|

|

||||||

|

|

March 28, 2016 Run-Of-The-Mill Outcomes vs. Worst-Case Scenarios With the S&P 500 Index at the same level it set in early-November 2014, and the broad NYSE Composite Index unchanged since October 2013, the stock market continues to trace out a massive arc that is likely to be recognized, in hindsight, as the top formation of the third financial bubble in 16 years. The chart below shows monthly bars for the S&P 500 since 1995. It's difficult to imagine that the current situation will end well, but it's quite easy to lose a full-cycle perspective when so much focus is placed on day-to-day fluctuations. The repeated speculative episodes since 2000 have taken historically-reliable valuation measures to extremes seen previously only at the 1929 peak and to a lesser extent, the 1937 peak (which was also followed by a market loss of 50%). Throughout history, at each valuation extreme - certainly in 2000, 2007 and today - investors have openly embraced rich valuations in the belief that they represent some new, modern and acceptable “norm”, failing to recognize the virtually one-to-one correspondence between elevated valuations and depressed subsequent investment outcomes.

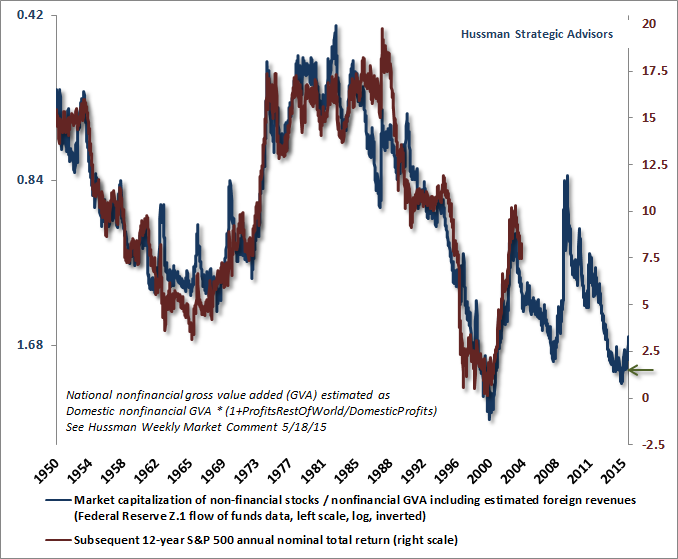

Wall Street analysts talk endlessly on financial television about low interest rates “justifying” current valuations, without completing the story that even if this were true (and it’s not - see the links below), these rich valuations still imply predictably dismal future returns on stocks, particularly on a 10-12 year horizon. The fact is that the relationship - the direct mapping - between the most historically reliable valuation measures and actual subsequent market returns hasn’t changed a bit in nearly a century. I emphasize the phrase “historically reliable” because many of the most popular valuation measures vaunted by Wall Street have a strikingly weak correlation with actual subsequent market returns, and that record gets no better when one imputes these measures across an extended historical dataset (see in particular my August 2007 comment Long-Term Evidence on the Fed Model and Forward Operating P/E Ratios, and my May 2015 piece Recognizing the Risks to Financial Stability). Though corporate earnings are necessary to generate deliverable cash to shareholders, comparing prices to earnings is actually quite a poor way to estimate prospective future investment returns. The reason is simple - most of the variation in earnings, particularly at the index level, is uninformative. Stocks are not a claim to next year’s earnings, but to a very long-term stream of cash flows that will be delivered into the hands of investors over time. Corporate earnings are more variable, historically, than stock prices themselves. Though “operating” earnings are less volatile, all earnings measures are pro-cyclical; expanding during economic expansions, and retreating during recessions. As a result, to quote the legendary value investor Benjamin Graham, “The purchasers view the good current earnings as equivalent to ‘earning power’ and assume that prosperity is equivalent to safety.” Not surprisingly, the valuation measures having the strongest correlation with actual subsequent investment returns across history are smoother, and serve as better “sufficient statistics” for the relevant long-term cash flows. Across the scores of measures I’ve evaluated or created over three decades of research, the ratio of non-financial market capitalization to corporate gross value added (essentially corporate revenues, including estimated foreign revenues, excluding double-counting of intermediate inputs) is best correlated to actual subsequent market returns over a 10-12 year horizon. The 12-year horizon is notable, because that’s the point where serial correlation drops to zero, and is therefore the most likely point at which full mean-reversion can be expected, on average. In the chart below, the blue line tracks MarketCap/GVA on an inverted log scale (left). The red line is the actual subsequent S&P 500 nominal annual total return over the following 12-year period.

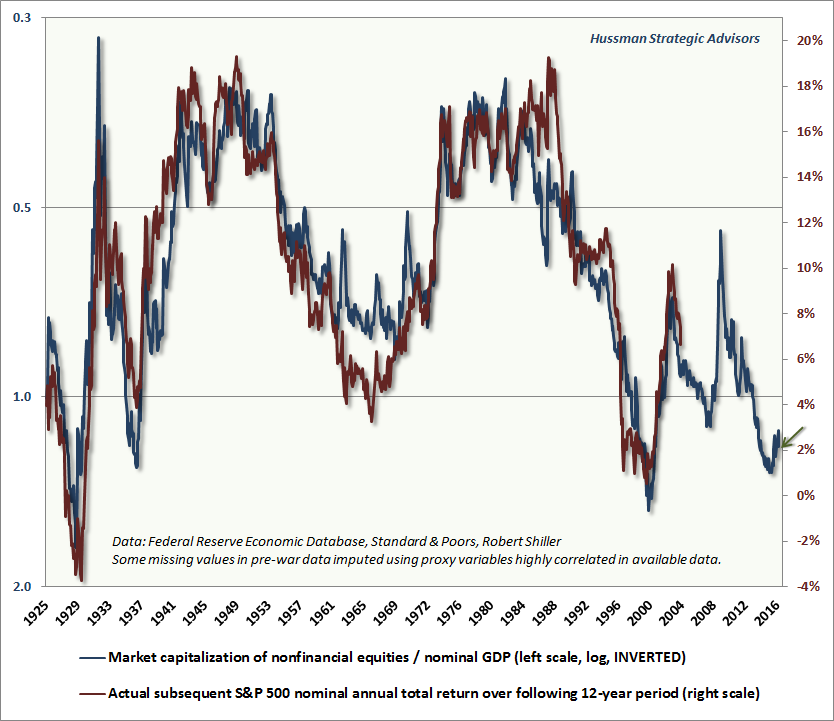

The essential thing to notice is that the relationship between valuations and total returns hasn’t deteriorated at all in recent years. Yes, the period since the mid-1990’s has repeatedly taken stocks to richer valuations than we’ve seen in the post-war period (associated with troughs on the chart, since valuations are shown on an inverted scale), but those valuation extremes have ultimately been associated with predictably dismal outcomes. For a detailed exposition, including a mathematical decomposition that formalizes this relationship, see Rarefied Air: Valuations and Subsequent Market Returns. One of the reasons I created the MarketCap/GVA measure was to incorporate estimated foreign revenues of U.S. companies, as many investors seemed to imagine that international trade has vastly changed valuation relationships. As it happens, the effect on valuations, and their relationship with subsequent returns, is far more modest than seems to be assumed. For data and a detailed discussion on this point, see The New Era is an Old Story. In that light, the next chart shows the ratio of nonfinancial market capitalization to GDP. Here, I’ve imputed some of the pre-war data points based on highly correlated proxy data that is available through the full period, as one can do for forward operating earnings and other series. Since the potential effect of estimation error is larger the further one goes back, I’ve presented only data since 1925, where I’m reasonably confident that the estimates are valid. The expanded chart gives further support to Warren Buffett’s 2001 comment in Fortune that the ratio of market capitalization to GDP is “probably the single best measure of where valuations stand at any given moment.” Though MarketCap/GVA performs slightly better in post-war data, GVA is difficult to estimate back to the 1920’s. In any event, both measures have remained strikingly accurate in recent cycles. MarketCap/GDP is shown in blue, on an inverted log scale (left). Actual subsequent 12-year S&P 500 nominal annual total returns are shown in red (right scale).

As with nearly every good valuation measure, the usual outliers are apparent above. Actual market returns were worse than one would have expected in the 12-year period that followed the early-1960’s, largely because of the combination of unexpected inflation and recession that brought valuations to a secular low in 1974. Conversely, actual market returns were better than one would have expected in the 12-year period that followed 1988, largely because the tech bubble brought valuations to a secular peak in 2000. Every bear market in history, including those that completed recent cycles, has taken valuations to the point where expected long-term returns approached or exceeded 10% annually. This is also true for bear markets prior to the 1960’s when interest rates regularly hovered at levels similar to the present. On a combined set of historically-reliable measures, we presently estimate that valuations are more than twice their historical norms; twice the level that has routinely been pierced to the downside in even the most run-of-the-mill market cycle completions across a century of history, regardless of the level of interest rates. Valuations and full-cycle market outcomes - the other side of the mountain With the S&P 500 still within a few percent of its record 2015 high, investors have a critical opportunity here to understand the difference between a run-of-the-mill outcome and a worst-case scenario. The present ratio of MarketCap/GDP is about 1.2, which we fully expect to be followed by nominal total returns in the S&P 500 of about 2% annually over the coming 12 years. Given the current dividend yield on the S&P 500 actually exceeds 2%, the historically run-of-the-mill expectation from current valuations is that the S&P 500 Index itself will be below current levels 12 years from today, in 2028. I realize that a projection like this seems preposterous. Unfortunately, this just reflects objective evidence that has remained reliable over a century of market cycles. Recall that our real-time projection for 10-year S&P 500 total returns in 2000 was correctly negative even on the basis of optimistic assumptions. The basic arithmetic was the same. Notice that expected market returns of about 6% have historically been associated with a MarketCap/GDP ratio of 0.8. The historical norm associated with 10% equity returns has been about 0.6. The secular lows of 1949 and 1982 hit ratios about 0.33. So a rather minimal completion of the current cycle would take the market down by about -33% from here (=0.8/1.2-1), a run-of-the-mill cycle completion would be about -50%, and a truly worst-case scenario would take the market down by about -73% to a secular valuation low in the current market cycle. One can’t rule anything out given reckless monetary policy, fragile European banks, excessive covenant-lite lending and so forth, but I don’t expect more than a run-of-the-mill cycle completion here. Once we consider market outcomes beyond more than a couple of years, we have to be careful to take GDP growth into consideration. Assuming labor market participation, productivity, and inflation all eventually recover, suppose that nominal GDP growth averages something close to 5% annually in the future. The mapping between valuations and investment returns is then just straightforward arithmetic. For example, a move to normal valuations 12 years from today would result in a change in the S&P 500 Index of: (1.05)^12 x (0.6/1.2) - 1 = -10.2%, or about -0.9% annually. Adding dividend income would bring the total return closer to 2% annually. So again, it’s not a worst-case scenario to expect the S&P 500 Index to be slightly lower, 12 years from now, than it is today. It’s the run-of-the-mill expectation. No, to estimate the worst-case scenario, we have to contemplate secular valuation lows. Unfortunately, from current valuation extremes, those calculations are quite ugly. Given 5% nominal GDP growth over a 12-year horizon, a secular low in 2028 would result in a change in the S&P 500 Index, from current levels, of (1.05)^12 x (0.33/1.2) - 1 = -50.6%, or about -5.7% annually. That's your worst case scenario on a 12-year horizon. Imagine, for example, that the next secular valuation low doesn’t occur for another 25 years. The same arithmetic implies that a secular low in 2041 would result in a change in the S&P 500 Index of: (1.05)^25 x (0.33/1.2) - 1 = -6.9%, or about -0.3% annually. That’s your worst case scenario for very long-term investors: seeing the S&P 500 Index below its present level, 25 years from now. To avoid some version of that outcome, we basically have to rule out the possibility of a secular market low at any point in the next quarter-century. When one contemplates everything that happened from 1925 to 1950, or 1950 to 1975, or 1975 to 2000, it’s clearly a stretch to rule out anything of the kind. Are we saying that investors should avoid stocks until valuations register a secular low? Absolutely not. Rich valuations often have very little impact over shorter portions of the market cycle. Overvalued markets can persist for quite a long period of time provided that investors are inclined toward risk-seeking (which is most reliably inferred from market internals across a broad range of individual stocks, industries, sectors, and security types, including debt securities of varying creditworthiness). And even though aggressive and persistent Fed easing didn’t avoid the collapses of 2000-2002 and 2007-2009, those collapses did rapidly improve valuations and raise prospective returns. In short, there’s a compelling reason to lighten up on market exposure when rich valuations are joined with poor market internals, but there will also be numerous opportunities to establish market exposure over time without requiring particularly depressed valuations. Look, I’m the first to concede that after establishing a rather distinguished reputation in previous, complete market cycles, I stumbled badly in 2009 after insisting on stress-testing our methods of classifying market return/risk profiles against Depression-era data, resulting in a series of knock-on challenges that took until mid-2014 to fully address (for the narrative, see the Box in The Next Big Short: The Third Crest of a Rolling Tsunami). Still, one begs for trouble if their only rebuttal to obscene overvaluation and a century of evidence is a whimpering ad-hominem about things I’ve already recognized, discussed, and addressed. Nothing in my subjective narrative alters the objective fact that market risk is wickedly elevated here on the most historically reliable measures. The central lesson to be learned from market history - and particularly from yield-seeking bubbles - is not that valuations are irrelevant, nor that central bank intervention is capable of sustaining bubbles permanently. Rather, the lessons are: 1) market internals, and the investor risk-preferences they convey, are the hinge between overvalued markets that remain elevated and those that collapse, and 2) unlike prior market cycles, even extreme “overvalued, overbought, overbullish” conditions were insufficient to derail speculation in the face of reckless monetary policy since 2009 - one had to wait until market internals deteriorated explicitly before adopting a hard-negative market outlook. If one learns those hard-won lessons about the importance of investor risk-preferences and market internals over portions of the market cycle, one need not fall prey to the delusion that easy money can support stocks once risk-aversion sets in (recall 2000-2002 and 2007-2009), and one need not make the mistake of discarding the essential lessons that valuations have taught in complete market cycles across a century of history. To summarize present market conditions, the most historically-reliable valuation measures remain obscenely elevated; we fully expect nominal total returns for the S&P 500 to average 0-2% over the coming 10-12 years, with negative real returns over both horizons; and we expect a 40-55% market decline to complete the current market cycle. All of these would be only run-of-the-mill outcomes from present valuations. Market internals remain broadly unfavorable, but we’ve recently observed just enough improvement in trend-sensitive measures to hold us to a neutral rather than hard-negative outlook over the very near-term. A break below roughly 1975 would restore a hard-negative outlook. While we have to be comfortable with some amount of near-term uncertainty, I expect the completion of the present market cycle to produce strong opportunities to adopt a constructive or aggressive market stance. As I’ve said before, only informed optimists reject that the market is forever doomed to rich valuations and dismal future returns. That optimistic outlook has a century of evidence on its side.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |