|

|

||||||

|

|

January 14, 2008 Past, Present and Future Just a performance note that was posted to the website on Friday : The 0.22 NAV decline in the Strategic Growth Fund on Friday, January 11 was largely attributable to unusual dispersion between our broadly diversified (but not capitalization weighted) stock holdings and the indices we use to hedge. In particular, the technology and retail sectors declined by 2-3%, while the cap- weighted indices we use to hedge declined by a smaller amount. --- As I discussed in last week's market comment: "the growing internal turbulence of the market has recently created opportunities to populate our stock holdings with what I view as reasonable and even favorable absolute valuations. You can observe this dispersion in the fact that equal-weighted market indices have been declining more sharply than the capitalization-weighted indices. This can produce a bit of short-term discomfort because we do use those cap-weighted indices to hedge, but I see it as a very good development in terms of intermediate and long-term prospects for investment returns." My impression is that Wall Street's initial response to recession concerns is to do "trading by caricature" - looking at past bear markets, sorting by which industry groups did best and worst on average, and responding without further analysis. This is why you hear so many analysts parroting their fresh affection for healthcare and consumer staples. The problem with these caricatures is that the bear market performance of various sectors is significantly affected by initial valuations, and presently, technology and consumer discretionary (e.g. retail) stocks reflect among the best valuations in the market. It may seem counterintuitive, but the sort of "blunt" selling we observed last week is generally a favorable development. It allows value-conscious investors to establish positions as stocks are sold indiscriminately, after which the market often sorts the wheat from the chaff more carefully. Including reinvested distributions, the Strategic Growth Fund is less than 5% below its record high. We will almost certainly experience some "local" volatility of a few percent in both directions, because this phase probably is not over. But while it's easy to develop a performance gap of a few percent between a well diversified portfolio of stocks and the capitalization weighted indices, these should not be extrapolated as if something is wrong. The Fund is fully hedged, and I believe well hedged, but some amount of basis fluctuation between our stocks and the general market should be expected. The willingness to accept a controlled amount of "basis risk" has been precisely the source of the Fund's returns since inception. The closer our holdings reflect the indices we use to hedge, the smaller our day-to-day volatility is, but the closer our returns resemble Treasury bills. As the market develops greater divergences between the valuations of various industry groups, we can accept more basis risk on the expectation of higher returns. It will be helpful for shareholders to recognize that this will involve some fluctuations, but that we are well hedged against major market trouble. My efforts are directed at lessening the periodic discomfort without missing opportunities that I expect to contribute to strong subsequent returns. For the record, we didn't get a whole lot of traction in the early part of the 2000-2002 bear market either (green is HSGFX, red is the S&P 500 total return). Then, as now, we did not carry net short positions - the dollar value of our shorts never materially exceeds our long holdings

The chart below provides a good idea of the internal weakness of the broad market lately. Note that both charts track the 500 stocks in the S&P 500 Index, with the only difference being that the blue line is the standard, cap-weighted index, while the red line weights all of the component stocks equally. These are the same stocks in each index, so even an equally-weighted position in the S&P 500 stocks, hedged with the S&P 500 index, would be down about 5% in recent months. Evidently, the typical stock is experiencing heavier liquidation than is evident in the popular averages. Generally speaking, market internals often deteriorate prior to major losses in the widely followed indices.

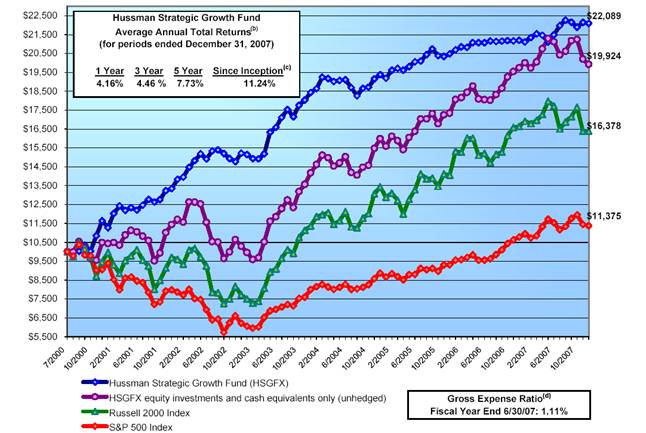

Past, Present and Future As we enter 2008, I thought it would be a good time for a thorough discussion of Fund performance and considerations for the period ahead. The only way to adequately begin is with the recognition that the returns in the Strategic Growth Fund have been far below my long-term expectations in the 4 years since early 2004, and particularly in the period of just over 2 years since early 2006. Our investment strategy has strongly outperformed the S&P 500 over the complete bull-bear market cycle, with substantially smaller periodic losses, and I believe that it is well-suited to achieve those objectives in the years ahead. That said, the past few years of single-digit returns have been an obvious disappointment. The following is a small version of our regular performance chart. The blue line is the Strategic Growth Fund. The purple line below it represents the "stocks only" performance of the Fund's holdings, excluding the impact of hedging transactions. The green line below that tracks the total return of the Russell 2000 index, and the bottom line in red is the total return of the S&P 500 Index.

Since 12/31/03, the S&P 500 itself has only beat Treasury bills by about 4% annually (which is a very slim margin for a bull market period). That gap of about 4% represents the foregone returns that have resulted from hedging the Fund's holdings against market fluctuations since then. The S&P 500 would have to decline by a bit less than 14%, holding the Fund unchanged, for the Fund's total return to match that of the S&P 500 since the end of 2003. That said, our primary disappointment in recent years has not been hedging or overall investment strategy. For us, the difficulty has been in gaining enough traction from our stock selection to significantly outperform the indices we use to hedge, mostly during the past two years. The returns of the S&P 500 in recent years have been disproportionately attributable to energy, basic materials, capital goods, and other companies with poor stability in earnings and balance sheets. We've held some of these (particularly oil companies), but due to the unpredictability of their long-term cash flows, their valuations have a large speculative and commodity-driven component. Despite the excitement about growth from China and other "BRIC" countries, I've been averse to placing a large portion of shareholder assets at risk in companies that strike me as cyclical and commodity plays. I don't understand, for example, how investors believe that fertilizer stocks are worth 50-60 times their already elevated earnings. But that also means that I've missed the boat on these and similar stocks. The Past From the Fund's inception in 2000 through the end of 2003, the Fund's stock selections outperformed the S&P 500 by over 10% (i.e. 1000 basis points) annually. I don't view that period as particularly unusual - I've built my reputation as an investment advisor since 1985 primarily on stock selection, and those returns were not at odds with that experience or with long-term historical research. Moreover, the dollar value of our shorts never materially exceeds our long holdings which reduces the risk that our hedging strategy will generate predictable losses even in an overvalued bubble - something that admittedly bedeviled us in the late 1990's as the market advanced toward its peak. So from my standpoint, the period from 2000-2003 represented the faithful application of our investment discipline, and what I viewed as reasonable returns, consistent with historical evidence. For that reason, I described the Fund's performance at the time as "neither extraordinary nor disappointing" and generally began the annual and semi-annual reports with a note that the Fund had performed as intended. I did note that we could expect to experience greater volatility at the point where a larger (unhedged) exposure to stocks became appropriate, and also that we would accept that volatility only where it appeared likely to be compensated over time. In 2004-2005, even though I could easily purchase the stocks that I viewed as attractive without any major price impact (which is still the case), our stock selection performance margin slipped to 2-4% in excess of the S&P 500. If you've been reading these comments for any length of time, you know that this is when I began expressing frustration over low-quality cyclicals and "garbage stocks" that were driving much of the market's returns. Still, our margin of outperformance was enough to produce further gains, and the Fund outperformed the S&P 500 even in the "bull market" year of 2005. By contrast, during the past two years, the Fund's stock holdings have lagged the S&P 500 by about 3% annually, which has held the returns of our hedged position to still-positive but low single digits. The Present So where do we stand? From the beginning of 2004 through last Friday (1/11/08), the Strategic Growth Fund achieved a total return of 16.78% (3.92% annually), versus a total return of 35.67% (7.86% annually) for the S&P 500. From the beginning of 2006 through last Friday, the Strategic Growth Fund achieved a total return of 5.05% (2.45% annually) versus 16.64% (7.86% annually) for the S&P 500. Presently, the S&P 500 would have to decline by just under 14%, with the Fund unchanged, to align our returns with those of the S&P since 12/31/03 (1.1678/1.3567 - 1 = -0.1392). While I continue to expect the Fund to achieve its objective of outperforming the S&P 500 over the complete market cycle, with smaller periodic pullbacks than the index, the Fund's returns over the past few years are a disappointing fraction of my long-term expectations. Just as frustrating as these tepid returns is the knowledge that I've executed our investment strategy faithfully day after day to achieve that result. Most everything I own is invested in the Strategic Growth Fund (the remainder is in Strategic Total Return), so it should be self-evident that I have confidence in the Fund's invesment strategy as an effective means to achieve our investment objectives. The Future Many investors believe that the best response to a disappointing period of returns is to abandon their investment strategy. I've never seen an investor who has done that repeatedly with success. We are always engaged in research that might improve on our existing approach, but the recent stretch of flattish returns is simply not one that we are inclined to "fix" by embracing stocks with poor earnings stability, rich valuations, unsustainable profit margins, and debt-ridden balance sheets. We continue to avoid these, in the belief that they do not represent reliable investment value. As unsatisfying as this may sound, I believe the best way to significantly outperform the S&P 500 over the complete market cycle, with controlled risk and smaller periodic losses than the index, is to continue adhering to our investment discipline. As discussed above, we're beginning to observe an increased dispersion in the valuations of individual stocks, which has generally provided good stock selection opportunities. By necessity, building an equity portfolio that diverges in certain ways from the indices we use to hedge carries some risk that our stocks will lag the index, but that is the only way we have the potential to outperform it, and that in turn, has been the primary basis for our long-term returns. Meanwhile, since I am not willing to invest a major portion of shareholder assets in materials, industrial cyclicals and commodity plays, true believers in these sectors will be best served making those investments elsewhere. With a few exceptions (which we are willing to hold), many of the stocks in these sectors that can be valued on the basis of probable future cash flows appear significantly overvalued because of an optimistic view that the world economy is somehow "decoupled" from the United States. Others are simply impossible to value without forming pointed expectations about the future long-term path of oil, nickel, potash and other commodity prices. We have had good success trading precious metals shares over the years, but because large share transactions can have a significant price impact, these are largely confined to the Strategic Total Return Fund. If we were interested in serving speculators instead of long-term shareholders, I suppose that we could start a "Bandwagon Fund" to invest in the industrial cyclicals and overvalued momentum stocks that we stubbornly refuse to buy for shareholders who value financial stability. Unfortunately, it's evident that such a fund would be competing in a crowded field. It's doubtful that the long-term returns would be acceptable either, since momentum strategies tend to perform well until they experience excruciating losses. Sadly, investors seeking that sort of speculative vehicle will need to look elsewhere. To some extent, the exuberance about basic materials, fertilizer and the like is reminiscent of the dot-com boom. At that time, it was very clear that the internet itself would grow very rapidly. The problem was that investors equated growth in that industry with expected growth of profits for every company participating in it. But unless there is something particularly special and defensible about a company's products, growth in an industry generally also implies the emergence of competitors and the flattening of profit margins. The same, I think, is likely to be true for companies now embraced by investors because of recent demand from industrializing BRIC countries. Moreover, a century of economic experience suggests that major countries intertwined by trade do not "decouple." My impression is that in the coming quarters, the word "decoupling" will be increasingly replaced by the phrase "synchronous global recession." On the positive side, the Strategic Growth Fund has achieved positive returns in every year since its inception in 2000. The deepest pullback in Fund value has been less than 7%, despite a maximum loss in the S&P 500 approaching 50% during the 2000-2002 bear market. Including reinvested distributions, the Fund is currently less than 5% from an all-time high. Our stock selections have strongly outperformed the S&P 500 over time, and the Fund has more than doubled since inception versus a single-digit (less than 1% annual) total return on the S&P 500. We were correct about the collapse of the tech and internet bubbles and the extent of the probable losses. Our measures that recently warned of recession are the same ones that correctly identified the oncoming recession in late 2000. We've been correct about the likelihood of tepid bull market returns in the current cycle, about the risks to financials, about rising mortgage defaults, about probable weakness in the U.S. dollar, and have managed our bond and precious metals positions very effectively over the years. Still, the overvalued, overbought, overbullish conditions of 2006 through mid-2007 led us to maintain a hedged position that missed, in hindsight, some potential returns (though as of Friday, the S&P 500 has achieved a total return of just 0.73% since the end of 2006, while the Russell 2000 has lost -9.42%). I also recognize that my refusal to invest in stocks having poor stability in earnings and balance sheets has left shareholders starved for returns in recent years. In any event, it is not useful to ascribe too much meaning or importance to minor day-to-day fluctuations. A one-day mismatch of 1% between the performance of our stocks and the indices we use to hedge will currently move the Fund's NAV by 15 cents in one direction or another. This is unusual, but certainly happens from time-to-time in volatile markets with turbulent internals. From my perspective, the only proper way to serve shareholders well is to adhere to our investment discipline, improve it where possible, and to communicate openly about both our successes and our periodic disappointments. As always, our objective is to significantly outperform the S&P 500 over the complete market cycle, with smaller periodic losses than the general market. The objective isn't to outperform Treasury bills every year, nor is it specifically to outperform the S&P 500 over shorter periods. I believe that our investment approach is very well suited to achieving our objectives, but I also recognize that some shareholders are anxious for returns. I wish I could assure immediate rewards for your patience. Though I believe the Fund is well-positioned here, it's not possible to assure investment performance. What I can assure is that I will take those actions that I have a well-tested basis to expect will be rewarding, and to avoid, hedge, or diversify away those risks that I have a well-tested basis to expect will be unrewarding. Market Climate As of last week, the Market Climate for stocks was characterized by unfavorable valuations and unfavorable market action. Frankly, I am surprised that the market's compressed oversold condition has not resulted in a material "clearing rally." Typically, when the vast majority of stocks are trading at the lows of their recent range, the market clears this with an advance averaging several percent over the following 4-6 sessions. The heaviness of the market's action, coupled with increasing volatility at 10-minute increments, continues to suggest significant risk. My impression is that a further decline of several percent from here would increase the probability a sharp clearing rally enough to warrant covering part of the short-call side of our hedges (leaving the put options in place to defend against further weakness), while a strong clearing rally from here would be a good point to raise our put option strikes and establish a stronger "staggered strike" defense against subsequent weakness. In any event, I expect that we'll have a variety of opportunities to modify our hedges in response to market action, while maintaining a generally defensive position until valuations or market action improve sufficiently. In bonds, the Market Climate last week was characterized by unfavorable yield levels and moderately favorable yield trends. The Strategic Total Return Fund continues to carry a duration of about 2 years, mostly in TIPS, with just over 20% of assets invested in precious metals shares, for which the Market Climate continues to be very favorable on our measures. That said, precious metals shares are volatile enough that I reserve positions much beyond 25% of assets for periods when these shares are also significantly oversold. As a result, I would expect to periodically clip our exposure to this sector on further strength, not because of negative expectations for the sector, but simply to keep our risk well managed. -- Disclosures Average annual returns for the Strategic Growth Fund for periods ended 12/31/07: 1 year 4.16%, 3-year 4.46%, 5 year 7.73%, since inception on July 24, 2000 11.24%. Past performance does not ensure future results, and there is no assurance that the Fund will achieve its investment objectives. An investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted above. More current performance data through the most recent month-end, as well as special reports and analysis, are available at the Fund's website www.hussmanfunds.com . The Fund has the ability to vary its exposure to market fluctuations depending on overall market conditions, and may not track movements in the overall stock market, particularly over the short-term. The Fund has the ability to hedge market risk by selling short major market indices in an amount up to, but not exceeding, the value of its stock holdings. The Fund also has the ability to leverage the amount of stock it controls to as much as 1 1/2 times the value of net assets, by investing a limited percentage of assets in call options. While the intent of this strategy is long-term capital appreciation and protection of capital, the investment return and principal value of the Fund may fluctuate or deviate from overall market returns to a greater degree than other funds that do not employ these strategies. For example, if the Fund has taken a defensive posture and the market advances, the return to investors will be lower than if the Fund had not been defensive. Alternatively, if the Fund has taken an aggressive posture, a market decline will magnify the Fund's investment losses. Investors should consider the investment objectives, risks, and charges and expenses of the Fund carefully before investing. For this and other information, please obtain a Prospectus and read it carefully before investing. A copy of the Prospectus may be obtained at www.hussmanfunds.com or by calling 1-800-487-7626. The Distributor of the Hussman Funds is Ultimus Fund Distributors, LLC., 225 Pictoria Drive, Suite 450, Cincinnati, OH, 45246. (a)The Hussman Strategic Growth Fund invests in stocks listed on the New York, American, and NASDAQ exchanges, and does not specifically restrict its holdings to a particular market capitalization. The S&P 500 and Russell 2000 are indices of large and small capitalization stocks, respectively. "HSGFX equity investments and cash equivalents only (unhedged)" reflects the performance of the Fund's stock investments and modest day-to-day cash balances, after fees and expenses, but excluding the impact of hedging transactions. The Fund's unhedged equity investments do not represent a separately available portfolio, and their peformance is presented solely for purposes of comparison and performance attribution. (b)Returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. (c)Annualized. Initial public offering of shares was July 24, 2000. (d)The Fund's expense ratio is through its most recent fiscal year (June 30, 2007). --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |