|

|

||||||

|

|

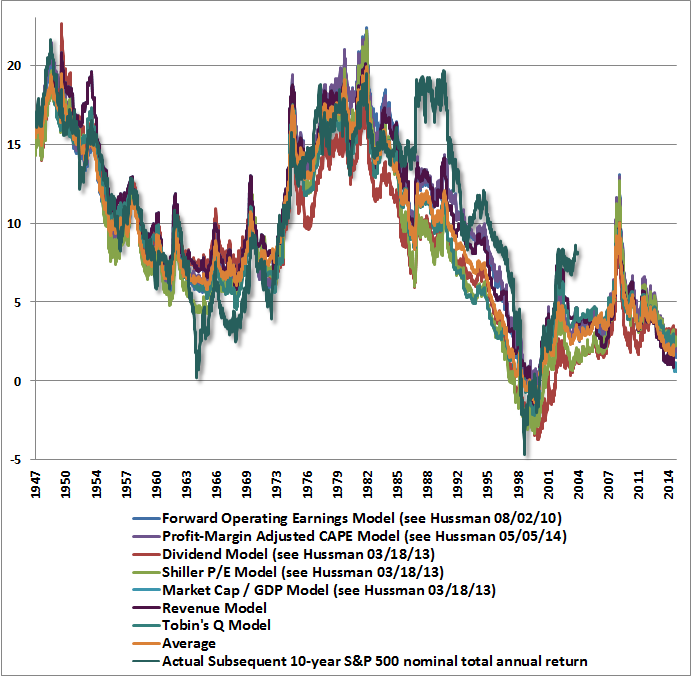

February 16, 2015 Extreme Overvaluation and the Inventory Problem Last week’s advance had the earmarks of a short-squeeze, featuring a low-volume advance to marginal new highs on a number of indices including the S&P 500, on hopes that a Greek bailout and a firming in oil prices will put a floor under global economic deterioration. On factors that affect our estimate of the market return/risk profile, credit spreads remain broadly wider than they were a few months ago, and our primary measures of market internals remain unfavorable. Meanwhile, equity valuations – on the most historically reliable measures we identify – are now fully 117% above their pre-bubble norms, on average. As of Friday, our estimate of prospective 10-year S&P 500 annual nominal total returns has declined to just 1.4%, suggesting that even the dismal 2% yield-to-maturity on 10-year bonds is likely to outperform equities in the decade ahead. The chart below brings the present situation up to-date, showing the 10-year annual nominal total return (in percent) projected for the S&P 500 on a variety of historically reliable methods, compared with the actual subsequent 10-year return of the S&P 500 over the following decade.

Note that actual subsequent return sometimes overshoots or undershoots the return that one would have projected a decade earlier – “errors” that are indicative of secular under- or overvaluation at the end of those 10-year periods (see the discussion in Expect a Decade of 1.7% Portfolio Returns from A Conventional Asset Mix). Just as the shortfall of actual 10-year returns from those projected in 1964 reflected the collapse to secular undervaluation in 1974, and the surplus of actual 10-year returns from those projected in 1988-1990 reflected the move to extreme overvaluation in 1998-2000, the recent overshoot of actual 10-year returns from those projected in 2004 is indicative of severe secular overvaluation at present. So even apparent “errors” are actually highly informative (in fact, these errors are better correlated with actual subsequent market returns than many popular valuation methods such as the Fed Model). From the chart above (and those I published in the midst of the financial crisis), it should be clear that our valuation methods themselves were not the reason for our challenges in the half-cycle since 2009. The January 12, 2015 comment A Better Lesson than This Time is Different details and brings to a close our discussion of those challenges – which had their origins in my unfortunately timed insistence on stress-testing our methods against Depression-era data, when valuations similar to those we observed in 2009 were followed by a further two-thirds collapse in the stock market. We view the difficult transition that followed to be complete. The upshot is that equities are likely to produce total returns close to zero over the coming decade. But they still present something of an “inventory” problem. The basic inventory problem is to accumulate inventory prior to advances in price, to hold that inventory as long as it appreciates in price, and to release that inventory when prices are elevated. What we observe at present is a market where the inventory now fetches record prices and is likely to enjoy little return for long-term holders, and suffer severe losses over the completion of the present cycle. But should short-term demand become even greater, one can’t rule out a move to even higher prices and even more dismal long-term prospective returns – something to be celebrated by those who hold out long enough to sell at that point, but tragic for those who actually buy the inventory in the hope that it will be rewarding over time. Investors essentially differ in the amount of averaging that they bring to this inventory problem. Buy-and-hold investors tie their wagon to the fact that average historical equity returns have been satisfactory over the very long-term, and fully ignore the large swings in prices and valuation that invariably occur over the course of the market cycle. We don’t have any problem with this approach, provided that buy-and-hold investors are fully aware and mentally prepared for the cyclical risks involved, and that they align their portfolio duration to the expected horizon over which the funds will be needed (see Hard Won Lessons and The Bird in the Hand for more discussion). Full-cycle investors give more attention to the variations in prospective returns that are indicated by reliable measures of valuation. From an investment perspective, we observe that expected 10-year returns are at dismal levels at present. We also observe that except for the cycle that ended with the 2002 low, every market cycle in history (both post-war and Depression-era) ended with prospective 10-year S&P 500 total returns in excess of 10% annually, even in periods prior to the 1960’s when interest rates were quite similar to those we observe at present. The response of such an investor is simple – cut risk and brace for the market difficulty that will emerge over the completion of the market cycle. Still, there is an even narrower and much more speculative approach to this inventory problem, which is focused on a shorter horizon than the complete cycle, attempts to fully capture returns even in segments of the market cycle that have already reached extreme valuations, and ridicules full-cycle investors who might, in hindsight, miss such opportunities. The typical problem with this approach is that speculators invariably wear out their welcome by holding inventory even after indications of growing investor risk-aversion have emerged. The eventual attempt of speculators to exit a narrow door simultaneuosly at rich valuations is chronicled in air-pockets, free-falls and crashes across a century of market history. For our part, the best approach we’ve found to these problems of varying coarseness is to focus on a full-cycle investment discipline, but to overlay that with features that are at least moderately tolerant of the rare speculative bubble. We certainly believe that the long-term prospects for equities remain dismal at current valuations, but if there is one key lesson to draw from the challenges we’ve addressed in recent years, it’s that the near-term outcome of speculative, overvalued markets is conditional on investor preferences toward risk-seeking or risk-aversion, and those preferences can be largely inferred from observable market internals and credit spreads (see A Better Lesson than “This Time is Different”). So we remain focused on the condition of market internals, credit spreads, and other measures of investor risk preferences, as an improvement on those measures could open the prospect of further speculation regardless of the level of valuations. Even in that event, a value-conscious, risk-managed, full-cycle discipline would not ignore the valuation extremes. Rather, a return to risk-seeking investor preferences might warrant an outlook along the lines of “constructive with a safety net.” In any case, instead of speculating about whether or not Greece will obtain more favorable bailout terms, or whether global economic activity will reverse the recent evidence of deterioration, our primary focus remains on those measures of investor risk preferences. Suffice it to say that current equity markets are no place for long-term investors, and that even a resumption of risk-seeking investor preferences would demand a considerable safety net. For now, we believe the best interpretation of recent market action is as a hopeful, low-volume short-squeeze to marginal new highs, despite early deterioration in market internals following a period of extreme overvalued, overbought, overbullish conditions. This pattern is much like we observed in September 2000 and October 2007. Still, we can’t rule out a more durable resumption in risk-seeking preferences, which we’ll infer from market internals and other factors, and we’ll take fresh evidence as it arrives in any event. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |