Turtles All the Way Down

John P. Hussman, Ph.D.

President, Hussman Investment Trust

February 2019

So we have to make a distinction. If the Fed launches a fresh policy of extraordinary easing in the next downturn, the appropriate response will depend on whether market internals indicate that investors are inclined toward speculation, or whether they are inclined toward risk aversion. The central consideration here is what I call ‘uniformity’ – when investors are inclined to speculate, they tend to be indiscriminate about it. It’s difficult to get extended market advances without recruiting that kind of uniformity, but it will be important to avoid being sucked into the market in response to Fed easing alone. Historically, initial Fed rate cuts in response to a market downturn have been followed by very negative consequences (after the initial obligatory market pop), because they generally indicate that something has gone wrong.

– John P. Hussman, Ph.D., November 28, 2018

Last week, the Federal Reserve issued policy statements intended to telegraph a shift toward easier, or at least more patient monetary policy. Though Wall Street interpreted this shift as a major about-face in the Fed’s policy stance, the most significant shift in Fed Chair Jerome Powell’s statements actually occurred on November 28. Even here, we would characterize the Fed’s policy stance as neutral with a slight hiking bias, but investors should not imagine that a shift to outright easing by the Fed would necessarily be favorable for stocks.

Back on October 3, Powell alarmed investors, I suspect inadvertently, when he communicated the Fed’s efforts to normalize interest rates using these words:

“The really extremely accommodative low interest rates that we needed when the economy was quite weak, we don’t need those anymore. They’re not appropriate anymore. Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral. We may go past neutral, but we’re a long way from neutral at this point.”

Powell walked that statement back on November 28, when he described the position of rates as “just below” neutral. Following an additional rate hike by the Fed in December, Powell noted on December 20 that “We have reached the bottom end of the range of committee estimates of what might be neutral. I think from this point forward, we are going to let the data speak to us and inform the outlook.”

That “bottom of the range” view strongly aligns with our own. It’s important to recognize that what we call “structural” real GDP growth (labor force growth + trend productivity) has declined persistently in recent decades, to a level that’s now down to just 1.4% annually. All additional real GDP growth in recent years has been driven by a decline in the rate of unemployment from 10% in 2009 to the current level of just 4%. With a far smaller reservoir of “cyclical” economic slack, it’s likely that real GDP growth will slow toward that 1.4% structural rate. Any material increase in the unemployment rate would go hand-in-hand with a recession, and an outright contraction in real GDP.

As I noted in my November comment, during the relatively low-inflation period since the 1980’s, Treasury bill yields have typically stood 0.5% to 1% above real GDP growth, but slightly below nominal GDP growth. Even if one assumes that stronger productivity will push structural real GDP growth toward 2% annually, a neutral Treasury bill yield would reasonably fall in the area of 2.5-3.0%. Without a further decline in unemployment, an acceleration in productivity, or higher inflation pressures, 1.4% structural real GDP growth would put our range for “neutral” at just 1.9-2.4%. In either case, as Powell observed, short-term interest rates are already within that pocket.

That said, I certainly don’t believe that adjustments in Fed policy have very strong or reliable effects on economic outcomes, nor apparently does Powell. That’s one of the reasons I respect him more than his predecessors. He’s well aware of how loose the relationships are between Fed policy and actual economic outcomes, so he’s likely to encourage reasoned and deliberate actions rather than dogmatic and deranged experiments. He is, however, surrounded by activists, so that will be a challenge.

With regard to longer-term bonds, during the relatively low-inflation period since the 1980’s, 10-year Treasury bond yields have typically averaged about 2% to 2.5% above the rate of real GDP growth, with yields roughly equal to nominal GDP growth. In that context, a 1.4% structural real GDP growth rate coupled with 2% inflation would put the “neutral” range for 10-year Treasury yields between 3.4-3.9%. That’s clearly above the prevailing yield of just 2.6%.

In my view, current long-term rates only make sense in the context of still-aggressive monetary policy abroad, coupled with subdued expectations for U.S. growth and inflation. There may be further room for yields to fall in a recession scenario, but we don’t associate bonds with a strong expected return/risk profile here.

I certainly don’t believe that adjustments in Fed policy have very strong or reliable effects on economic outcomes, nor apparently does Powell.

This brings us to last week’s Fed policy statement. Though my impression is that the financial markets were rather over-eager in their interpretation of the Fed’s stance last week, it’s probably a distinction without a difference. As a practical matter, further Fed rate hikes appear unlikely without a surprising tightening of labor market conditions or increasing inflation pressures.

When one examines what the Fed actually said, rather than Wall Street’s interpretation of it, it becomes clear that the Fed did not actually pronounce an “end” to its normalization of rates, but merely indicated “patience.” The statement accompanying Wednesday’s meeting observed (italics mine):

“The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcome… the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate.”

In an additional statement, the Fed also attempted to clarify that it is targeting a policy regime where a massive balance sheet is no longer needed, though it did end that statement with an obligatory reassurance that all policy tools remain at its disposal:

“The Committee intends to continue to implement monetary policy … primarily through setting rates, and in which active management of the supply of reserves is not required. The Committee continues to view changes in the target range for the federal funds rate as its primary means of adjusting the stance of monetary policy. The Committee is prepared to adjust details for completing balance sheet normalization in light of economic and financial developments. Moreover, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet, if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate.”

In the news conference that followed, Fed Chair Jerome Powell also took pains to reiterate that the Fed’s intention is to move away from the policy of quantitative easing, observing that the Fed’s goal is to have “a balance sheet no larger than it needs to be for us to effectively and efficiently conduct monetary policy.”

So again, in contrast to Wall Street’s interpretation that Wednesday’s statement by the Fed represented a massive policy change, the actual shift, to the extent there was one, occurred back in November.

Fed easing is not always “good” for stocks

Remember that while valuations are the main determinant of long-term investment returns, market outcomes over shorter segments of the market cycle are heavily dependent on whether investors are inclined toward speculation or risk-aversion. That inclination is wholly psychological. We read that psychology out of the behavior of market internals, because when investors are inclined to speculate, they tend to be indiscriminate about it.

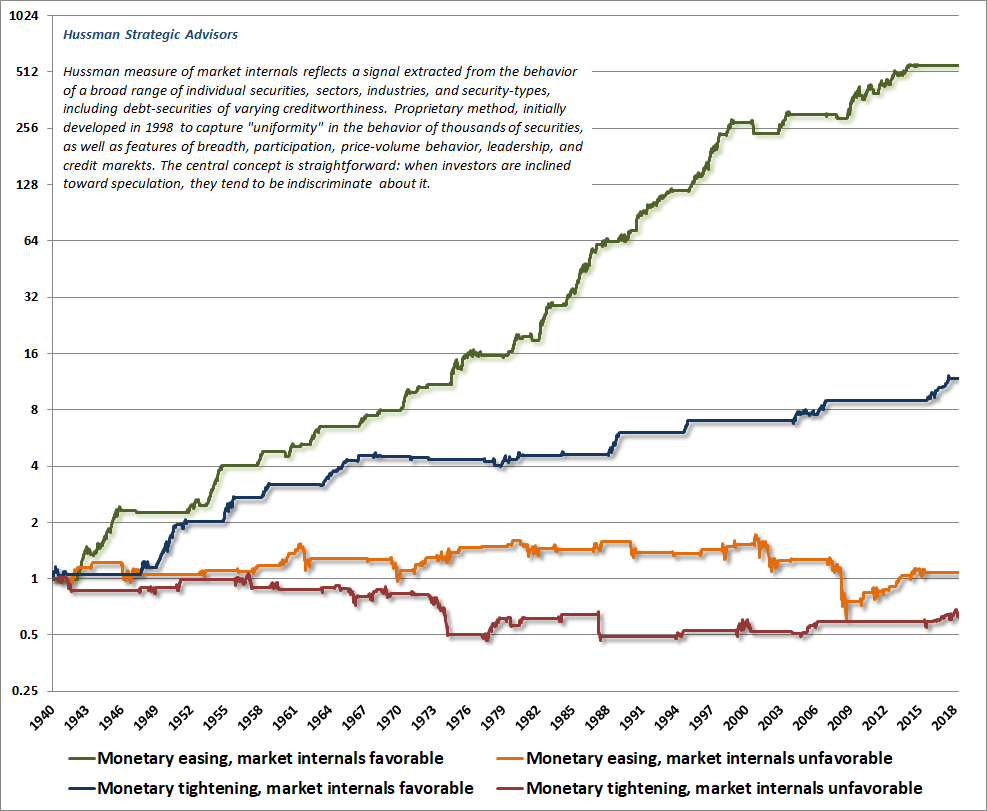

As I’ve demonstrated previously, even a shift to Fed easing typically has no benefit for stocks, aside from a short-lived knee-jerk reaction, unless market internals indicate that investors are inclined toward speculation. The entire total return of the S&P 500 since the 2007 market peak, and also since the 2000 market peak, has occurred during periods when our measures of market internals were uniformly favorable, while nearly all of the market collapses in 2000-2002 and 2007-2009, as well as the market weakness of recent months, occurred when internals were ragged and divergent.

So while Fed easing clearly amplifies speculation when investors are inclined to speculate, it has very little effect in periods when investors are inclined toward risk-aversion. The chart below, from Bubbles and Hot Potatoes, offers a sense of this distinction. Here, I’ve defined “easing” as periods where the most recent move in the Federal Funds rate or the Discount Rate was downward, or where Treasury bill yields decline by at least 0.50% from their high of the previous 6-month period. The opposite criteria are used for tightening. This classifies about 63% of periods as easing, and 37% as tightening. The monetary policy stance is then partitioned based whether the condition of market internals (our proxy for whether investors are inclined toward speculation or risk-aversion) was favorable or unfavorable.

This is one of the key lessons that investors are likely to learn over the completion of this cycle, even though they should already remember that the Fed eased persistently and aggressively throughout the entire 2000-2002 and 2007-2009 market collapses, to no avail. For that reason, it will be important to take our cues directly from market action, not from Federal Reserve actions per se.

Even a shift to Fed easing typically has no benefit for stocks, aside from a short-lived knee-jerk reaction, unless market internals indicate that investors are inclined toward speculation. The entire total return of the S&P 500 since the 2007 market peak, and certainly since the 2000 market peak, has occurred during periods when our measures of market internals were uniformly favorable, while nearly all of the market collapses in 2000-2002 and 2007-2009, as well as the market weakness of recent months, occurred when internals were ragged and divergent.

The gradual retreat of Federal Reserve statements toward an easier policy stance is similar to what we observed in January 2001 and again in January 2008, both at the beginning of what would devolve into severe bear market collapses. Notably, the recent retreat by the Fed was also joined by “two-tiered” market behavior, favoring growth stocks and decidedly disfavoring value stocks. In each case, the failing uniformity of market internals was far more relevant for market prospects than Fed easing itself. My comments from 2001 and 2008 reflect these concerns:

“Enough of their cries of ‘Why have you forsaken us?’ and ‘Lead us out of the wilderness!’ On January 3rd, Alan Greenspan finally descended from the burning bush, holding in his hands two stone tablets. A Fed Funds cut inscribed on one, a Discount Rate cut on the other, together forming a single commandment: ‘Buy Cisco.’

“Investors haven’t learned their lesson. Despite the brutalization of New Economy stocks over the past year, ignorance and greed obey no master. Following the Fed move, investors went straight for the glamour tech stocks, dumping utilities, pharmaceuticals, consumer staples, hospital stocks, insurance stocks – anything that smacked of safety or value. Investors are behaving like an ex-con, whose first impulse after getting out of the joint is to knock over the nearest liquor store.

“In short, the immediate response of investors to interest rate cuts was to create a two-tiered market. And unfortunately, it’s exactly that failing ‘trend uniformity’ that places this advance in danger. Historically, sound market rallies are marked by uniform market action across a wide range of sectors.”

– John P. Hussman, Ph.D., Hussman Investment Research & Insight, January 2001

We observed essentially the same dynamic in January 2008:

“As anticipated, the Fed initiated a large ‘intermeeting cut’ on Tuesday morning, which allowed the stock market to dodge a bullet. Unfortunately, my impression is that the bear is toting a semi-automatic with a full clip of ammo.

“My continued concern is that numerous market plunges have been indifferent to both interest rate trends and even valuations, with the main warning flag being deterioration in the quality of market internals, as we observe at present. Both in the U.S. and internationally, ‘singular events’ tend to occur well after internal market action has turned unfavorable, and prices are well off their highs.

“We’ve been open to a fast clearing rally, which we observed as a 7% surge from intra-day low on Tuesday to intra-day high on Friday, on waning volume. At present, I have no pointed views about short-term direction. Valuations are better than they were a few months ago (though still generally rich), but none of the risks that have concerned me in recent months have diminished.”

– John P. Hussman, Ph.D., Broadening Instability, January 28, 2008

No near-term forecasts, but severe full-cycle concerns

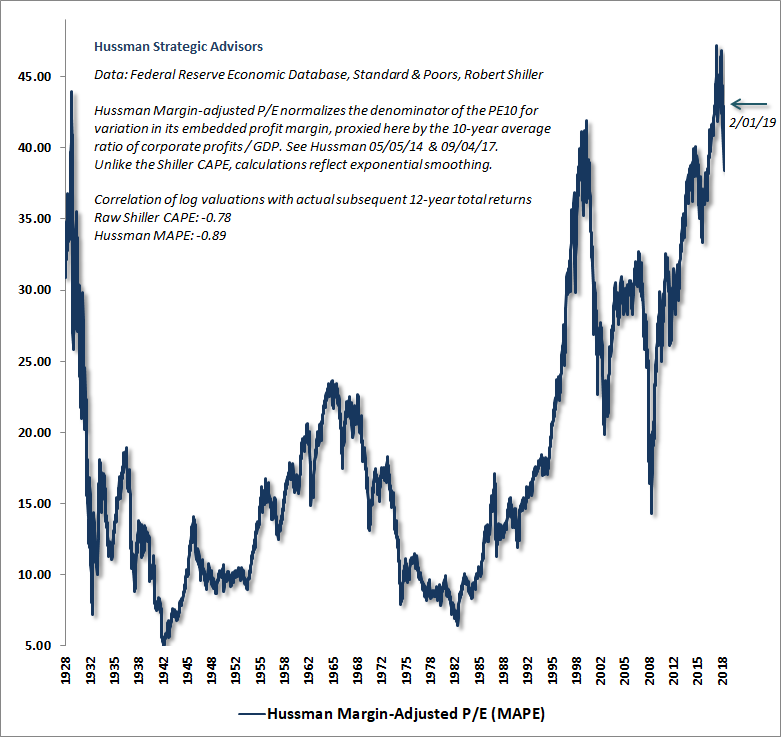

As I noted two weeks ago, the expected “clearing rally” from the December lows has served its function, eliminating the oversold condition of the market, and reviving bullish sentiment among investors. As of Friday, February 1st, the “clearing rally” from the December lows has brought the S&P 500 within 8% of the most extreme point of overvaluation in U.S. history; with valuations that continue to rival the 2000 and 1929 peaks, on the measures that we find best correlated with actual subsequent S&P 500 total returns.

Meanwhile, our measures of market internals remain unfavorable. It’s that combination of extreme valuations and unfavorable market internals that continues to create a potential “trap door” situation for the market, and an environment that’s permissive of steep losses.

As I did in late-December when discussing the prospect of a sharp clearing rally, I use the word “permissive” to emphasize the fact that we are not trying to forecast market outcomes, but are instead attempting to identify conditions in which various outcomes may be more or less likely to occur. That distinction is important.

We always have to allow for potential shifts in market internals, and the combination of a retreating Fed, continued job growth, and the prospect of various “deals” on the budget and trade provides food for “Goldilocks” narratives that might encourage speculators to take that bit in their teeth. As much as I expect the S&P 500 to lose about 50-60% of its value over the completion of this market cycle, most likely over the next couple of years, I have no pointed forecast regarding shorter-term outcomes.

The ‘clearing rally’ from the December lows has brought the S&P 500 within 8% of the most extreme point of overvaluation in U.S. history; with valuations that continue to rival the 2000 and 1929 peaks, on the measures that we find best correlated with actual subsequent S&P 500 total returns. Meanwhile, our measures of market internals remain unfavorable. It’s that combination of extreme valuations and unfavorable market internals that continues to create a potential “trap door” situation for the market, and an environment that’s permissive of steep losses.

The most recent shift in our measures of internals was the deterioration I noted on February 2, 2018, fully a year ago. Shifts in our measures of internals persist about 30 weeks on average, but with a wide range of variation. 25% of shifts have persisted longer than 40 weeks, and about 25% of shifts have persisted 7 weeks or less. A few favorable periods have survived beyond 80 weeks, and a handful have been single-week whipsaws. We view the uniformity and divergence across market internals as an indication of speculative or risk-averse psychology among investors, and we shouldn’t be surprised to see a few periods of speculation even over the course of what’s likely to be a steep and extended bear market decline.

If internals were to improve with valuations as extreme as we currently observe, the most aggressive response I’d expect would be to encourage a constructive outlook with a tight safety net. But the more reasonable valuations become, the more latitude there will be to adopt an aggressively bullish outlook in response to improved internals.

If our measures of market internals were to improve here and now, whatever full-cycle expectation we might have for market losses would be deferred until we were to observe fresh deterioration. As conditions stand, my impression is much as it was in early 2008: “I have no pointed views about short-term direction. Valuations are better than they were a few months ago (though still generally rich), but none of the risks that have concerned me in recent months have diminished.”

If internals were to improve with valuations as extreme as we currently observe, the most aggressive response I’d expect would be to encourage a constructive outlook with a tight safety net. The more reasonable valuations become, the more latitude there will be to adopt an aggressively bullish outlook in response to improved internals.

As for recession risk, my impression is that risks are increasing more than Wall Street generally concedes, but we still don’t observe enough deterioration to conclude that a recession is imminent. My October comment, The Music Fades Out, included a discussion of our Recession Warning Composite.

Presently, our recession concerns would increase greatly if the remaining components of that composite were to shift, including a decline in the ISM Purchasing Managers Index below 50, an increase in the rate of unemployment above 4% (barring another government shutdown that might otherwise bias it higher), and a slowing in the growth rate of nonfarm payrolls below about 1.4% year-over-year.

Once we observe those factors, confirming evidence would include a decline in aggregate hours worked versus 3-months earlier. A steep drop in consumer confidence, particularly about 20 points below its 12-month average, would further raise our expectations of a recession.

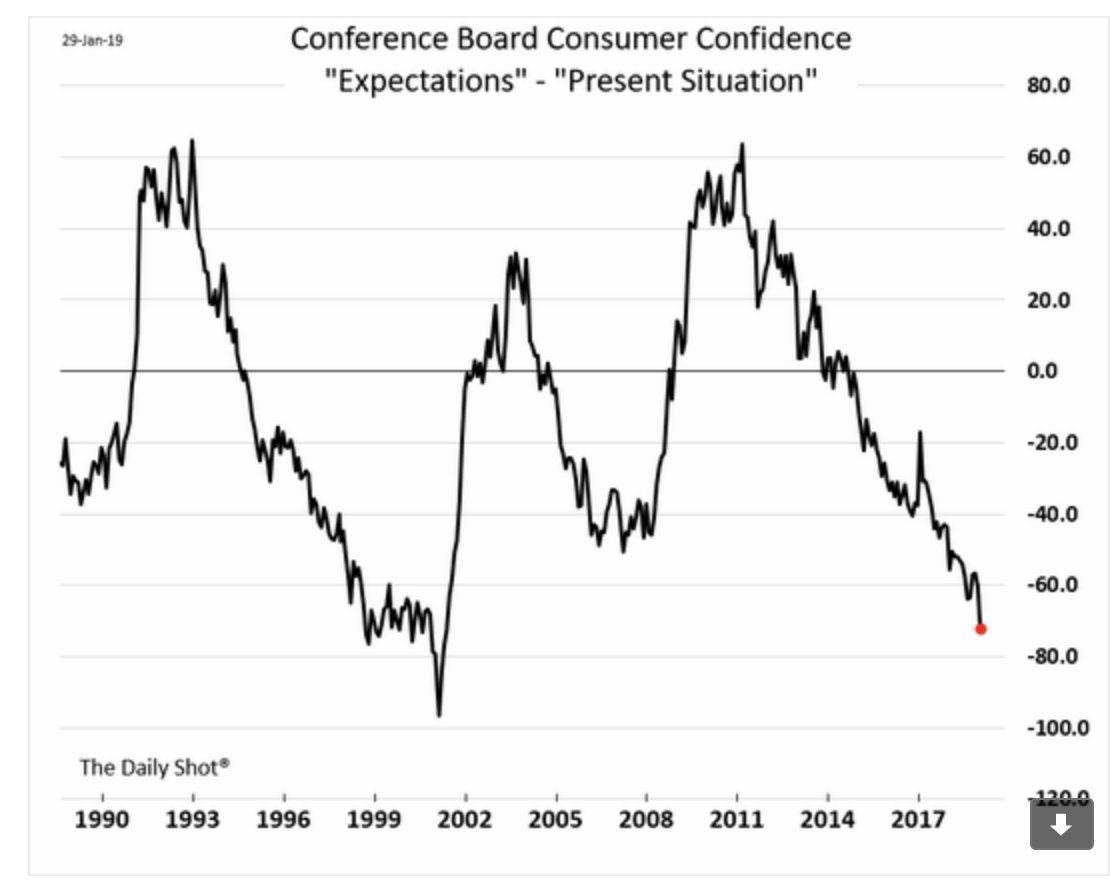

For now, we’re seeing certain inversions that tend to precede economic weakness, but don’t have immediate timing associated with them. For example, as I noted last month, the “future expectations” component of consumer confidence continues to deteriorate relative to the “present situation” component. Other observers have also echoed this concern. This chart is from The Daily Shot.

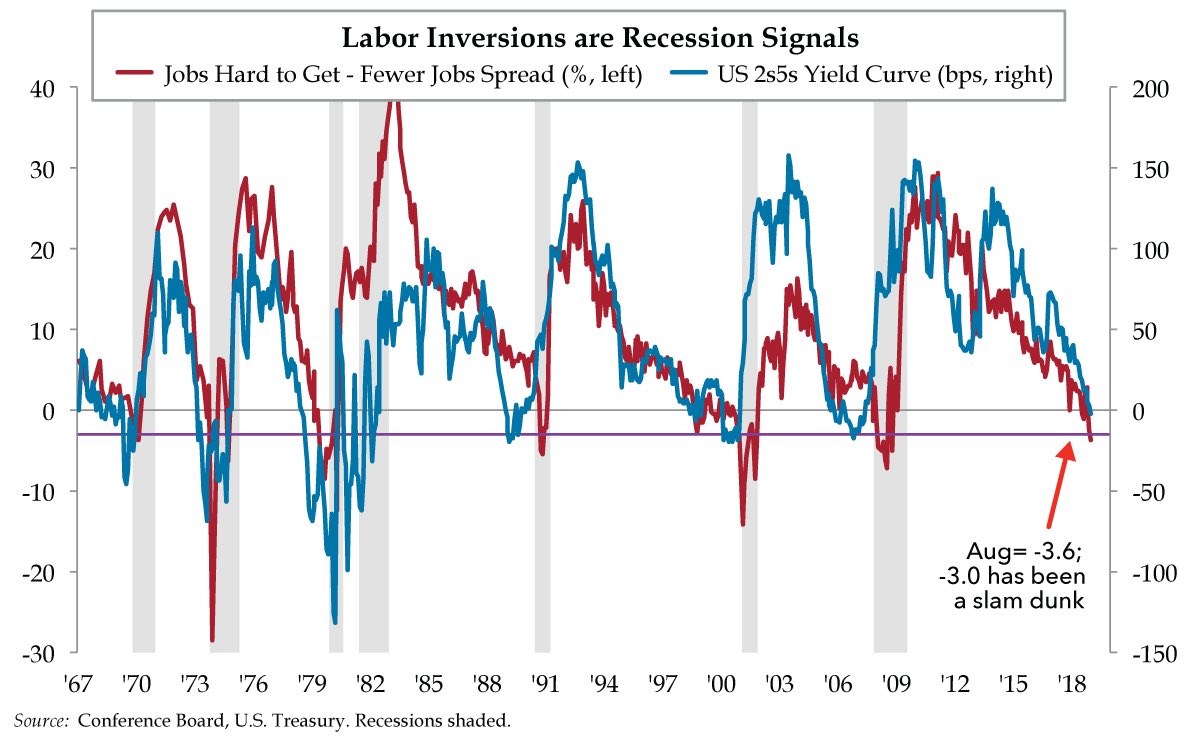

We also observe what my friend Danielle DiMartino Booth calls a “labor market inversion” in the jobs components of the Conference Board measures. Again, my inclination is to wait for more decisive evidence from all components of our Recession Warning Composite, but this remains a very late-stage economic expansion, and it’s appropriate to monitor conditions closely for recession risk.

Our recession concerns would increase greatly if the remaining components of our Recession Warning Composite were to shift, including a decline in the ISM Purchasing Managers Index below 50, an increase in the rate of unemployment above 4% (barring another government shutdown that might otherwise bias it higher), and a slowing in the growth rate of nonfarm payrolls below about 1.4% year-over-year.

Turtles all the way down

A central feature of the recent experience with quantitative easing (QE) is that even as the Federal Reserve bought up Treasury bonds from the public and replaced them with $4 trillion in base money (currency and bank reserves), the swap did not provoke investors to lose confidence in the long-term purchasing power of the dollar. So rather than driving the rate of inflation higher, investors responded by treating the zero-interest base money as a pile of hot potatoes, which each successive holder could disown only by trading it for some risky security. Hence, QE helped to amplify speculation rather than inflation.

Looking at Wall Street’s emerging dialogue, including questions we’ve received about the subject, it’s clear that some market participants and even politicians are beginning to imagine that this kind of behavior can be expected regardless of the quantity of money involved, and regardless of economic conditions. The idea, which runs contrary to centuries of economic evidence, is that any amount of money creation will be passively accepted by investors without a loss of confidence. On that assumption, the argument follows that any amount of economic activity can be generated simply by printing enough pieces of paper.

If you think about how money is valued, it’s clear that people accept it because they believe it will provide a claim on the future output of others. Of course, that expectation requires that future producers will also give away their output and accept the money, on the belief that yet other future producers will do the same. That expectation has to continue indefinitely.

Like the question “What holds up Atlas when Atlas holds up the world?” it’s not enough to answer that he’s standing on a turtle. It’s got to be turtles all the way down. The value of money has an enormous psychological component, and if that psychological confidence breaks, the result is inflation or hyperinflation (particularly when disruptions in the supply of goods are also involved).

This brings us to a notion that’s been increasingly bandied about, called Modern Monetary Theory or MMT. The theory basically asserts that the government is a monopolist in creating currency, and that unemployment is essentially the result of the monopolist choosing to excessively restrict the supply of currency. The corollary is that sufficiently large government deficits, financed by currency creation, can eliminate unemployment. Essentially, MMT proposes that the government has an effectively unlimited ability to spend, with no risk of insolvency, simply by printing more currency.

One might immediately respond that this proposition ignores the potential for inflation, and one would be correct. If that was all there was to the theory, it would sink like a stone. Though some proponents give lip service to the possibility of “resource constraints,” that possibility never actually seems to constrain anything.

To provide an intellectual foundation, MMT is typically described using accounting identities that relate government deficits to money creation. I’ll present these in a (hopefully) simple way below. These identities are nothing more than arithmetic, but they dress the theory up enough that its basic prescription – go ahead and print money to finance endless deficits – seems a bit more dignified.

Like the question ‘What holds up Atlas when Atlas holds up the world?’ it’s not enough to answer that he’s standing on a turtle. It’s got to be turtles all the way down. The value of money has an enormous psychological component, and if that psychological confidence breaks, the result is inflation or hyperinflation.

If you’ve read my own stuff for any length of time, you’re familiar with ideas like the savings-investment identity, and it’s no revelation that government deficits have to be financed either by debt creation or money creation, so fiscal policy is never actually “independent” of monetary policy. But phrased in particular, and slightly misleading ways (like “The only way for the private sector to accumulate a surplus is for the government to run a deficit”), these rather boring accounting identities are used by MMT as tools that promise only benefits from currency-financed deficit spending.

The one-minute exposition begins with the basic accounting equation for national income and output:

GDP = Consumption + Investment + Government Spending + Exports – Imports

which is typically written as:

Y = C + I + G + X – M

Adding and subtracting taxes T and rearranging gives:

(Y – T – C) + (M – X) + (T – G) = I

This is the savings-investment identity, and is always true by definition.

The first term here is “domestic saving,” which is simply the income of U.S. residents after subtracting taxes and consumption (Y – T – C). This figure includes both household and corporate saving.

The second term (M – X) is “foreign saving.” If our imports exceed our exports, it must be that foreigners have produced more than they have consumed, and are sending the difference to us. In other words, they have saved. What do foreigners get in return for the net goods and services they send to us? They get U.S. securities. We have to pay for our imports, so every dollar of goods and services we import has to be paid by exporting something. If we don’t pay by exporting goods and services, then we pay by exporting securities to foreigners instead. So imports minus exports (M – X) measure the net amount of foreign saving required to balance our payments, and the net amount of U.S. securities that foreigners accumulate.

The third term (T – G) is “government saving,” which is currently an oxymoron, but this figure can of course by negative.

The overall equation says that all investment – and here we’re talking about any output of the economy that isn’t consumed, including factories, housing, equipment, inventory, unwanted inventory, and all other unconsumed output – is the result of various sectors of the economy refraining from consuming, that is by “saving.” That’s an identity because either output is consumed or it isn’t. Period.

The proponents of MMT are fond of saying “The only way for the private sector to accumulate a surplus is for the government to run a deficit.” This makes surpluses sound like a very good thing, and therefore makes government deficits sound like a good thing as well.

Examining the savings-investment identity more closely, two things should be immediately apparent. First, government deficits only raise private surpluses if we’re also counting foreigners among those who are accumulating surpluses, and also if we’re holding the amount of gross domestic investment constant. An embedded assumption here is that no amount of government spending can “crowd out” private investment.

Second, and more importantly, what those “surpluses” really represent is output that isn’t consumed by the private sector (though the government presumably uses it for their benefit).

So what kind of “surplus” is actually “accumulating” in private hands when the government runs a deficit? Well, the private sector accumulates government liabilities, either in the form of 1) U.S. government debt like Treasury bonds, or 2) base money, created when the Federal Reserve buys Treasury bonds and pays for them with objects that are spit out from a printing press – just read the top line of those green pieces of paper in your wallet.

What we actually have from the savings-investment identity is a slightly less palatable proposition: “Holding gross domestic investment constant, government deficits must result either in the public accumulating government liabilities or by foreigners accumulating financial claims on the U.S.” You can see why the proponents of MMT don’t use that one.

What kind of ‘surplus’ is actually ‘accumulating’ in private hands when the government runs a deficit? Well, the private sector accumulates government liabilities, either in the form of 1) U.S. government debt like Treasury bonds, or 2) base money, created when the Federal Reserve buys Treasury bonds and pays for them with objects that are spit out from a printing press.

Keynesian economists are fond of arguing that government spending has a “multiplier” effect on output. This argument, like its cousin, the “money multiplier,” mainly relies on the arithmetic of infinite series, rather than any actual considerations of economics. In both cases, the quiet assumption is that there are no constraints on output, resources, productivity, or risk-taking, so that new output immediately appears in response to new demand, and demand immediately increases in response to new income. Turtles all the way down. Having abandoned any concept of scarce resources, this isn’t really economics at all, but the profession feeds it to the youth early enough that they grow up without questioning any of it.

One has to remember that Keynes published the General Theory in 1936 in response to a deflationary depression, three years after the unemployment rate peaked at 25.6%. At that time, the ratio of government debt to GDP was 40%, up from just 16% in 1929. The assumption that output might be very responsive to new demand, without inflation, may very well be attractive in that environment, but is not particularly winsome in an economy with an unemployment rate down to just 4%, with the Federal deficit pushing $1 trillion, and total public debt now over 104% of GDP.

In my view, the current enthusiasm for MMT is an artifact of a long disinflationary period since the 1980’s, during which the U.S. has financed increasingly large deficits by issuing liabilities, while the U.S. public and global investors have accumulated them without a major loss of confidence in their value. The recent experience with QE has hardened the belief that the appetite of the public for these liabilities is infinite.

The proponents of MMT are fond of saying ‘The only way for the private sector to accumulate a surplus is for the government to run a deficit.’ This makes surpluses sound like a very good thing, and therefore makes government deficits sound like a good thing as well. What we actually have from the savings-investment identity is a slightly less palatable proposition: ‘Holding gross domestic investment constant, government deficits must result either in the public accumulating government liabilities or by foreigners accumulating financial claims on the U.S.’ You can see why the proponents of MMT don’t use that one.

The problem here is that public perceptions about inflation are almost always conditioned by the recent behavior of inflation itself. High recent inflation reinforces the belief that inflation will be permanent. Low recent inflation reinforces the belief that infinite amounts of money can be created with no risk. Both situations reflect a basic fact about inflation: the most reliable predictor of inflation isn’t money growth, or output growth, or government deficits, or the rate of unemployment, but rather the rate of inflation itself.

Again, inflation has an enormous psychological component: it reflects a loss of confidence that the liabilities issued by the government will retain their ability to purchase the same amount of real goods and services that they can purchase today. The key uncertainty about inflation is that it is largely a psychological event, and depends heavily on the confidence, or loss of confidence, by the public that government liabilities (bonds and base money) can be held without deterioration in their value.

In the 1960’s, the U.S. relied on that sort of confidence when it was under the gold standard, yet ran increasing government deficits that were essentially funded on the expectation that U.S. investors and foreign governments would simply accumulate them indefinitely. The French criticized this behavior as an “exorbitant privilege,” resulting from the position of the U.S. dollar as the benchmark currency for international transactions (which was established by the Bretton Woods agreement in 1944).

By the 1970’s, the psychological confidence of the public in the dollar was shocked by two events that disrupted expectations for price stability. First, foreign governments became intolerant of accumulating dollars, and demanded to convert them into gold. In 1971, Nixon had to close the gold window, ending the de-facto gold standard that had supported stable exchange rates. Shortly thereafter, inflation exploded, and it was later amplified by supply shocks resulting from the OPEC oil embargo.

It’s not clear whether we’ll see a similar loss of public confidence about price stability in the years ahead, but I’m not at all optimistic about the idea that government debt and money creation can expand indefinitely without consequences. Just as we use the uniformity of market internals to gauge the psychological inclination of investors toward speculation versus risk-aversion, our own focus will remain on the uniformity of inflation-sensitive assets (precious metals, oil, commodities, real assets, bond prices, inflation-protected securities, and so forth) to gauge psychological shifts regarding inflation.

One has to remember that Keynes published the General Theory in 1936 in response to a deflationary depression, three years after the unemployment rate peaked at 25.6%. At that time, the ratio of government debt to GDP was 40%, up from just 16% in 1929. The assumption that output might be very responsive to new demand, without inflation, may very well be attractive in that environment, but is not particularly winsome in an economy with an unemployment rate down to just 4%, with the Federal deficit pushing $1 trillion, and total public debt now over 104% of GDP.

In the meantime, what’s the best way to think about the benefits and risks of government debt and deficits? The central thing, I think, is to avoid discussing any of it without also thinking carefully about what the money is being used for. If the government has the opportunity to start a project involving infrastructure or renewable energy that isn’t possible for the private sector to coordinate, and has a very high likelihood of throwing off 10% annual benefits to the economy, indefinitely, it may be a very good idea to run a deficit and issue debt to finance that project. The same is true even for social initiatives with indirect benefits that might be measured in public well-being rather than cash.

But spend poorly, and the overall capacity of the economy will fail to grow in tandem with the debt burden. What’s often forgotten is that once debt or money is created, it remains outstanding until it is retired, or until an oversupply finally provokes a loss of confidence that we observe as inflation or plunging bond prices. It’s that fact that makes me unsympathetic to this paragraph from Chapter 10 of Keynes’ General Theory, except in the midst of a Depression:

“If the Treasury were to fill old bottles with banknotes, bury them at suitable depths in disused coalmines which are then filled up to the surface with town rubbish, and leave it to private enterprise on well-tried principles of laissez-faire to dig the notes up again (the right to do so being obtained, of course, by tendering for leases of the note-bearing territory), there need be no more unemployment and, with the help of the repercussions, the real income of the community, and its capital wealth also, would probably become a good deal greater than it actually is. It would, indeed, be more sensible to build houses and the like; but if there are political and practical difficulties in the way of this, the above would be better than nothing.”

That paragraph is the essence of MMT. It carries with it no particular requirement for the government to spend in a way that leads to durable expansion in economic activity, sufficient to ensure that the new liabilities can be carried indefinitely without an ultimate collapse in their value. The failure to seriously consider and embed those issues as central elements of the theory is what makes MMT (and lots of other models) little more than arithmetic, rather than economics.

Put simply, debt and deficits can only be judged as beneficial or detrimental to the extent that we know how the funds are being used, and the extent we believe that the direct and indirect benefits to society are enough to repay or at least permanently carry the resulting liabilities.

One of the first things you’ll hear in an undergraduate economics class is that “Economics is the study of how scarce resources are allocated.” Then, without any sense of irony, most professors will launch into Keynesian theory, money multipliers, and other models that effectively assume no scarcity or resource constraints whatsoever.

In my view, real, thoughtful economic analysis asks questions like “What are the resources”, “What are the constraints, and where are they binding”, “Where are the barriers, distortions, or coordination failures?”, “What are the externalities”, “Who bears the costs ?”, “What relationships are actually true in the data?”, “What are the incentives and how will this policy change them?”, “What are the unintended consequences?”, and “What are the most productive uses?”

The standard of living of any nation, after all, is measured by the amount of goods, services, and intangible well-being that individuals in that nation can enjoy. The productivity of any nation is measured by the amount of goods, services, and intangible well-being that individuals in that nation can produce. I’d absolutely define both of these broadly, so that individual well-being is given adequate weight in assessing our collective prosperity, and I’d also include non-monetary factors like environmental sustainability. However we might account for all of that, our long-term standard of living is always dependent on how we channel our resources to nourish our long-term productivity. So many discussions of economics completely miss that point. In my view, it’s ultimately the point of economics that matters most.

Keep Me Informed

Please enter your email address to be notified of new content, including market commentary and special updates.

Thank you for your interest in the Hussman Funds.

100% Spam-free. No list sharing. No solicitations. Opt-out anytime with one click.

By submitting this form, you consent to receive news and commentary, at no cost, from Hussman Strategic Advisors, News & Commentary, Cincinnati OH, 45246. https://www.hussmanfunds.com. You can revoke your consent to receive emails at any time by clicking the unsubscribe link at the bottom of every email. Emails are serviced by Constant Contact.

The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse.

Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking “The Funds” menu button from any page of this website.

Estimates of prospective return and risk for equities, bonds, and other financial markets are forward-looking statements based the analysis and reasonable beliefs of Hussman Strategic Advisors. They are not a guarantee of future performance, and are not indicative of the prospective returns of any of the Hussman Funds. Actual returns may differ substantially from the estimates provided. Estimates of prospective long-term returns for the S&P 500 reflect our standard valuation methodology, focusing on the relationship between current market prices and earnings, dividends and other fundamentals, adjusted for variability over the economic cycle.