|

|

||||||

|

|

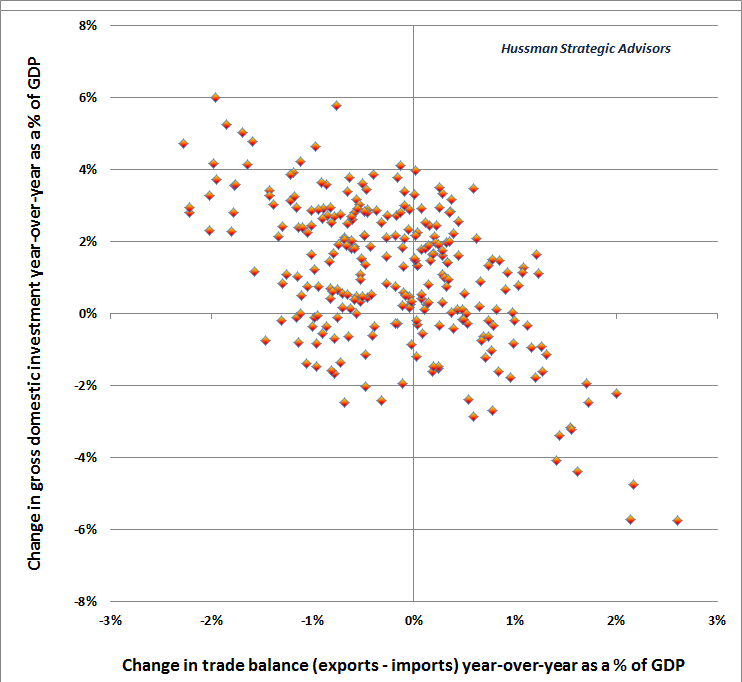

January 30, 2017 On Governance Those of you who have followed my work over the decades know that I look at the world holistically in terms of the interconnection and responsibility we have toward others, and I’ve never been much for separating “business” from those larger values. After all, most of my income regularly goes to charity, and nearly everything that remains follows our own investment discipline. Whether my comments on matters like peace, civility, economic policy or governance are well-received or not (and I'm grateful that they have been over the years), there are moments when one has the responsibility to speak if one has a voice. Our country faces many legitimate political disagreements. There are segments of America that view government as too bureaucratic, see foreign trade as a source of job insecurity, value national security as a priority, believe that each country has the right to a national identity, and feel that even a nation of immigrants has limits on the pace at which it can assimilate new citizens. They feel that their interests have been subordinated to an elitist philosophy that presumes that regulation is always beneficial, and that government always knows best. Those who value conservative policies have a right to advocate for them, and to support candidates who represent their interests. We can engage honestly and in good faith about those concerns, even where we disagree. Political issues like that are best settled not by insulting each other, but by openly expressing and listening to the values and concerns of each, and constructing solutions where each side might concede or trade various lower priorities, so that both can achieve their higher ones. From my perspective, the problem isn’t politics. A civil society can work out those differences. The immediate problem, and the danger, is the mode of leadership itself. A leader can call forth either the “better angels of our nature” or the worst ones. I am troubled for our nation and for the world because of the example of coarse incivility, mean-spirited treatment of others, disingenuous speech, thin temperament, self-aggrandizing vanity, puerile character, overbearing arrogance, habitual provocation, and broad disrespect toward other nations, races, and religions that is now on display as our country’s model of leadership. Despotism reveals itself through a reliance on threat, intimidation, bullying, coercion, and a chilling instinct to address problems through forms of termination, such as the killing of enemies and the exclusion and dismissal of adversaries. I am equally troubled by emerging risk, discussed below, to the Constitutional separation of powers. My intent is not to insult, but rather to name the elements of this pattern. Even in the face of our differences, it’s important that we refuse to resign ourselves to passively accepting or normalizing this model. A dismissive regard for truth, civility, transparency, ethics, and process is dangerous because it lays groundwork and creates potential for unaccountable, corrupt and arbitrary government. I believe that the people of our nation are both decent and vigilant enough to openly and loudly reject this behavior even where they might agree with various policy directions. There is no changing the outcome of what was already a dismal choice for many Americans, but we can insist on rejecting a model of uncivil behavior. It is unworthy of emulating for ourselves, much less for our children. To minimize detestable behavior is essentially to condone it. It is the refuge of cowards to defend obvious offenses by deconstructing them (“He wasn’t belittling a disabled person. See? He’s waving his hands while belittling this person too”), or to condone predatory behavior toward women by diffusing responsibility (“Yeah, but that other guy was also a predator”). Our intolerance for such a tireless pattern of offense shouldn’t depend on our race, or gender, or ability, or political views, even among those who view the man as a means to achieve political ends. With regard to international relations, the intentional provocation of both allies and trading partners is of deep concern. One might allow a generous interpretation that these provocations are intended to create new bargaining chips for use in trade negotiations (e.g. insulting Mexico, taunting China about Taiwan and the South China Sea). Yet even setting offenses aside, the associated protectionism is misguided economics, particularly at this point in the economic cycle. Given U.S. labor demographics, even a 4% unemployment rate in 2024 would bring average annual civilian employment growth to just 0.4% annually in the coming 8 years, while a 6% unemployment rate would place intervening job growth at just 0.2% annually. All other economic growth will rely on productivity growth (output per worker). The primary determinant on that front will be growth in U.S. gross domestic investment (GDI). Because of savings-investment dynamics, steep reductions in the trade deficit have always been associated with a collapse in U.S. GDI growth. Put simply, this new trade strategy courts recession or worse. That’s particularly true given a speculative financial bubble resulting from Federal Reserve’s misguided dogma that zero interest rates would bring prosperity without consequence. We now face the third financial collapse since 2000 (more data on that below). Meanwhile, we should recognize that foreign provocation has also been used around the world, and throughout history, as a strategy to expand domestic control. This often takes the form of “emergency powers.” Given the man’s clear aspiration to accrue and exercise authority, we shouldn’t naively ignore that potential. Recalling James Madison, “If tyranny and oppression come to this land, it will be under the guise of fighting a foreign enemy. The means of defense against a foreign danger historically have become the instruments of tyranny at home.” We have a leader that talks of the benefits of foreign plunder and the virtues of torture, yet we don’t recognize the seeds of despotism? Oh, that’s right, because we’re talking about the “enemy.” The enemy. It’s necessary to prosecute those who commit violence, in order to defend the rights of others, but to entertain notions such as torture, plunder, and the violation of human rights is an insult to the virtues our nation has sacrificed so much to achieve. Hatred does not remove hatred. We have to look into causes and conditions. Prejudice against a whole religion will not bring peace, nor will it contribute to an understanding of what motivates extremism. Whether the roots of violence are about foreign influence, territorial control, fear of losing power, protecting an existing way of life, or perceptions of injustice (whether legitimate or imagined), violence is often clothed in religion, both as a mobilization tactic, and so each side can claim that God is on their side. ISIS is no more about Islam than the Troubles in Ireland were about the religious faith of Catholics or Protestants, or the KKK was about Christianity. We can’t kill and torture our way to peace. We might satisfy pride and the desire for revenge, but the outcome would be a perpetual cycle of hatred, where our children eventually take our place in that cycle. The temptation is for sides both to turn up their high-beams, but as the Reverend Dr. Martin Luther King implored, “Someone must have sense enough to dim the lights.” Again, yes, those who actually commit violence should justly be prosecuted, but it’s madness to make enemies of entire populations. Along with enforcement against violent extremists, it’s essential to seek out and address the legitimate concerns of moderates. The first step toward peace happens when somebody has the courage to look deeply and ask, “How does the person I call my enemy suffer, and what can I do within my power, and consistent with my security, to address that suffering?” We are asked to rally around our new Administration, in the hope that it will be successful. Yet if, even at the outset, “success” asks us to accept the insult to loyal allies; if it asks us to accept daily incivility toward other citizens of our country; if it asks us to accept a demonstrably ill-conceived economic dogma that will do little but provoke trade frictions, weaken domestic investment, and provide tax benefits to the business sector, while indiscriminately shifting the costs and externalities of harmful action onto the public and the environment; if it asks us to accept blind prejudice toward other nationalities and religions; and if it flirts with even the prospect of foreign plunder and torture, then there is little question that we have already lost. A final concern relates to the separation of powers and the relationship between the express will of the People and the actions of the Executive. When the founders of this nation established the separation of powers in the U.S. Constitution, they were serious about it. Over time, through lack of vigilance, the public has allowed this separation to be undermined, to the point where people hardly recognize when violations occur. Here is a reminder. Article I Section I places all legislative powers with Congress. Article I Section 7 provides that all bills for raising revenue originate in the House of Representatives, which are then amended by the Senate. Article I Section 8 provides that only Congress has the power to declare war. Article I Section 9 provides that no money may be spent that is not pursuant to a law enacted by Congress. The Executive branch has the obligation under Article II Section III to “take Care that the Laws be faithfully executed”, and under the Constitution, only after a war is declared by Congress, or the military is called forth by Congress, does the President have the authority to direct military actions. In order to carry out the obligation of Article II Section III, the President may very well issue executive orders, but those orders are not laws in themselves. They are directives that apply only to members of the executive branch, for the purpose of upholding and faithfully executing existing laws previously passed by Congress. If an existing law infringes on the rights of the people, or overreaches the powers enumerated in the Constitution, the role of the Supreme Court is to adjudicate those disputes. If an executive order or an agency’s interpretation of an existing law is challenged, the Court has previously articulated a two-part test: if the intent of Congress is clear, the Court should “give effect to the unambiguously expressed intent of Congress.” If the intent of the law is ambiguous, the Court should examine whether the interpretation is a permissible construction. What I find alarming is that recent executive orders have been announced as new proclamations, instead of faithfully executing the provisions of existing laws duly enacted and funded by Congress under Article I of the Constitution. While the formal language of the orders themselves might reference existing laws, or give lip-service with the phrase “to the extent permitted by law,” the orders then self-contradict by directing the circumvention of those laws (for example, “to the extent permitted by law,” agencies are directed to “waive, grant exceptions from, or delay” the execution of the law, or to identify sources of funding for a project that is nowhere specified in the law). To ask "Where was this criticism during the past 8 years?" is to ignore the distinction between the faithful execution of laws one may dislike, and the invention of provisions that do not exist under prevailing law, which is what we now observe. The worst offender in prior years was not our former administration. It was the Federal Reserve, as Ben Bernanke created off-balance sheet "Maiden Lane" shell companies to purchase assets prohibited by law, in violation of Sections 13 and 14 of the Federal Reserve Act, making what he called "a money-financed gift to the private sector." Nobody recalls my silence. Congress later rewrote those sections to spell them out like a children's book. Even the media fail to discuss the fact that the Executive is both obligated to, and constrained by, the express will of the People, not the other way around. Only when Congress passes a law does it become the law of the land, provided it is otherwise Constitutional. To allow a weakening of these separate and enumerated powers is to invite the arbitrary exercise of authority, and even the risk of tyranny, rather than limited, representative government of the people that honors the Bill of Rights, equal protection, and the rule-of-law. I understand that facts are facts, and that this is the election result that our system produced. So what is the point, or the desired outcome, of protest? The fundamental outcome is to raise our vigilance; to preserve our character; to defend the rule of law and the separation of powers; to refuse to normalize or quietly endorse incivility; to promote diplomacy even as we pursue security; to demand more than the example set before us; to call us again and again to the better angels of our nature. We should voice our full expectation that Congress defend those enumerated powers, unmoved by speeches that assert the right of the executive to bind our nation to some “new decree” (who uses the word “decree” in an inauguration speech?) We should also ask that regardless of party, our representatives exercise those powers with dignity that befits our nation. As for individual issues, remember that the laws of our country are not established by tweets in the middle of the night. They are established by Congress. Citizens lose their voice when they fail to use it. All of us, left, right, or moderate, should protect that freedom. The U.S. Senate switchboard is (202) 224-3121. The U.S. House switchboard is (202) 225-3121. An actual person will answer, and can direct you to your state representative. Feel free, also, to forward or reprint these comments as you wish. Foreign trade, real investment, and corporate taxes While references for many of the foregoing observations are easily available, the basis for a few of the economic and financial comments is provided below. For data and evidence regarding labor market demographics and the components of GDP growth, see my December 12, 2016 comment Economic Fancies and Basic Arithmetic. On the relationship between the trade deficit and U.S. gross domestic investment, the following chart shows data since 1947, and captures the inverse relationship. Think of it this way: Whenever we import a dollar of goods and services, we export a dollar of “stuff” in return. That “stuff” can either be goods and services, or securities. So by definition, when the U.S. is a net exporter of securities to foreign investors, it must also be running a trade deficit in goods and services. That’s just an accounting identity. Investment and savings must be equal in equilibrium (this is also an accounting identity). From a financial perspective, an export of U.S. securities is an import of foreign savings. Putting this all together, booms in U.S. gross domestic investment (factories, capital goods, equipment, housing) are typically financed by an import of foreign savings and corresponding “deterioration” in the trade deficit. Conversely, “improvement” in the trade deficit is systematically related to deterioration in U.S. gross domestic investment.

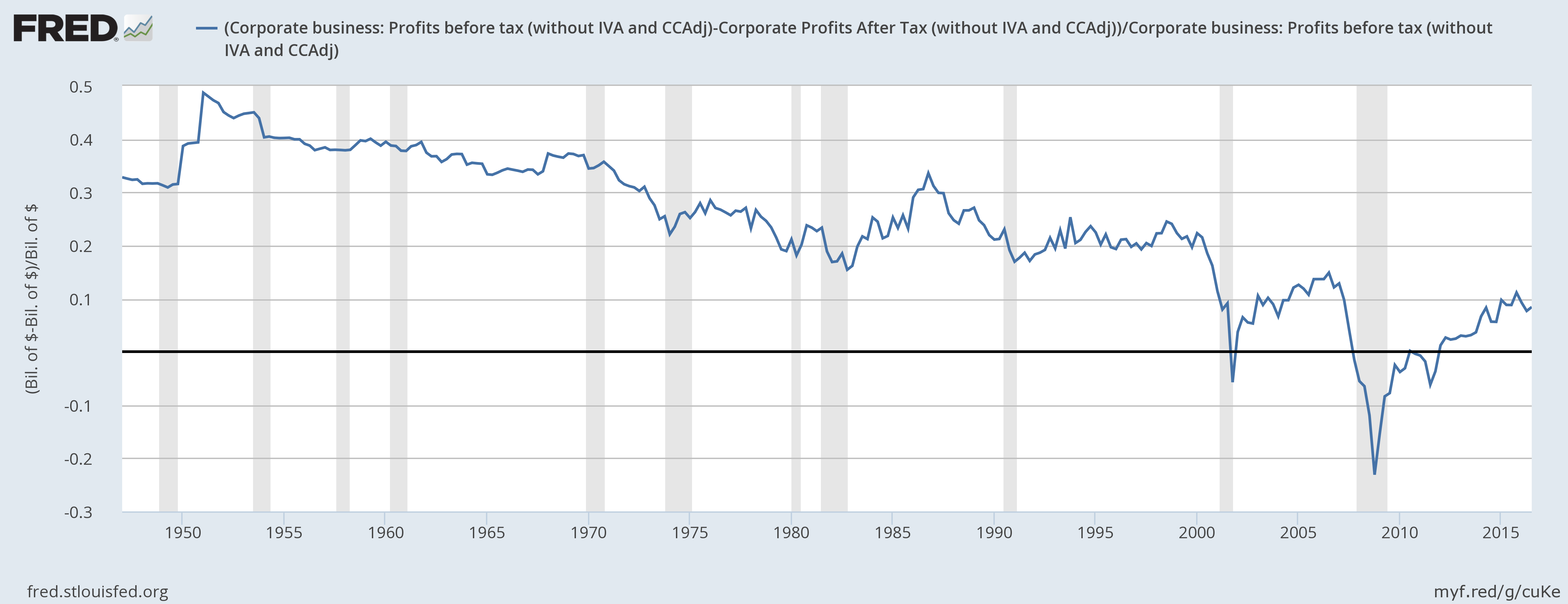

The result of all this is that U.S. investment booms are typically associated with a widening, not a narrowing, of the U.S. trade deficit. If you really want a collapse in U.S. gross domestic investment, cannibalize national savings by expanding the U.S. budget deficit through massive spending projects and lower taxes, and simultaneously limit the import of foreign saving by provoking a trade war aimed at “improving” the U.S. trade deficit. That’s precisely the direction this administration is heading. It seems we’ve forgotten the consequences of the Smoot-Hawley Tariff, which was passed in June 1930, at the outset of the Great Depression. When we look across history at periods of sustained economic growth like those that began in 1982 and 1990, we find that they began from points of significant slack, including high unemployment and a surplus on the trade balance (reflecting prior weakness in gross investment and the general economy). Neither condition is true today. With regard to tax policy, we already know from the 2004 tax holiday that reductions aimed at repatriation of foreign profits don’t result in more investment or jobs, but in stock buybacks and bonuses. I’ve always been a strong advocate of reduced monetary activism, of productive investment, of infrastructure that durably relieves capacity constraints (renewable energy would be one such area), and of expenditures and tax incentives toward those ends, particularly when they are tied to job creation or workforce training. Those approaches deserve bi-partisan support. But the effect of those shifts will emerge over decades, and will not materially alter the course of the real economy over a small number of years. As for current tax policy, the chart below shows effective U.S. corporate taxes as a percentage of pre-tax profits (the negative figures represent recessionary periods when corporations accrued a net tax benefit as a result of loss write-offs - click for a larger image). It’s quite possible that a change in corporate tax policy will change the way that corporations shelter their income, but given that the effective corporate tax rate is already lower than at any time except recessions and the recent recovery, my impression is that investors are vastly overestimating the increment to profits that would result from corporate tax reform.

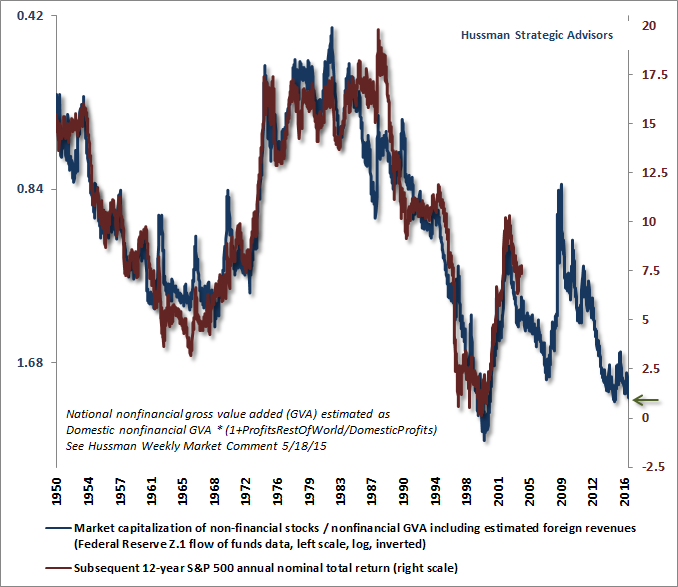

Presently, U.S. corporate taxes represent just over 4% of corporate revenues. Historically, the lowest level outside of recession (and the recent recovery) has been about 3%. From here, even moving to the lowest effective U.S. corporate tax rates in history would boost corporate profit margins by scarcely 1%. A massive speculative bubble meets an errant pin Given limited prospects for a material expansion in already-record profit margins, investors continue to face steep downside risk as the result of obscene market valuations. The consequences of years of yield-seeking speculation are still baked in the cake. Recall that the housing bubble and subsequent global financial crisis had two sources. On the demand side, the Federal Reserve’s decision to hold short-term interest rates at just 1% after the 2000-2002 market collapse created yield-seeking demand among investors for relatively safe but higher yielding alternatives to Treasury bills. They found that alternative in mortgage securities. On the supply side, a poorly regulated Wall Street was more than happy to create new “product” by churning out new mortgage securities. To create mortgage securities, you have to make mortgage loans, so Wall Street lowered credit standards and eventually lent to anyone with a pulse. A combination of "financial engineering" and lax oversight of ratings agencies and GSEs turned odious debt into AAA securities, hiding the default risk within government-insured institutions. As the bubble was taking form, I warned, "Why is anybody willing to hold this low interest rate paper if the borrowers issuing it are so vulnerable to default risk? That's the secret. Much of the worst credit risk in the U.S. financial system is actually swapped into instruments that end up being partially backed by the U.S. government. These are held by investors precisely because they piggyback on the good faith and credit of Uncle Sam." The resulting global financial collapse taught us nothing. That same misguided codependence between Federal Reserve and Wall Street has now produced yet another speculative episode. Years of zero-interest rate policy have produced a mature first half of a yield-seeking bubble-crash cycle, but the objects of speculation have now extended to both the stock market and the debt market (particularly the higher-yielding but junkier “covenant lite” variety that provides little protection in the event of bankruptcy). The unpleasant second half of this cycle remains ahead. To offer a sense of what’s likely to unfold, the following chart shows the ratio of nonfinancial market capitalization to corporate gross value added (MarketCap/GVA), which is more strongly correlated with actual subsequent S&P 500 total returns than any alternative measure we’ve studied over time. In the chart below, MarketCap/GVA is shown on an inverted log scale in blue. The red line is the actual subsequent S&P 500 nominal total return over the following 12-year period. At present, we project a likely market loss over the coming decade, with S&P 500 total returns averaging just 1% annually over the coming 12 years. Those aren't much different than the awful market outcomes I projected in real-time at the 2000 market peak. In that instance, the S&P 500 lost half of its value over the completion of the market cycle, with negative total returns for a buy-and-hold approach from March 2000 all the way out to November 2011. Every investment strategy has its season. My sense is that passive, value-insensitive investors are now facing another long, hard winter. Meanwhile, flexible, value-conscious investors are approaching the first day of spring.

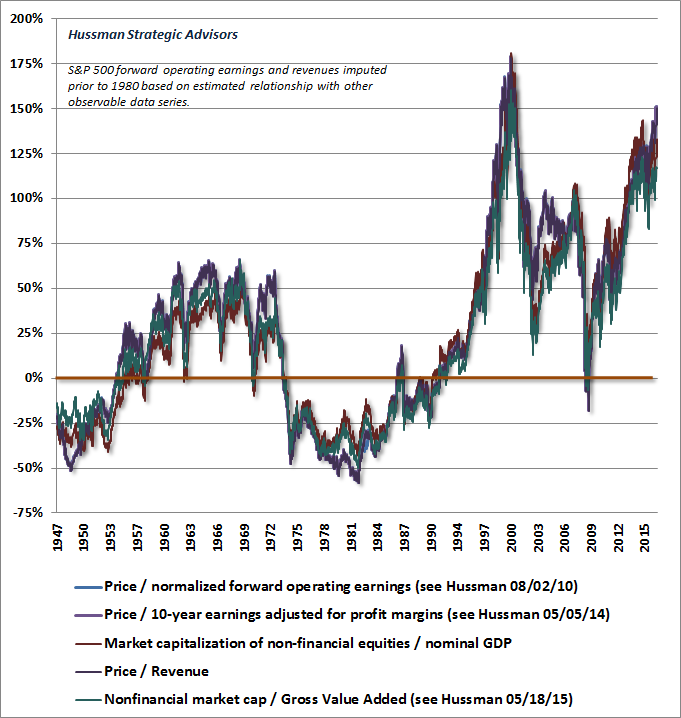

[Note: For a relative ranking of useful valuation measures, see Rarefied Air: Valuations and Subsequent Market Returns; for more detail on the link between these measures and subsequent returns, see Two Point Three Sigmas Above The Norm; and to understand why earnings-based measures should always be adjusted for the position of profit margins in the economic cycle, Margins, Multiples, and the Iron Law of Valuation]. The following chart shows some of the most reliable valuation measures we identify in terms of their percentage deviations from historical norms. These measures are currently 125% to 150% above (2.25 to 2.50 times) norms that have regularly been approached or breached over the completion of market cycles across history. At the 2000 and 2007 peaks, we correctly projected the probable extent of the losses that passive investors faced over the completion of the market cycle. Presently, we estimate that this speculative cycle will be completed by market loss in the S&P 500 in the range of 50-60%.

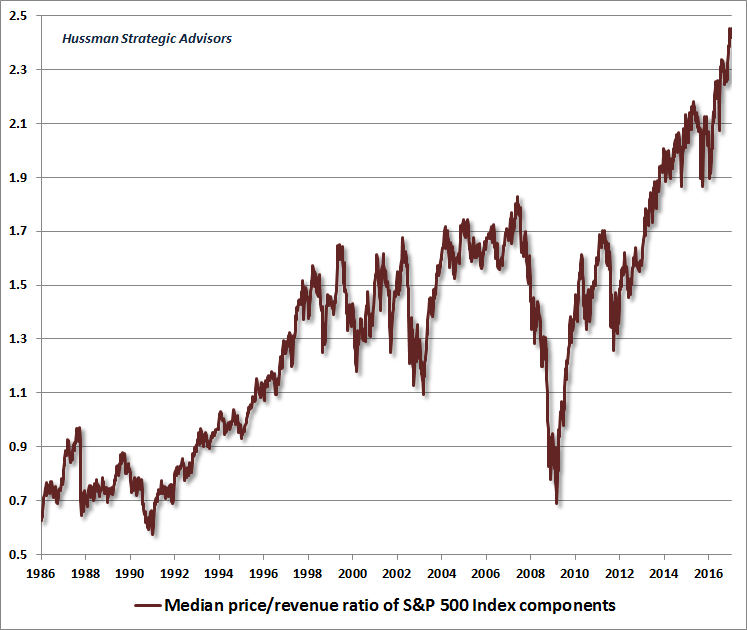

On the basis of capitalization-weighted indices, historically-reliable valuation measures now approach those observed at the 2000 bubble peak. Yet even this comparison overlooks the fact that in 2000, the overvaluation featured a subset of very large-capitalization stocks that were breathtakingly overvalued, while most stocks were more reasonably valued (see Sizing Up the Bubble for details). In many ways, the current speculative episode is worse, because it has extended to virtually all risk-assets. To offer some idea of the precipice the market has reached, the chart below shows the median price/revenue ratio of individual S&P 500 component stocks. This median now stands just over 2.45, easily the highest level in history. The chart presents data since 1986. The longer-term norm for the S&P 500 price/revenue ratio is less than 1.0. Even a retreat to 1.3, which we’ve observed at many points even in recent cycles, would take the stock market to nearly half of present levels.

A final comment. With the notable exception of the half-cycle since 2009, we’ve always come out admirably, and with quite a good reputation, over complete market cycles. In the early 1990’s, our historically-informed, value-conscious discipline encouraged a leveraged investment stance for years. We later anticipated both the 2000-2002 tech collapse (and its extent), and shifted to a constructive outlook in early 2003. We anticipated the 2007-2009 global financial crisis (and its extent), and encouraged a constructive outlook in late-2008 once the market was down by more than -40%, as we viewed stocks as undervalued. We also have our faults. We don't shine in the late-stages of a bubble, but that frustration quickly vanishes over the completion of the market cycle. Our real frustration in the half-cycle since 2009 began when I insisted on stress-testing our methods against Depression-era data, observing that valuations similar to those of early-2009 were followed by a further two-thirds loss in the market. We inadvertently stumbled in subsequent half-cycle as a result, because we relied too much on regularities of prior market cycles that were at least temporarily disrupted by zero-interest rate policy (see the “Box” in The Next Big Short for the full narrative). I saw a kind compliment from a reader last week, saying “he’s two steps ahead of all.” Unfortunately, the markets provide better rewards for being only one step ahead. In recent years, deranged Federal Reserve policy added several extra steps to extend the peak of an already dizzying precipice. We’ve made adaptations to address that, but those adaptations don’t encourage us to speculate during the peaking segment of a hypervalued market cycle where the Fed is already tightening and market internals (particularly among interest-sensitive securities) are already deteriorating. As always, our focus remains on the complete market cycle, and our outlook will change as the evidence does. The problem our nation faces is a serious one. We have now paired a massive speculative bubble with an errant pin that has every prospect of creating disruption. A steep financial retreat was already baked in the cake prior to the election. My concern is that having reached this precipice, there are few policies that have the capacity to make the consequences substantially better, but many that could make the outcomes substantially worse.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |