|

|

||||||

|

|

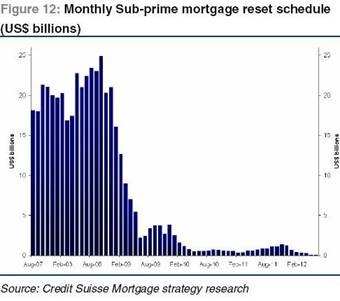

March 30, 2009 On the Urgency of Restructuring Bank and Mortgage Debt, Steps to Stability - Needed Legislation 1) Enable the receivership of distressed bank and non-bank financial institutions (including bank holding companies), encouraging voluntary debt-equity swaps as an alternative to the receivership / conservatorship of insolvent institutions. 2) Stabilize insolvent financial institutions through receivership if the bondholders of the institution are unwilling to swap debt for equity. In virtually all cases, the liabilities of these companies to their own bondholders are capable of fully absorbing all losses without the need for public funds to defend those bondholders. Receivership involves defending the customer assets, changing the management, wiping out the common stock and a portion of the bondholders' claims, continuing the operation of the institution in receivership, and eventually selling or reissuing the company to private ownership, leaving the bondholders with the residual. Massive bailouts using public funds are unnecessary, as are disorganized Lehman-style failures. 3) Allow "toxic asset" purchases using public funds only to the extent that the entire issuance of various securitized mortgage pools can be purchased "all or none" at a moderate percentage of face value. This would allow the underlying mortgages to be restructured - ideally writing them down to a similar percentage of face - reducing their foreclosure risk, and increasing the likelihood that public funds will be recovered. 4) Act quickly on foreclosure mitigation. Establish a Treasury conduit to administer (but not guarantee) property appreciation rights on restructured mortgages, again encouraging voluntary restructuring, using the Treasury conduit as a coordinating mechanism (additional details below). 5) Allow bankruptcy judges to substitute a portion of foreclosed mortgage obligations with equivalent claims on subsequent property appreciation. "Push-down" of mortgage principal without offsetting compensation rights to lenders should be emphatically avoided. Background Last week, the U.S. Treasury Secretary advanced two proposals; one was a call for regulatory reform that is absolutely essential to the resolution of the current financial crisis. The other was a recipe for the insolvency of the FDIC, which would squander public funds to subsidize private speculation in troubled mortgage securities. To understand this financial crisis, it is important to consider the balance sheet of a typical leveraged financial institution. The example below is similar to the one I presented last year in You Can't Rescue the Financial System if You Can't Read a Balance Sheet, but makes allowance for the fact that assets continue to be impaired due to policy failures, and that deposit banks such as Citigroup use more bond financing than investment banks. At the beginning of the recent crisis, the condition of U.S. financial institutions was much like the following: Good Assets: $90 Liabilities to Customers: $65 Now suppose there are losses in those questionable assets - not all the way to zero, but to $4: Good Assets: $90 Liabilities to Customers: $65 The above institution is insolvent. There are several ways to address this situation. Direct Capital Infusions The first possible response is to provide public capital directly to the banks, which is what the Treasury did last year by purchasing newly issued preferred stock of banking institutions. A capital infusion increases the asset side of the balance sheet (cash on hand) and increases the shareholder equity side of the balance sheet by the same amount. The difficulty is that without clear restrictions on the use of that capital, banks have the freedom to continue business as usual, including using the public capital to finance bonus payments and other expenditures. Absent explicit restrictions, there is also no assurance that the public funds will be lent out. To some extent, financing additional loans is not the purpose of capital infusions. The purpose is to replace the cushion of equity ("Tier 1 capital") that stands between the bank's customers and bankruptcy. Capital infusions are certainly a viable option to respond to the immediate threat of insolvency. These infusions were largely responsible for reducing the immediate threat to the U.S. financial system in late 2008. However, in the face of large and increasing losses, capital infusions are not sustainable. The public stands to lose the entire amount of funding if the institution fails, unless the infusions can be provided as a senior claim ahead of bondholders in the event of bankruptcy, and still be counted as "Tier 1 capital" otherwise. There are currently no legal or regulatory provisions to accomplish this. Note that gross private debt currently stands at about 350% of GDP, about double the historical norm. Meanwhile, many of the assets underlying this debt are being marked down in value by 20-30% or more. Given that GDP itself is about $14 trillion, a continued policy of bailouts will eventually require a commitment of public funds amounting to a significant fraction of $14 trillion. The "real" burden of the mounting federal debt will have to be devalued through inflation, or it will place an onerous claim on the nation's future production and capital investment (which might otherwise be able to provide for the needs of an aging population). Ultimately, if a financial institution is not capable of surviving without large and constant infusions of public capital, the stockholders and bondholders of that company - not the public - should be responsible for the losses incurred. As noted below, this can be achieved without customer losses or a disorganized Lehman-style unwinding. Toxic Asset Purchases The Treasury's proposal to address insolvency is to finance the purchase of impaired assets from the banks, primarily using taxpayer funds. But note that if the questionable assets are taken off of the bank's books at their actual value ($4 in the example above), there is absolutely no change on the liability side of the balance sheet. The bank's capital position does not improve. The "toxic asset sale" simply replaces the bad assets with cash. While this might improve the "quality" of the bank's balance sheet, it does not make the institution solvent. Indeed, the only way for the toxic asset sale to increase shareholder equity is if the buyer overpays for the asset. To accomplish this, the Geithner plan creates a speculative incentive for private investors, by effectively offering them a "put option," whereby taxpayers would absorb all losses in excess of 3-7% of the purchase amount. This is essentially a recipe for the insolvency of the Federal Deposit Insurance Corporation itself, which would provide the bulk of the "6-to-1 leverage." To the extent that it is not acceptable for the FDIC to fail, the Geithner plan implies an end-run around Congress, and would ultimately force the provision of funds to cover probable losses. An equal concern is that there is no link between removing "toxic assets" from bank balance sheets and avoiding large-scale home foreclosures and loan defaults. All the transaction accomplishes is to take the assets out of the bank's hands, to offer half of any speculative gains to private "investors," and to leave the public at risk for 93-97% of the probable losses. What the plan emphatically does not do is to affect the payment obligations of homeowners in a way that would reduce the likelihood of foreclosure. Moreover, the last thing that a bank would do with the proceeds would be to refinance such mortgages, because that would provide full repayment to the original lenders while taking on the risk of the newly refinanced loans. If part of the intent of Congress is to increase lending, this could be done directly by providing funds to GSEs or by broadly providing capital to solvent regional banks. This would be a much more effective way of increasing the volume of lending in the U.S. economy without putting taxpayers at risk of major losses. There is no need for the public to purchase impared assets in order to increase lending activity. Remember that the "toxic assets" held by banks represent pools of mortgages that have been cut up into dozens of individual pieces; the higher grade pieces having first claim to payments made on the underlying mortgages, and the lower grade pieces having claims to less likely payments. It is improbable that banks will be interested in selling off the better "tranches," and yet there is no benefit (aside from rank speculation) to owning the lower tranches unless the underlying mortgages can be restructured. As a result, the only point in the public having anything to do with these securitized mortgages is if all of the tranches of a given issue can be purchased simultaneously, so that the underlying payment obligations of the homeowners can be restructured. That is, if the entire issue could be purchased at 50% of the original face amount, the underlying mortgages could be written down by the same proportion. Those mortgages would then be far more likely to be repaid, and as a result, the restructured debt could be sold back into the financial markets without the need for taxpayers to hold it to maturity. There is no "all or none" mechanism in the Treasury's toxic assets plan to accomplish this. While the U.S. equity market advanced strongly on the day the Treasury plan was announced, most market indices were lower by the end of the week, and credit spreads (indicators of bondholder concerns about default risk) did not budge. It is far from clear that the Wall Street has confidence in the plan, beyond the fact that a trillion dollars to speculate on mortgage securities at taxpayer expense was not immediately rejected. Debt Restructuring From the beginning of the recent crisis, starting with Bear Stearns, I have emphasized that nearly all of the financial institutions at risk of insolvency have enough liabilities to their own bondholders to fully absorb all probable losses without any loss to customers or the American public. The sum total of the policy responses to this crisis has been to defend the bondholders of distressed financial institutions at public expense. Note that in the example balance sheet above, 30% of the liabilities of the institution represent debt to the company's own bondholders. It is these individuals - not homeowners, not the American public - that are being defended by the promise of trillions of dollars in public money. For example, while Citigroup has approximately $2 trillion in assets, those assets are financed not only by customer deposits, but also by nearly $600 billion in debt to Citigroup's own bondholders. It is these private bondholders who provided the funds for Citigroup to acquire questionable assets. The bondholders of distressed financial institutions - not the American public - should bear responsibility for the losses of those institutions. This can be accomplished, without harm to customers or the broader financial system, in one of two ways: 1) The bondholders could voluntarily agree to move a portion of their claims lower down in the capital structure, swapping debt for equity (preferred or common), allowing the bank to have a larger cushion of Tier-1 capital, avoiding insolvency, and hopefully allowing the bank to recover by its own bootstraps , preferably assisted by debt restructuring on the borrower side (via property appreciation rights and the like). Alternatively; 2) The U.S. government could take receivership of the financial institution, defend the customer assets, change the management, wipe out the stockholders and a chunk of the bondholders claims entirely, continue the operation of the institution in receivership, and eventually sell or reissue the company to private ownership, leaving the bondholders with the residual. Indeed, this is how the largest bank failure in history - Washington Mutual - was handled so seamlessly last year that it was almost forgettable. This is not Argentina-style "nationalization," but receivership - a form of "pre-packaged bankruptcy" that protects the customers and allows the institution to continue to operate, followed by re-privatization. This would fully protect all of the customers and depositors at no probable expense to the public. What should not be done is what was allowed in the case of Lehman Brothers - a disorderly failure, by which the company was allowed to fail with no conservatorship of the existing business. It was not the failure of Lehman per se, but the disorder resulting from its piecemeal liquidation, that caused distress to the financial markets. That said, it is true that the bondholders of major banks include pension funds, insurance companies, mutual funds, foreign investors and other holders that would be adversely affected by a writedown in bond values. But this is part of the contract - when one lends money to a financial institution, one also assumes the risk and responsibility of bearing the losses. Congress always has the ability to mitigate the losses of some parties, such as pension funds, if it is agreed that this is in the public interest. But to defend all bondholders of financial institutions at public expense is to commit the future economic output of innocent citizens to cover the losses of mismanaged financial institutions. As a result of the intervention by the Federal Reserve and the U.S. Treasury, even the bondholders of Bear Stearns stand to receive 100% repayment of both interest and principal on their bond investments. This is absurd. Receivership Provisions More than a year ago, in a March 24, 2008 comment (Why is Bear Stearns Trading at $6 instead of $2?), I emphasized the need for immediate authority to take distressed financial institutions into receivership in order to cut away the stockholder and bondholder obligations, while preserving the ongoing business, as well as its obligations to customers and counterparties: "At what point will investors figure out that the liquidity problems are nothing but the precursors of insolvency problems? At what point will investors stop begging the government to save private companies and recognize that the losses should be taken by the stock and bondholders of the offending financial institutions? If the Fed and the Treasury are smart, they will act quickly to figure out how to respond to multiple events like we've seen in recent days, to expedite turnover in ownership and quickly settle the residual claims of bondholders, without the kind of malfeasance reflected in the Bear Stearns rescue." It is essential for regulators to have the ability to take distressed institutions into receivership, so that customers and counterparties of insolvent financial companies can be fully protected. Ideally, this determination should be made not by the Treasury, but by the FDIC, which has a clearer regulatory role. The objective of receivership provisions would be to allow the failing institution to be partitioned into an operating entity (including whatever questionable loans are on the books), while cutting away the obligations to the stockholders and bondholders of that institution. Upon the sale, liquidation, or re-privatization of the institution, the bondholders would receive the portion of the proceeds that are not required as regulatory capital. To reduce the indirect effects of such receivership on other institutions, it would be helpful to legislate a restriction on the use of credit default swaps (essentially insurance contracts against the failure of a company's bonds), requiring that such swaps may be used for bona-fide hedging purposes only. That is, a credit default swap could not be entered for purely speculative purposes, but only to offset the default risk of the same or similar bonds held by the investor. Foreclosure Abatement Although trillions of dollars have been promised or committed in hope of resolving the current financial crisis, the simple fact is that virtually nothing has been done to reduce the incidence of foreclosures. Even if the plan to remove toxic assets from bank balance sheets is successful (however "success" might be defined), the rate of foreclosure will be unaffected, because no change in the payment obligations of homeowners will result. As with financial institutions, insolvent mortgages would best be addressed by a) voluntarily swapping debt for equity, or failing that; b) technical default and restructuring of the debt obligation. From the standpoint of homeowners, a debt-equity swap is equivalent to writing down the mortgage principal, while at the same time giving the lender an equal and offsetting claim on the future appreciation of the home. As I noted in The Economy Needs Coordination, Not Money, From the Government, "The most useful feature of government in resolving the foreclosure crisis is not its ability to squander taxpayer money, but its ability to provide coordinated action. I still believe that the best approach to foreclosure abatement would be for the Treasury to set up a special "conduit" fund to administer "property appreciation rights" or what I've called PARs. "Suppose a $300,000 mortgage is in foreclosure (or the homeowner and lender can agree to the following arrangement outside of foreclosure court). A reasonable mortgage restructuring might be to cut the principal of the mortgage to $200,000, and to create a $100,000 property appreciation right. The homeowner would agree to pay off the PAR to the Treasury (and administered through the IRS) out of future price appreciation on the existing home or subsequent property. The homeowner would be excluded from taking on any home equity loans or executing any "cash out" refinancings until the PAR was satisfied. The maximum PAR obligation accepted by the Treasury would be based on the value of the home and the income of the homeowner. "The lender would receive not a direct claim on that homeowner, but a participation in the Treasury's "PAR fund" which would pay out proportionately from all PAR proceeds received by the Treasury (technically, new shares in the PAR fund would be assigned based on a ratio reflecting the extent to which existing shareholders have already been paid off, so earlier shareholders don't receive more than they have coming to them). "Importantly, the Treasury would not guarantee repayment, but would simply serve as a conduit. There would be no "free lunch" at taxpayer expense. If the homeowner was to eventually sell the home and not purchase another, the obligation would become a low-interest loan obligation and would eventually be a claim on the estate of the homeowner, but with an initial exclusion at low income and a progressive recovery rate based on the size of the estate. The PARs would be tradeable, since they would be based on a single pool of cash flows, though they would almost certainly trade at a discount to face value. Assuming that the PAR obligations are fixed and don't increase at some rate of interest, then even if home prices were expected to take about 15 years to recover, the PARs would still trade at more than 50% of face. Given that recovery rates in foreclosure are running at only about 50% of the entire loan, it is clear that this sort of approach would be preferable to foreclosure in most cases. If this sort of mechanism were available, lenders might agree to outright principal reductions as well in preference a costly foreclosure process. "This sort of approach would reduce foreclosures without relying on free money from the government, or violating contract law. The PARs would provide a legally enforceable, diversified stream of cash flows at far lower cost than individual lenders would have to spend to collect from individual homeowners. Since home sales are taxable events, the IRS would be in an ideal position to enforce these obligations." The Danger of Inaction If there is any good news at present, it is that the capital infusions of late-2008 have temporarily stabilized the banking system, and that the U.S. economy is presently enjoying a brief and modest reprieve from the financial crisis. This is largely the result of an ebbing in the rate of sub-prime mortgage resets, which reached their peak in mid-2008, with corresponding mortgage losses and foreclosures a few months later. Since this crisis began, the profile of mortgage resets has been well-correlated with subsequent foreclosures.

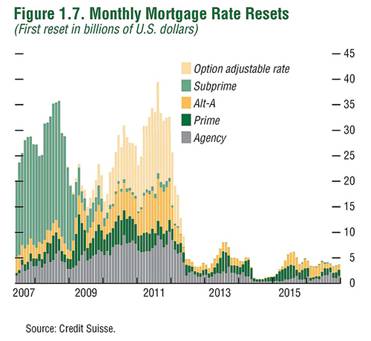

Unfortunately, the reset schedule above depicts only sub-prime mortgages. As the recent housing bubble progressed, the profile of mortgage originations changed, so that at the very peak of the housing bubble, new originations took the form of Alt-As (low or no requirement to document income) and Option-ARMs (teaser rates, with no required principal repayments). A broader profile of mortgage resets is presented below (though even this chart does not include the full range of adjustable mortgage products).

This reset profile is of great concern, because the majority of resets are still ahead. Moreover, the mortgages to which these resets will apply are primarily those originated late in the housing bubble, at the highest prices, and therefore having the largest probable loss. Though many of these mortgages are tied to LIBOR, and therefore benefit from low LIBOR rates, the interest rates on the mortgages are typically reset to a significant spread above LIBOR, and this spread remains constant as interest rates change. Undoubtedly, some Alt-A and option-ARM foreclosures have already occurred, but the likelihood is that major additional foreclosures and mortgage losses lie ahead. If we fail to address foreclosure abatement during the current window of opportunity (early to mid-2009), there may not be time for legislative efforts to contain the resulting fallout.

As a foreshadowing of the probable foreclosures ahead, the following is what the Federal Reserve, FDIC, and the Office of Thrift Supervision noted about option-ARMs and other loans in a colorful little booklet entitled "Interest-Only Mortgage Payments and Payment-Option ARMs: Are They For You?" , published in November 2006: "Owning a home is part of the American dream. But high home prices may make the dream seem out of reach. To make monthly mortgage payments more affordable, many lenders offer home loans that allow you to (1) pay only the interest on the loan during the first few years of the loan term or (2) make only a specified minimum payment that could be less than the monthly interest on the loan. "Whether you are buying a house or refinancing your mortgage, this information can help you decide if an interest-only mortgage payment (an I-O mortgage)--or an adjustable-rate mortgage (ARM) with the option to make a minimum payment (a payment-option ARM)--is right for you. Lenders have a variety of names for these loans, but keep in mind that with I-O mortgages and payment-option ARMs, you could face * "payment shock." Your payments may go up a lot--as much as double or triple--after the interest-only period or when the payments adjust. "In addition, with payment-option ARMs you could face * negative amortization. Your payments may not cover all of the interest owed. The unpaid interest is added to your mortgage balance so that you owe more on your mortgage than you originally borrowed. "Payment-option ARMs have a built-in recalculation period, usually every 5 years. At this point, your payment will be recalculated (lenders use the term recast ) based on the remaining term of the loan. If you have a 30-year loan and you are at the end of year 5, your payment will be recalculated for the remaining 25 years. The payment cap does not apply to this adjustment. "Lenders end the option payments if the amount of principal you owe grows beyond a set limit, say 110% or 125% of your original mortgage amount. For example, suppose you made minimum payments on your $180,000 mortgage and had negative amortization. If the balance grew to $225,000 (125% of $180,000), the option payments would end. Your loan would be recalculated and you would pay back principal and interest based on the remaining term of your loan. It is likely that your payments would go up significantly. "Be sure you understand the loan terms and the risks you face. And be realistic about whether you can handle future payment increases. If you're not comfortable with these risks, ask about another loan product." Judging from the reset schedule above, it is clear that more than a few borrowers ignored this advice. Market Climate As of last week, the Market Climate for stocks was characterized by reasonable valuations - moderate undervaluation on earnings-based measures that assume a reversion to above-average profit margins in the future, but continued overvaluation on measures that do not rely on future profit margins being above historical norms. This is an important distinction, because much of my constructive perspective about valuations late last year was based on the expectation of something of a "writedown recession" whereby our policy focus would have been on properly defending customers through greater use of the receivership process - demonstrating that the financial system itself could remain sound even while allowing the writedown and restructuring of debt. I believed, as I wrote a year ago, that "The U.S. economy will get through this without the requirement of massive public bailouts. What is required, however, is that the stock and bondholders of financial companies take due losses. Customers and counterparties need not, and I expect will not, be harmed." My optimism that our policy-makers would see clearly enough to follow this course was mistaken (fortunately, we are within 5% of where we stood at the beginning of this bear market). The misguided policy of defending bondholders against losses with public funds has increased uncertainty, crowded out private investment, harmed consumer confidence, and prompted defensive saving against possible adversity. We observe this as a plunge in gross domestic investment that is much broader than just construction and real estate, and a corresponding but misleading "improvement" in the current account deficit as domestic investment plunges. Aside from a few Nobel economists such as Joseph Stiglitz (who characterized the Treasury policy last week as "robbery of the American people") and Paul Krugman (who called it "a plan to rearrange the deck chairs and hope that that keeps us from hitting the iceberg"), the recognition that this problem can be addressed without a massive waste of public funds (and that it is both dangerous and wrong to do so) is not even on the radar. In short, attempting to avoid the need for debt restructuring by wasting trillions in public funds increases the likelihood that the current economic downturn will be prolonged, places a massive claim on our future production in order to transfer our nation's wealth to the bondholders of mismanaged financial companies, and raises the likelihood that any nascent recovery will be cut short by inflation pressures. We are nowhere near the completion of this deleveraging cycle. To the extent that we continue to force add-on effects in the form of declining employment and capital investment, we also reduce the likelihood that profit margins and returns on equity will recover to the historically above-average levels which have prevailed in recent years. The advance of the past few weeks has cleared the prior oversold condition and the market is now overbought in a generally negative Climate. As should be clear from last year's decline, the market can be severely oversold and only become more oversold, so an oversold condition is not a timing tool. That said, oversold conditions in clearly favorable Market Climates are often followed by strong advances, and overbought conditions in clearly unfavorable Market Climates are often followed by spectacular declines. At the recent market low, the Market Climate could certainly not be characterized as favorable, but at the present overbought level, there is considerable risk of a fresh plunge. Thus far, the recent advance has been focused on low-quality and distressed sectors such as financials, insurance and homebuilders. If the current advance is durable, we would expect to observe stronger market internals, greater participation among higher quality sectors, and a clear easing of credit spreads, which remain near their highs despite the advance in equities. On sufficient improvement in market internals, we would be inclined to establish call option positions that would gradually take us to a significantly less hedged position on persistent market strength, but we do not expect to eliminate our put option defenses until the combination of valuations and market action becomes clearly favorable, or until it is reasonable to expect a sustained economic recovery within a quarter or two. Nothing in our analysis of valuations, market action, or economic conditions compels us that removing downside protection is reasonable at present. In bonds, the Market Climate last week was characterized by unfavorable yield levels and relatively neutral yield pressures. The yields on Treasury Inflation Protected Securities have declined further in recent sessions, with inflation-adjusted yields on some issues dropping below 1%. I expect that a further decline in real yields would prompt us to reduce our holdings modestly, as it is doubtful that persistent inflation surprises will be a near-term outcome. I continue to view the U.S. dollar as vulnerable to depreciation given the rapid expansion in government liabilities, so the Strategic Total Return Fund continues to hold about 20% of assets in precious metals shares and foreign currencies, with a few percent in utility shares on the basis of longer-term total return prospects. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |