of real concern. My own expectation is that even if there is a longer life to this bull market, the 2016 gain will be erased rather soon, in a quite ordinary late-stage correction, much like those that emerged with increasing frequency approaching other major market peaks. Our outlook will change with conditions, particularly with respect to valuations, market internals, and the presence or absence of overextended syndromes. For now, the stock market is now much like Wile E. Coyote temporarily hovering just past the edge of a cliff. The moment of descent isn’t clear, but I believe it would be a mistake to climb onto his shoulders.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |