|

|

||||||

|

|

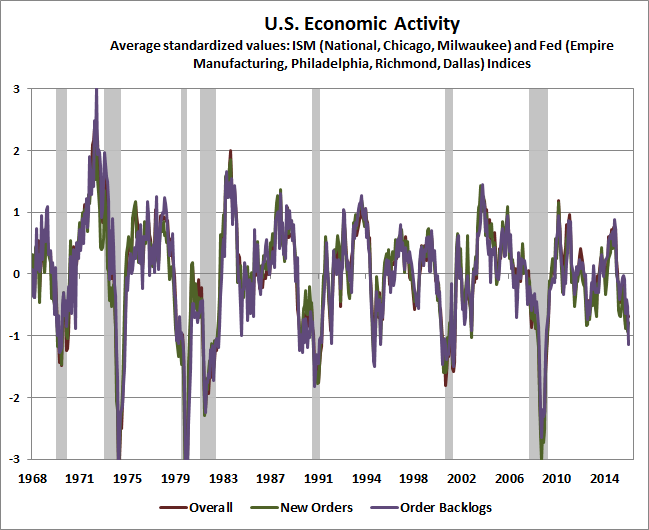

January 11, 2016 Complex Systems, Feedback Loops, and the Bubble-Crash Cycle Our expectations for a global economic downturn, including a U.S. recession, have hardened considerably in the past few weeks, with a continued expectation of a retreat in equity prices on the order of 40-55% over the completion of the current cycle as a base case. The immediacy of both concerns would be significantly reduced if we were to observe a shift to uniformly favorable market internals. Last week, market conditions moved further away from that supportive possibility. As I’ve regularly emphasized since mid-2014, market internals are the hinge between an overvalued market that tends to continue higher from an overvalued market that collapses; the hinge between Fed easing that supports the market and Fed easing that does nothing to stem a market plunge; and the hinge between weak leading economic data that subsequently recovers and weak leading economic data that devolves into a recession. We continue to observe deterioration in what I call the “order surplus” (new orders + order backlogs - inventories) that typically leads economic activity. Indeed, across a variety of national and regional economic surveys, as well as international data, order backlogs have dried up while inventories have expanded. Understand that recessions are not primarily driven by weakness in consumer spending. Year-over-year real personal consumption has only declined in the worst recessions, and year-over-year nominal consumption only declined in 2009, 1938 and 1932. Rather, what collapses in a recession is the inventory component of gross private investment, and as a result of scale-backs in production, real GDP falls relative to real final sales. Emphatically, recessions are primarily points where the mix of goods and services demanded by the economy becomes misaligned with the mix of goods and services being produced. As consumer preferences shift, technology introduces new products that dominate old ones, or market signals are distorted by policy, the effects always take time to be observed and fully appreciated by all economic participants. Mismatches between demand and production build in the interim, and at the extreme, new industries can entirely replace the need for old ones. Recessions represent the adjustment to those mismatches. Push reasonable adjustments off with policy distortions (like easy credit) for too long, and the underlying mismatches become larger and ultimately more damaging. A few charts will bring the economic picture up-to-date. The first is our familiar composite of regional and national Fed and purchasing managers’ surveys. We also maintain a broad composite of dozens of other leading economic variables, which shows the same pattern of retreat. Keep in mind that employment figures (initial claims for unemployment, non-farm payrolls, the unemployment rate, and the duration of unemployment, in that order) are the most lagging economic series available, and typically turn well after the economy does.

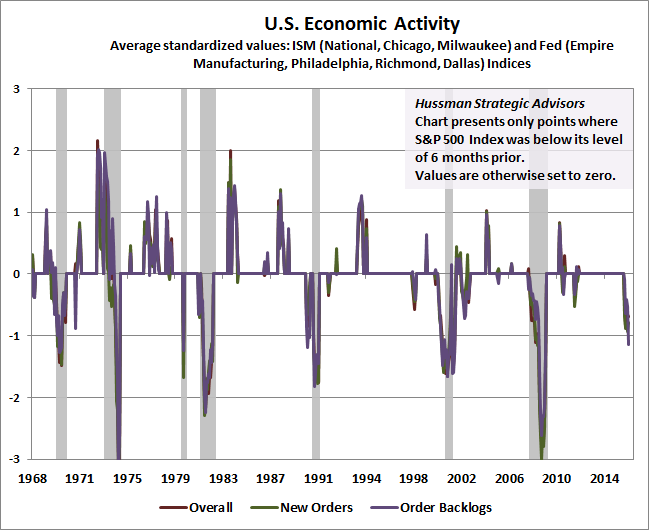

While a weak equity market, in and of itself, is not tightly correlated with subsequent economic weakness, equity market weakness combined with weak leading economic data is associated with an enormous jump in the probability of an economic recession. See in particular From Risk to Guarded Expectation of Recession, and When Market Trends Break, Even Borderline Data is Recessionary. The chart below presents the same data as the one above, except that it shows only values corresponding to periods where the S&P 500 was below its level of 6-months prior (as it is at present). Other values are set to zero. Again, while a uniform improvement in market internals would relieve the immediacy of our present economic and market concerns, we already observe deterioration in leading economic measures that - coupled with financial market behavior - has always been associated with U.S. recessions.

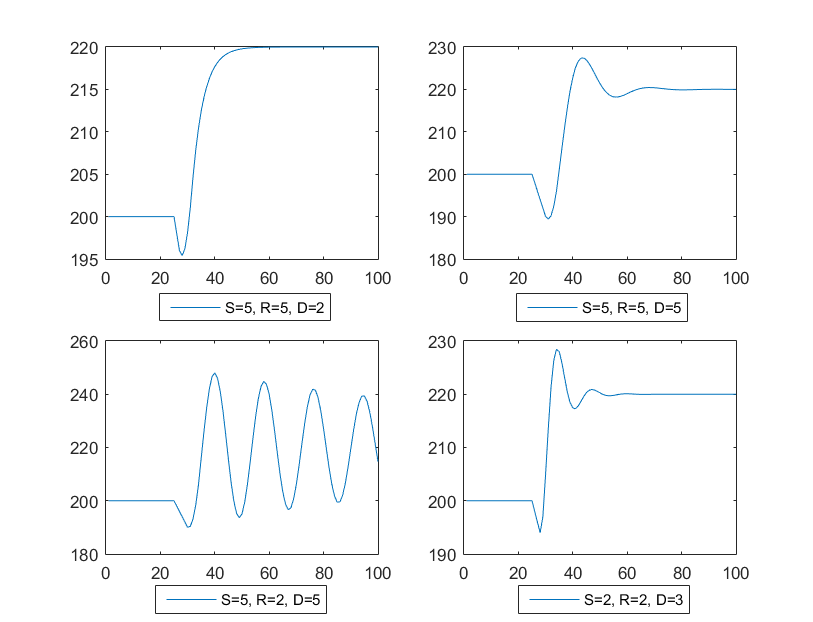

The immediate conclusion that one might draw is that the Federal Reserve made a “policy mistake” by raising interest rates in December. But that would far understate the actual damage contributed by the Fed. No, the real policy mistake was to provoke years of yield-seeking speculation through Ben Bernanke’s deranged policy of quantitative easing, which propagated like a virus to central banks across the globe. The extreme and extended nature of the recent speculative episode means that we do not simply have to worry about a run-of-the-mill recession or an ordinary bear market. We instead have to be concerned about the potential for another global financial crisis, born of years of capital misallocation and expansion of low-quality debt both here in the U.S. and in the emerging economies. For a review of these concerns, see The Next Big Short: The Third Crest of a Rolling Tsunami. Complex systems and feedback loops In any complex system, there are typically two types of feedback loops at work. Some feedback loops are balancing, so that deviations from some desired target are followed by actions to push the system back to that target. Your body has lots of these, which keep your temperature, blood sugar, and other vital processes in check. Other feedback loops are self-reinforcing, so that deviations from some starting point are followed by changes that push the system even further from that point. Cancer and viral replication are among those self-reinforcing feedback loops, and can be fatal if left unchecked by a balancing loop. Any system that rewards the winner of one competition with the means to win the next competition also contains a self-reinforcing feedback loop. Many internet and social media companies benefit from this dynamic, because new users tend to gravitate toward the platforms chosen by existing users. Even if these companies operate with little profit, speculative financial markets may provide them with a war chest of cash through overvalued public offerings, which can then be used to acquire other businesses. The U.S. income distribution has featured a similar feedback loop in recent decades because repeated cycles of capital misallocation have resulted in a scarcity of productive investment. The irony is that as productive capital becomes scarce, the pie becomes smaller, but a larger share goes to the owners of existing capital. Fed policymakers then respond to economic weakness with actions that amplify the misallocation of capital. Instead of continuing these monetary distortions, the best way to improve the distribution of income in the U.S. would be to encourage productive investment at every level - government (productive infrastructure, clean energy), industry (investment and R&D incentives), and individuals (education, job training). This would contribute both to a larger pie and a more equitable income distribution. Most complex systems contain both balancing and self-reinforcing feedback loops, and the behavior of the overall system can change dramatically depending on which loop becomes dominant at any point in time. As the late ecologist and systems analyst Donella Meadows (the author of Limits to Growth and Thinking in Systems) wrote: “The world often surprises our linear-thinking minds. If we’ve learned that a small push produces a small response, we think that twice as big a push will produce twice as big a response. But in a nonlinear system, twice the push could produce one-sixth the response, or the response squared, or no response at all... Nonlinearities are important because they confound our expectations about the relationship between action and response. They are even more important because they change the relative strengths of the feedback loops. They can flip the system from one mode of behavior to another... the sudden swing between exponential growth caused by a dominant reinforcing loop, say, and then decline caused by a suddenly dominant balancing loop.” Meadows observed that "systems largely cause their own behavior," and described how systems that combine even the simplest combination of balancing loops, self-reinforcing loops, or delays can generate strikingly complex dynamics. As an example, consider an auto dealership that targets its level of inventory based on its average sales over the past S days, responds to differences between desired and actual inventory by spreading the required orders over R days, and receives delivery of new cars D days after each factory order is placed. On day 25, there is a one-time shift in auto sales from 20 cars daily to 25 cars daily. That's the only shock to the system. The charts below (generated in Matlab) show how the car dealership’s inventories change in response to that one-time shock, based on how slowly or quickly the dealer smooths perceived sales, responds to inventory shortfalls, and receives deliveries from the factory.

Though Meadows applied systems theory primarily to ecology, social policy, and environmental sustainability, systems theory has similar implications for economics and the financial markets. Notice, in particular, the impact of the delivery delay D. Anytime new actions are taken more quickly than the consequences of one’s previous actions are fully taken into account, a complex system becomes prone to disruptive oscillations. As long as those consequences are slow to arrive, speeding up the response to new data doesn’t help, but instead actually increases the severity of the swings. [Geek’s note: mathematically, the differential equation will contain negative and complex eigenvalues]. From a systems perspective, my objection to activist central bank policy is that the Fed is targeting economic outcomes (employment, inflation) that are only weakly related to its policy tools, and yet those same policy tools can powerfully distort financial markets and international capital flows (provided that investors are inclined toward yield-seeking speculation). The Fed’s failure to recognize the gross disruptions it creates in the financial markets by encouraging yield-seeking speculation and enabling low-quality credit issuance is much like imposing a huge "delivery delay" D on the economic system. The Fed repeatedly fails to consider the full consequences of its actions even though they are baked in the cake, so they only feed into changes in policy once the financial system is in crisis and the Fed's target economic variables - employment and inflation - are directly affected. The result is waves of expansion and collapse that are wholly unnecessary. This rolling tsunami could be largely avoided if the Fed was to reduce the implied delivery delay D by giving timely and direct attention to the financial consequences of yield-seeking distortions and misallocation of credit produced by its own activism. By waiting until those consequences show up directly in employment and inflation, which are themselves only weakly related to Fed actions, the present conduct of monetary policy virtually guarantees a recurring cycle of bubbles, crashes, and economic crisis. Feedback loops in the financial markets In the financial markets, we can think of mean-reversion (in valuations, profit margins, and the relationship between prices and fundamentals) as a balancing feedback loop. As valuations fall, expected returns improve, which encourages value-conscious investors to support stocks. Conversely, as valuations become elevated, expected returns deteriorate, which encourages value-conscious investors to reduce their exposure. In contrast, speculation is a self-reinforcing feedback loop, because elevated prices encourage trend-following speculation about further advances, and plunging prices breed speculation about a further collapse. The overall behavior of the system is driven by whichever loop is dominant at any point in time, and market outcomes can be particularly explosive when both loops suddenly operate in the same direction. From the standpoint of the observable data that guide our own investment discipline, historically reliable valuation measures such as MarketCap/GVA and various overvalued, overbought, overbullish syndromes are useful ways to gauge the condition of the balancing loop. Meanwhile, since investors tend to be indiscriminate when they are inclined to speculate, the uniformity or divergence of market internals across a broad range of individual stocks, industries, sectors, and security types (including debt securities of varying creditworthiness) is a useful way to gauge the condition of the self-reinforcing loop. Historically, the strongest expected market return/risk profiles are associated with a balancing loop that features undervaluation, joined with a self-reinforcing loop that has shifted to favorable uniformity across market internals. Even after the balancing loop suggests poor long-term outcomes as a result of overvaluation, the self-reinforcing loop can dominate, which is what we observe during valuation bubbles. My central error in the recent cycle (see the Box in last week’s comment for a full narrative) was to respond directly to measures that had always been followed by a shift in dominance from the self-reinforcing speculative loop to the balancing one. Quantitative easing instead encouraged an unchecked feedback loop of self-reinforcing speculation, much as the Fed enabled during the housing bubble, only with equities rather than mortgage securities as the preferred objects of that speculation. In the face of QE, one had to wait until market internals deteriorated explicitly before taking a hard-negative outlook; a condition we imposed on our discipline in mid-2014. If market internals were favorable here, it would be a signal that investors were still inclined to speculate. In that environment, safe, low-yielding liquidity would be treated the same way it has in recent years - as an inferior hot-potato to be unloaded in a reach for better returns. Instead, we presently observe the combination of wicked overvaluation on historically reliable measures, joined with deterioration in market internals that signals accelerating risk-aversion among investors. In this environment, safe, low-yielding liquidity is a desirable asset, and as we saw in 2000-2002 and 2007-2009, creating more of it is not likely, in itself, to support the market at all. The primary feature for investors to monitor, therefore, is not Fed action, but rather the uniformity or divergence of market internals directly. From the perspectives of both feedback systems and market history, the 40-55% market retreat we expect over the completion of this cycle may emerge, partially, in the form of an initial market crash. When the balancing behavior of value-conscious investors is persistently unable to dominate a self-reinforcing feedback loop of speculation, obscene valuations result. Historically, market crashes have emerged when existing downward pressure from the balancing loop (evidenced by an extended period of overvalued, overbought, overbullish conditions) is joined by a reversal in the self-reinforcing speculative loop (evidenced by a shift to downside uniformity across market internals). Keep in mind, however, that market crashes have typically only emerged after the market first loses something on the order of 14%, rebounds from its initial loss, and then breaks that initial support. For that reason, a break below the prior 1820-1870 support area for the S&P 500 could represent a well-defined catalyst for concerted selling pressure among speculators. A 40-55% retreat in the S&P 500 would take the most historically reliable valuation measures only to their historical norms, so I continue to view that outcome as a run-of-the-mill expectation. Of course, even without a move to typical valuation norms, a material improvement in market internals could signal a resumption of self-reinforcing speculation, so nothing requires a linear move to historically normal valuations. Conversely, even after a move below typical valuation norms, market internals could signal continued risk-aversion by investors that would invite further losses. In that case, the balancing loop would suggest strong long-term returns as a result of undervaluation, but the self-reinforcing loop could dominate, which is how the market has occasionally reached “secular” valuation troughs far below typical valuation norms. The best approach, in my view, is to carefully attend to both loops. Both of them are now operating in the same direction, and (aside from the weak and unreliable influence of short-term oversold conditions) both point sharply downward here. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |