|

|

||||||

|

|

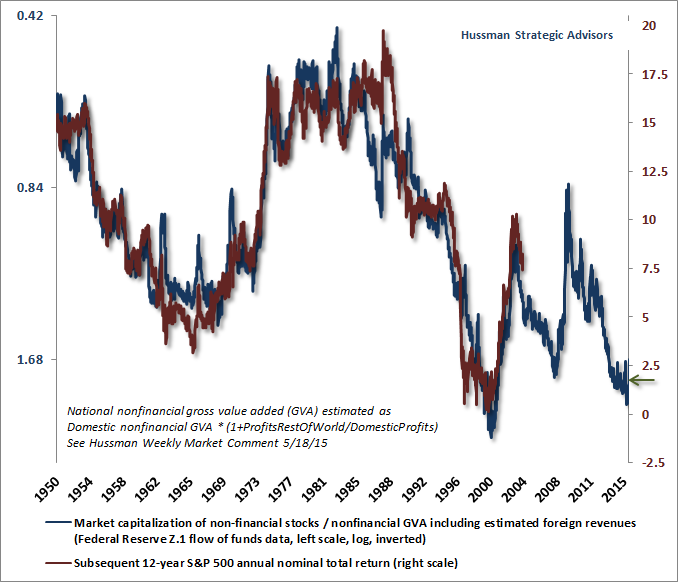

March 7, 2016 A Continued Undertone of Risk-Aversion Last week, the most historically reliable equity valuation measures we identify (having correlations of over 90% with actual subsequent 10-12 year S&P 500 total returns) advanced to more than double their reliable historical norms. When valuations have been near those historical norms, the S&P 500 has generally followed with average nominal total returns of about 10% annually. In contrast, current valuations are associated with expected 10-12 year total returns of about zero, with negative expected returns on both horizons after inflation. Now, in the context of low interest rates, some investors may view the prospect of zero total returns on stocks over the coming decade as reasonable and competitive. That’s fine, but understand that through most of the period prior to the 1960’s, interest rates regularly visited levels similar to the present, yet these same measures of stock valuations typically resided at well below half of present levels. In my view, investors who view current valuations as “justified relative to interest rates” are really saying that a decade of zero total returns on stocks is perfectly adequate compensation for the risk of a 45-55% market loss over the completion of the current market cycle - a decline that would historically be merely run-of-the-mill given current valuations, and that certainly cannot be precluded by appealing to low interest rates. See, across history, prospective and realized returns on stocks have been nowhere near as correlated with the level of interest rates as investors seem to believe. Indeed, because the level of interest rates at any point in time is highly correlated with the level of nominal economic growth over the preceding decade, the relationship between starting valuations and actual subsequent S&P 500 nominal total returns is nearly independent of interest rates. That is, interest rate and growth effects tend to cancel out over the holding period. For historical evidence and mathematical formalization of this, see Rarefied Air: Valuations and Subsequent Market Returns. Note that the argument is not that stock valuations themselves are independent of interest rates. Rather, once a given level of valuations is established, investors can read directly from those valuations what return they are likely to enjoy over the following 10-12 year period. The chart below shows this relationship using market capitalization to corporate gross value added (blue, on an inverted log scale) versus actual subsequent 12-year S&P 500 nominal total returns (red).

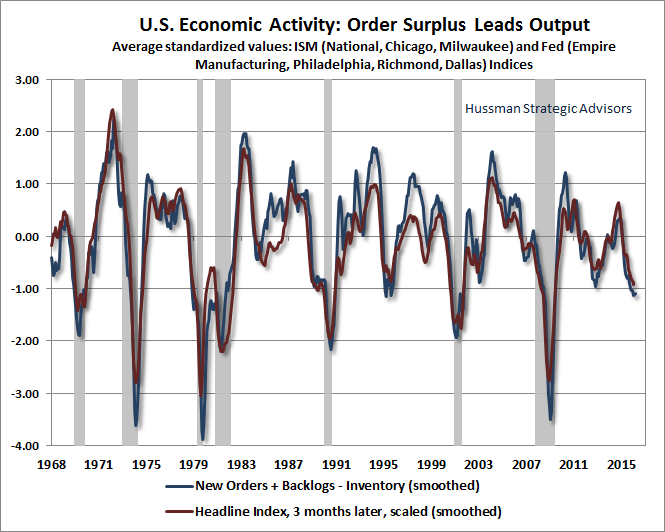

Put simply, my expectation is that investors will find 10-12 years from today that the relationship between valuations and actual subsequent market returns has played out exactly as it has across history. As a rough guide to how prospective returns will change over the completion of the current market cycle, we presently estimate that in order to establish expected 10-year S&P 500 total returns of 5% annually, the S&P 500 would have to decline to the mid-1500’s. In order to establish 10% expected total returns, we estimate that a decline to the 1000 level on the S&P 500 would be about right. Note that the completion of every market cycle across history has brought valuations toward or below levels consistent with 10% annual prospective returns. The dismal long-term prospects for market returns are essentially baked-in-the-cake as a result of present, extreme valuations. On the other hand, the prospects for the market over shorter portions of the market cycle have very little to do with the level of valuation and much more to do with the risk-seeking or risk-averse inclinations of investors. Because risk-seeking investors tend to be indiscriminate about it, we find that the best measure of risk-seeking is the uniformity of market internals across a broad range of individual stocks, industries, sectors, and security types, including debt securities of varying creditworthiness. Market internals have historically acted as the “hinge” between overvalued markets that remain stable (or even advance further) and overvalued markets that are prone to collapse. In recent weeks, we’ve certainly seen an improvement in many of these measures from their lows in January and February, but to-date, the extent of that improvement is of the character we typically observe during bear market rallies and short-squeezes - essentially a “fast, furious, prone-to-failure” clearing of oversold conditions on progressively dull trading volume. That brings the S&P 500 Index to about 2000, the same place it was in August 2014. Among widely followed indicators, credit spreads have narrowed, but still remain well above where they were say, 6 months ago. Breadth has improved, but is also now quite overextended on a variety of measures. Participation remains weak, with about two-thirds of individual stocks still below their 200-day averages and about 20% below their respective highs, on average. Our own measures are consistent with this profile, showing a relief from oversold extremes, but little evidence of a robust shift to risk-seeking. That’s certainly not to rule out the possibility that the recent advance could carry further and shift our measures of market internals to a more favorable condition, and it’s certainly not to rule out a further short-squeeze. But at present, we continue to infer a continued undertone of risk-aversion from market internals. We’ll respond to changes in the evidence as they emerge. As I’ve noted for some time, the immediacy of both our market and economic concerns would be substantially reduced in the event that market internals improve on our measures. That said, the most likely impact on our investment outlook would be to shift us to neutral, or something that might be described as “constructive with a safety net.” Without a more substantial retreat in valuations, I don’t see any meaningful likelihood that we’ll be encouraging an aggressively bullish market outlook in the near future. But provided such a retreat over the completion of this market cycle, I expect that opportunity to emerge like day follows night. Economic Notes On the economic front, despite the recent market advance and strength in payroll employment, observable economic data remain broadly consistent with the likelihood of an oncoming U.S. recession. A clear improvement in our measures of market internals would defer the immediacy of that concern, and would also create an environment where monetary easing would tend to support speculation in the financial markets. But historically (including the period since 2009), unless investors are already inclined to speculate, easy money fails to provide support to the market. Default-free money does not act as an inferior “hot potato” when investors are risk-averse. Recall, for example, that stocks collapsed in 2000-2002 and 2007-2009 despite persistent and aggressive Fed easing. At present, our recession expectations remain unchanged. It’s important to recognize the sequence in which economic data typically deteriorates. As I’ve frequently emphasized, the earliest indications of an oncoming economic shift are usually observable in the financial markets, particularly in growing deterioration across broad market internals, and widening credit spreads between debt securities of varying creditworthiness. The next indication comes from measures of what I call “order surplus”: new orders, plus backlogs, minus inventories. When orders and backlogs are falling while inventories are rising, a slowdown in production typically follows. If an economic downturn is broad, “coincident” measures of supply and demand, such as industrial production and real retail sales, then slow at about the same time. Real income slows shortly thereafter. The last to move are employment indicators - starting with initial claims for unemployment, next payroll job growth, and finally, the duration of unemployment. At present, we have the same syndrome of indications that allowed us to correctly identify oncoming recessions in October 2000 and again in November 2007. By contrast, I did anticipate a recession in 2011-2012 based on alternate criteria, particularly weakness in employment data that was subsequently revised away, and without the internal deterioration we observe at present. Notably, the economic consensus has never anticipated a recession in real time. As is true with any classification approach, increased sensitivity to true signals nearly always comes at the risk of occasional false signals. The chart below updates our measure of order surplus through February. Along with the deterioration we continue to observe in the order surplus as measured by regional and national Fed and purchasing managers surveys, actual industrial production and the value of new orders in manufacturing have contracted on a year-over-year basis. We’ve observed a slowdown, but not a downturn, in real retail sales and real personal income, so those remain areas of focus as we monitor the sequence of economic data.

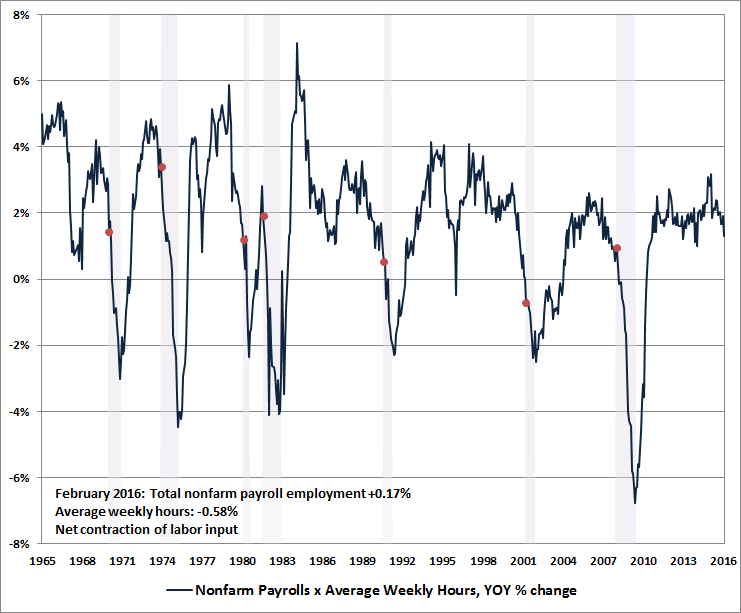

Among other confirming indicators of recession that I’ve regularly discussed, we now observe a gradual widening in the “consumer confidence spread,” with the “future expectations” index falling relative to the “present situation” index. We would be more compelled if this was accompanied by a drop in consumer confidence of 20 points or more below its 12-month average, which typically accompanies the beginning of recessions. We don’t see that yet. Employment data is always the most lagging, and deterioration typically begins with initial claims for unemployment. Though we don’t expect it just yet, a jump in new claims to about 20% above year-ago levels (currently implying about 320,000 weekly new claims) would be indicative of a shift from “oncoming” to “commenced” recession. The unemployment rate itself rarely turns sharply higher until well into recessions (and rarely turns down until well into economic recoveries). So while the unemployment rate is an indicator of economic health, it is not useful to wait for major increases in unemployment as the primary indicator of oncoming economic changes. Slowing growth in employment and hours worked do tend to accompany the beginning of recessions. Combining the two, a decline in aggregate weekly hours over a 3-month period typically accompanies the start of a recession. On Friday, February payrolls came in with a gain of 242,000, following a revised gain of 172,000 in January. While this is fine as far as those figures go, the February gain represented a +0.17% increase in total nonfarm payroll employment. Unfortunately, average weekly hours fell by -0.58%, resulting in a net contraction in labor input during the month of February. Interestingly, what was missing from the discussion of month-to-month changes in the job figures was any discussion of revised levels. See, the originally reported December jobs figure was 143,242 (thousand jobs), which has now been revised down by nearly 100,000 jobs, to 143,146. February total nonfarm payrolls are less impressive relative to the originally reported December figure. Put another way, from the standpoint of what we thought was true at the beginning of the year, an average of only 159,000 new jobs per month were created during January and February. The chart below shows the year-over-year change in the product of nonfarm payroll employment and average weekly hours (essentially a measure of overall labor input). The levels accompanying the start of prior recessions are indicated by the red dots. While the current level isn’t entirely inconsistent with a new recession, I continue to believe that “oncoming” is the most appropriate word to associate with our recession expectations, at least as of February.

On the subject of monetary easing, remember that the central requirement for easy money to have a speculative effect is that investors can’t be too concerned about capital losses. When investors reach for yield, the quiet assumption is that the extra yield won’t be wiped out by a decline in price. In a risk-seeking environment, as evidenced by uniform strength across a broad range of market internals, investors are prone to make that assumption. In a risk-averse environment, they are not. The same is true for decisions about spending and real investment. Think about it. Suppose that every central bank in the world was to immediately move interest rates negative, announcing that rates will be held at -0.5% for the next four years. From a financial perspective, this would really be no different than putting up a sign that says “Everything On Sale! Prices Slashed 2%!” Now, if you don’t think that slashing prices by a cumulative amount of 2% (-0.5% x 4 years) is enough to prompt consumers to spend, or induce corporations to launch major investments and capital spending projects, or drive speculators to load up on risky securities, you shouldn’t believe that even four years of -0.5% interest rates would have much effect on the economy or the financial markets either. That said, recognize the conditions where monetary easing does tend to be effective. Once market internals signal a risk-seeking environment, all low-interest money becomes a hot potato, and monetary easing reliably encourages speculation. But in a risk-averse market without robust market internals, central banks can throw everything at the wall, and very little will stick beyond a brief period of initial enthusiasm. As I emphasize nearly every week, the immediacy of both our market and economic concerns would be reduced in the event that market internals were to improve materially on our measures. Over the past month, we’ve observed what appears to be a typical “fast, furious, prone-to-failure” rebound from oversold levels, but not a shift that would allow us to infer a return to risk-seeking preferences among investors. That may change, and we’ll take the evidence as it arrives. Barring such a shift, I continue to believe that both vertical market losses and an imminent U.S. recession should be viewed as significant and probable risks. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |