|

|

||||||

|

|

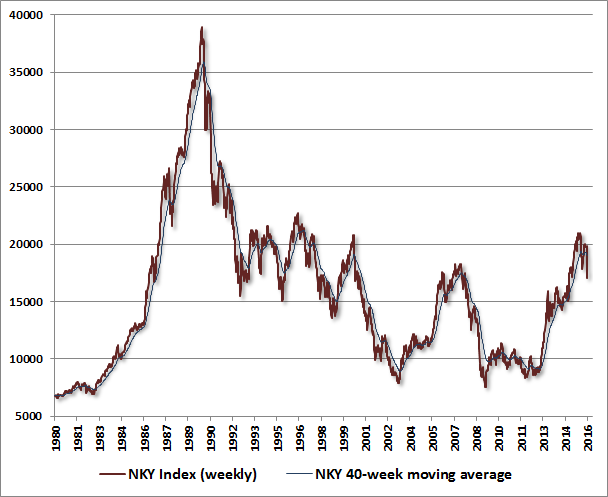

February 1, 2016 The Gas Pedal Is Useless When The Spark Plugs Are Gone Among the central lessons that investors should understand, before the completion of the current market cycle teaches it again, is this: the interpretation of nearly every piece of information - valuations, economic data, central bank action - is conditional on the status of market internals. While long-term investment returns are tightly correlated with good measures of valuation (e.g. MarketCap/GVA), investment returns over shorter portions of the market cycle are primarily driven by the willingness or aversion of investors to accept risk. Historically, the most reliable measure of investor risk-preferences is the behavior of market internals across a broad range of individual stocks, industries, sectors, and security types, including debt securities of varying creditworthiness. When market internals are broadly favorable, market overvaluation tends to be ignored over the short-run, and is typically followed by either flat returns or even more extreme levels of overvaluation. However, once internals deteriorate, signaling increasing risk-aversion among investors, the same market overvaluation is often associated with stock prices that drop like a rock (see The Hinge). When market internals are broadly favorable, weak leading economic data tends to be associated with only a temporary soft patch in economic growth. However, the same weak leading economic data, combined with deteriorating market internals, has a dramatically higher probability of being followed by recession (see When Market Trends Break, Even Borderline Data is Recessionary). The same is true of central bank action. There is no direct cause-and-effect mechanism that links central bank actions to the stock market. Rather, the effect of central bank action is dependent on the preference of investors to seek or avoid risk. When market internals are favorable and investors are inclined to speculate, safe, low interest (or zero interest, or negative interest) liquidity is viewed as an inferior asset to be abandoned like a hot potato. Since somebody has to hold every dollar of monetary base at every moment in time, Fed-created liquidity never actually comes “off the sidelines” - it just changes hands from one uncomfortable holder to the next. The key, however, is that in order to provoke yield-seeking speculation, a large segment of investors must be convinced that buying stocks or other risky assets will not subject them to capital losses. Uniformly positive market internals are an indication that investors broadly share that belief. In recent years, quantitative easing by central banks has turned the entire global financial system into one massive, yield-seeking carry trade in speculative assets. But the key to the carry trade mentality is that investors only "reach for yield" in riskier securities so long as they feel confident that the extra yield won't be wiped out by a decline in price. In contrast, if market internals are unfavorable, and particularly if valuations are still elevated, a drop in the level of interest rates may be unwelcome, but it’s not enough to provoke risk-averse investors to abandon safe liquidity and take on the risk of losing 10%, or 20%, or 50% of their money. Once market internals deteriorate, central bank easing fails to provoke speculation, on average. The gas pedal is useless when the spark plugs are gone. Worse, central bank easing, in the context of unfavorable market internals, is typically a response to unexpected economic weakness. As a result, such “panic” easings are often followed by a further collapse. Recall, as I noted in The Line Between Rational Speculation and Market Collapse, that the Fed began cutting interest rates on February 11, 1930 - nearly two and a half years before the market bottomed. The Fed cut rates on January 3, 2001 just as a two-year bear market collapse was starting, and kept cutting all the way down. The Fed cut the federal funds rate on September 18, 2007 - several weeks before the top of the market, and kept cutting all the way down. In the context of the recent half-cycle advance since 2009, remember also that it was not Fed easing that put the bottom in, so to speak. What ended the crisis was the March 2009 decision by the Financial Accounting Standards Board to abandon mark-to-market rules and allow banks and financial companies to use "significant judgment" in valuing their troubled assets. In hindsight, regulators went right along. The specter of widespread defaults vanished with the stroke of a pen (followed by a million sharpened pencils in accounting departments up and down Wall Street). Central bank easing does not, in itself, provoke speculation. Rather, the market response is dependent on investor risk-preferences, as indicated by market internals. Fed easing only reliably benefits the stock market when market internals are already favorable. Historically, it has been best to respond directly to internals than to jump the gun in the belief that central bank action will shift their condition. Panic at the Bank of Japan Last week, Bank of Japan Governor Haruhiko Kuroda, supported by a slim 5-4 board vote, announced a move to cut short-term interest rates to negative -0.1%, effectively charging banks for deposits held with the BOJ. While the knee-jerk response to central bank easing moves is invariably positive, investors should be careful to recognize the context surrounding this move. Based on the broad market action of Nikkei component stocks, market internals in Japan have deteriorated sharply since December, in contrast to most of the period since August 2012. Following a doubling of the Nikkei over that horizon, the current policy shift comes at a time when both valuations and market internals in Japan have shifted to the most unfavorable status in years. A few charts may offer some perspective. First, note the recent breakdown in the Nikkei, after a long advance since 2012. This retreat has been broad-based, with concerted weakness across numerous industries and sectors. In this environment, one might question whether the loss of a fraction of a percent in interest annually is likely to provoke investors to expose themselves to potentially major losses in a market with no internal support. That’s the same question that one could have asked in the U.S. markets in February 1930, or January 2001, and September 2007, all which were followed by major market collapses despite repeated and aggressive easing by the Fed.

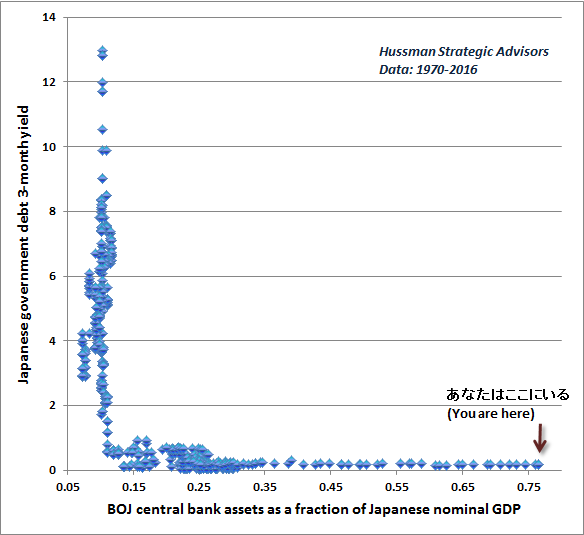

What’s somewhat striking is that having moved the Japanese monetary base from 20% of GDP to more than 75% of GDP in recent years, with very little economic response, anyone would seriously call this liquidity “ammunition.” From an economic perspective, the expansion in the BOJ balance sheet has been accompanied by a precisely offsetting collapse in monetary velocity, with little effect on either real GDP or inflation. From a speculative perspective, while the Nikkei Index remains lower than it was in 1986, 30 years ago, investors have demonstrated risk-seeking inclinations in recent years, holding the Nikkei above its 40-week average during most of the period from 2012 until mid-December of last year. At present, however, one should take quite a negative signal from the BOJ's action, because it's clearly a response to deteriorating economic prospects. A favorable shift in market internals would be supportive of speculation in Japan, but that possibility should be monitored explicitly. One can’t rule it out, but there is no inherent or reliable tendency for central bank easing to reverse unfavorable market internals, or to avoid steep further market losses (recall 2000-2002 and 2007-2009 in the U.S.). All of this madness goes back to Ben Bernanke, who was the intellectual architect of quantitative easing, and who successfully encouraged Japan to pursue this policy in 2000. Thoughtful, informed policy is typically conducted within a carefully considered "range" having reasonable upper and lower bounds. Bernanke’s abandonment of every such bound has produced policies that are, quite literally, deranged.

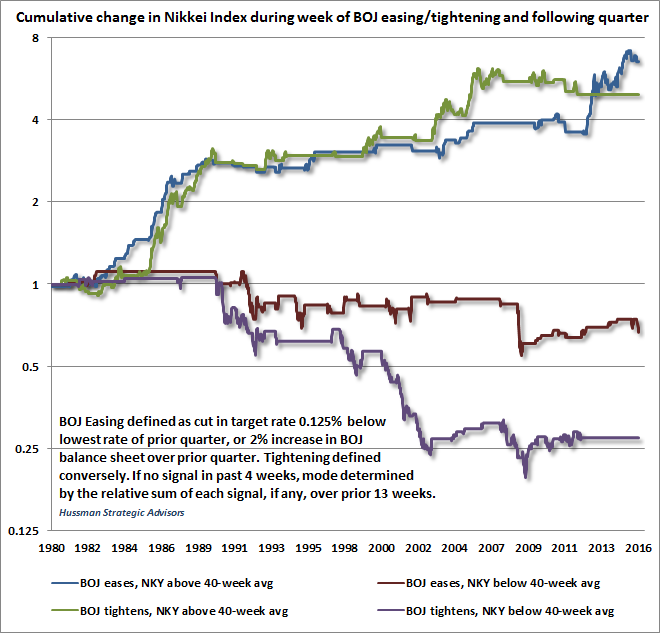

Again, when market internals are unfavorable, and particularly when valuations are still elevated, a drop in the level of interest rates may be unwelcome, but it’s not enough to provoke risk-averse investors to take on the risk of losing 10%, or 20%, or 50% of their money. Central bank easing relies on a scarcity of risk-aversion in order to have a material effect on speculation and stock prices. The chart below is a Japanese version of the study I presented in When an Easy Fed Doesn’t Help Stocks, and When it Does. In this case, market action is classified based simply on whether the Nikkei average is above or below its 40-week moving average. As we observe in the U.S., central bank easing in Japan only reliably benefits the stock market, on average, when market action is already favorable, indicating a preference among investors to accept market risk. Notably, even BOJ tightening is associated with gains in the Nikkei index, provided that investors are inclined to take risk. In contrast, once market support breaks, neither BOJ easing nor BOJ tightening is associated with subsequent gains in the Nikkei.

The upshot is that valuations, economic data and central bank actions have to be interpreted within the context of prevailing market internals and the investor risk-preferences that they convey. When investors are risk-averse and internal support has dropped away, a small change in interest rates is simply not sufficient to encourage risk-seeking. Understand that the context of the recent move by the Bank of Japan is materially different than the context that the BOJ has operated under since 2012. The current move does not reflect bold action on the basis of historically-informed cause-and-effect relationships or sound economic theory. Central bank actions in Japan and elsewhere merely reflect the continuation of demonstrably ineffective, deranged, and historically baseless experimentation. There is no material impact of QE on the real economy. On this point, it’s simply not true that “we have no counter-factual.” Rather, one can show that economic outcomes of the U.S., European, and Japanese economies in recent years have been no better than what would have been predicted based on prior values of purely non-monetary variables alone. In contrast to most of the period since 2009, central bank actions are now joined by an environment that has shifted to risk-aversion. When investors are risk-seeking and market internals are favorable, quantitative easing can certainly add speculative fuel. When investors feel confident that they can earn positive returns on risky assets, zero-interest liquidity is a hot-potato, and creating more of the stuff encourages speculation. In contrast, once risk-aversion sets in among investors, QE loses its ability to promote speculation because risk-free liquidity becomes a desirable asset rather than an inferior one. Investors should not expect favorable outcomes from this environment. As usual, I should emphasize that if market internals improve measurably, the immediacy of our downside concerns would ease considerably. But we are monitoring that prospect directly and explicitly, rather than assuming that central bank easing will automatically produce this improvement. Aside from short-lived, knee-jerk responses, there is no historical basis to assume that central bank easing will promptly encourage fresh speculation in an overvalued market that has lost internal support. To the contrary, as investors should recall from February 1930, January 2001, and September 2007, central bank easing in an internally-weak market environment has typically been a panic response to unexpected economic deterioration. Such actions should be interpreted as the panic signals that they are.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |